Alphabet Inc (Symbol: GOOGL) made waves as new options began trading for the January 2026 expiration this week. With 700 days until expiration, these fresh contracts bring a potential opportunity for sellers of puts or calls to earn a higher premium than the ones with a closer expiration. YieldBoost formula by Stock Options Channel has delved into the GOOGL options chain for the new January 2026 contracts and identified significant put and call contracts.

Potential Returns on Put Contracts

The put contract at the $140.00 strike price currently has a bid of $16.15. In the scenario of a sell-to-open action on that put contract, the investor commits to purchase the stock at $140.00 while collecting the premium. This sets the cost basis of the shares at $123.85, presenting an appealing alternative to the current share price of $141.38.

Given that the $140.00 strike denotes an approximate 1% discount to the current trading price of the stock (out-of-the-money by that percentage), there is a 63% chance the put contract would expire worthless. If this occurs, the premium would represent an 11.54% return on the cash commitment, or 6.02% annualized — a phenomenon Stock Options Channel refers to as the YieldBoost.

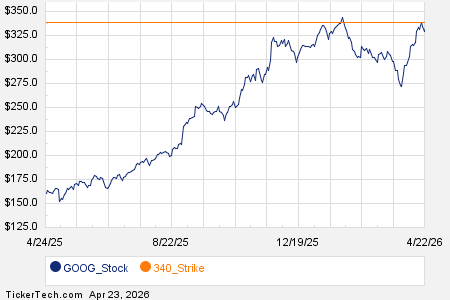

Visual Representation of Put Contract Positioning

Below is a chart showing the trailing twelve-month trading history for Alphabet Inc, pinpointing where the $140.00 strike is located relative to that history:

Exploring Opportunities with Call Contracts

On the calls side of the option chain, the call contract at the $160.00 strike price currently has a bid of $19.15. If an investor was to sell-to-open that call contract as a “covered call,” after purchasing shares of GOOGL stock at the current price level of $141.38/share, they commit to sell the stock at $160.00. The call seller also collects the premium, bringing about a total return of 26.72% if the stock is called away at the January 2026 expiration.

However, there is a possibility that the covered call contract would expire worthless, leaving the investor with both their shares of stock and the premium collected. The current odds of this happening are 43%, which if realized, would represent a 13.55% boost of extra return to the investor, or 7.06% annualized (referred to as the YieldBoost).

Visual Representation of Call Contract Positioning

Below is a chart showing GOOGL’s trailing twelve-month trading history, with the $160.00 strike highlighted in red:

The implied volatility in the put contract example records 34%, while the implied volatility in the call contract example is 28%. Meanwhile, the actual trailing twelve-month volatility is calculated to be 28%. For more put and call options contract ideas worth exploring, visit StockOptionsChannel.com.

Also see:

WRLD shares outstanding history

CCI Dividend History

TFX market cap history

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.