This article delves into the glaring divergence between U.S. fiscal policy and U.S. monetary policy over the past year, and its differential impact on various sectors of the economy.

It also takes a look at the sharp variance in these policies among the United States, Europe, and China.

The Clash of Titans: The Fed vs the Treasury

Over the past several years, navigating an overarching macroeconomic framework has been indispensable. Yet, maintaining agility and adaptability within that framework has been equally crucial. In retrospect, my success was attributed to my willingness to continuously revise my perspective based on the dynamic indicators during these tumultuous times.

From 2019 into 2022, I took a bullish stance on inflation and a bearish position on bonds, underscoring the likely manifestation of fiscal-driven inflation. I defined it as a shift from monetary dominance to fiscal dominance. This foresight turned out to be remarkably accurate as the market bore witness to a four-decade-high inflation and the most severe bond bear market in modern history. The timing and magnitude of these events closely aligned with my predictions.

Thus far, the tools employed by central banks have not been inflationary, primarily uplifting asset prices rather than bolstering middle-class consumption. They engaged in money printing, yet retained the money within central bank balance sheets by procuring bonds.

If central bank measures become more aggressive, coupled with fiscal policies and a focus on the middle class, they hold the potential to override the prevailing deflationary pressures with sheer monetary expansion. They can dispense helicopter money to alleviate debts, escalate inflation, bolster infrastructure, rescue underfunded pension systems, and fortify the middle class, should policymakers opt for this course.

I certainly wouldn’t want to possess a 20-year or a 30-year bond at remarkably low fixed yields in such an environment. Negative yields would be even more precarious.

– Excerpt from “The Bond Market is Spookier Than the Stock Market,” July 2019

Eventually, by early-to-mid 2022, it became apparent that the Fed intended to aggressively combat inflation, a stance that caught me off guard. Subsequently, my viewpoint shifted towards an impending cyclical period of disinflation and likely recession, while emphasizing my belief in more inflationary cycles throughout the decade. Historically, most inflationary periods comprise multiple discrete waves of inflation and disinflation, and this was shaping up to be no exception.

Initially, I anticipated the peak in year-over-year inflation to occur in Q1 2023, with some caveats concerning the right-tail risk from potential oil shortages that could extend it. The invasion of Ukraine by Russia in late February 2022 indeed activated this right-tail risk, contributing to the inflation peak a couple of months later in Q2 2023.

Due to base effects in the CPI calculation, there’s a reasonable likelihood of witnessing a local peak in the official CPI sometime in Q1 2022 within the 7-9% year-over-year range.

– Excerpt from Stock Waves Report, December 12, 2021

The producer price index is indicating signs of having reached a local peak in year-over-year terms. I anticipate a similar occurrence for the headline CPI by late Q1 or early Q2. Essentially, I believe there’s a good chance that year-over-year inflation will reach a local peak in a couple of months, leading to a period of stagnant or lower year-over-year inflation prints, while still remaining above the target. The right-tail risk to this view is that a spike in oil prices this summer due to supply shortages and strong demand from emerging markets could result in inflation, or more precisely, stagflation, even higher than my base case.

– Excerpt from Stock Waves Report, February 2, 2022

Overall, I continue to regard the macro environment as being in a cyclically disinflationary period, amidst an inflationary decade. Thus, managing a portfolio hinges on one’s time frame; assets anticipated to perform well over the next 5+ years could feasibly exhibit weakness over the next 6-12 months. When in doubt, I consistently adhere to my longer-run timeframe, while endeavoring to rebalance around the fringes, counter-cyclically.

– Excerpt from Stock Waves Report, August 7, 2022

Collectively, the consumer price index has surged by 19% since the start of 2020, which spans four years now. Under normal circumstances, with the Fed meeting their 2% inflation target annually, this increase would amount to approximately 8% during this period. This enduring elevation in prices elucidates why, despite cooling down in terms of rate of change, inflation still poses a burden for many individuals:

Back in May 2022, when interest rates loitered below 1%, I published an article, “Inflation Or Recession,” where I posited that the Fed’s tightening would likely yield a myriad of outcomes:

The Fed can plausibly persevere with tightening for an extended period. However, if the Fed raises rates to 3%, 4%, 5%, and beyond, when the debt as a percentage of GDP stands at such elevated levels, the annual interest expense of the U.S. Treasury would surpass $1 trillion, potentially precipitating financial distress among myriad companies and households attempting to refinance their debts. Moreover, a persistent reduction in their balance sheet through QT would exert a negative drag on money creation and asset prices.

Opinion: Unpacking the Fed’s Rollercoaster

Opinion: Unpacking the Fed’s Rollercoaster

The Unforeseen Ramifications

The dollar would likely strengthen further in that scenario, which would squeeze all of the countries that have a lot of dollar-denominated debt (which is primarily owed to places like Japan, Europe, and China). The foreign sector in aggregate would likely stop buying Treasuries, and might have to sell Treasuries to get dollars, like they did during March 2020.

US corporations would have unfavorable exchange rates on their exports, and export volumes would probably decrease.

The various yield curves would likely invert, the Treasury market would likely become illiquid, the high yield credit market would likely become illiquid, and recession indicators would probably worsen. Demand will have been reduced, but at the cost of a recession, and the financial system would start to seize up.

-May 2022, “Inflation or Recession”

The Unexpected Turn of Events

Almost all of that happened… at first. As the Fed continued to sharply raise rates, the Treasury’s annualized interest expense exceeded $1 trillion, many non-investment grade companies and real estate owners ran into major refinancing challenges, the dollar index strengthened to twenty-year highs through September 2022, exports stagnated, manufacturing contracted, the foreign sector in aggregate reduced its total holdings of Treasuries, the Treasury market became very illiquid in September 2022, the yield curve inverted, and the full year 2022 was terrible for most asset prices.

However, there were two important areas that held up much better than I personally expected: large investment-grade companies and homeowner consumers. That’s because they had locked in so much long-term fixed rate debt at low interest rates, that they were mostly immune to the Fed’s aggressive interest rate increases. And to the extent that upper middle class homeowners and large corporations had a lot of cash-equivalents, those cash-equivalents started to give them more interest income (largely from the U.S. Treasury) even as their interest expenses were locked in place, which ironically can be economically stimulating for them even as their weaker counterparts suffer.

The Fed’s aggressive interest rate increases mainly hit small businesses (which typically rely on shorter-duration bank loans), non-investment grade corporations (which issue shorter-duration bonds), commercial property developers and operators (which rely on shorter-duration leverage than residential real estate owners), and ironically the federal government itself (which uses rather short-duration debt on average).

Starting in Q4 2022, when market conditions and liquidity conditions were at their worst, the U.S. Treasury department began to override the Fed. The Treasury began rapidly drawing down their Treasury General Account, which began pushing money back into the financial system as fast as the Fed was removing it with quantitative tightening. Some of this was done of their own accord, but then the January-to-June 2023 debt ceiling impasse forced them to drain all of their spare liquidity into the market.

That period in January 2023, especially when seeing the debt ceiling liquidity drain ahead, is when I began to wake up and pivot again in my analysis and writings. My bearishness for the next six months decreased, because I saw these pro-liquidity moves from the Treasury. And then by spring 2023 I began to see how the larger and larger fiscal deficits were stimulating some parts of the economy despite the Fed’s hawkishness. And ironically the more the Fed raises rates, the more it increases the federal government’s deficits, which increases that stimulus and thus counteracts part of the Fed’s tightening.

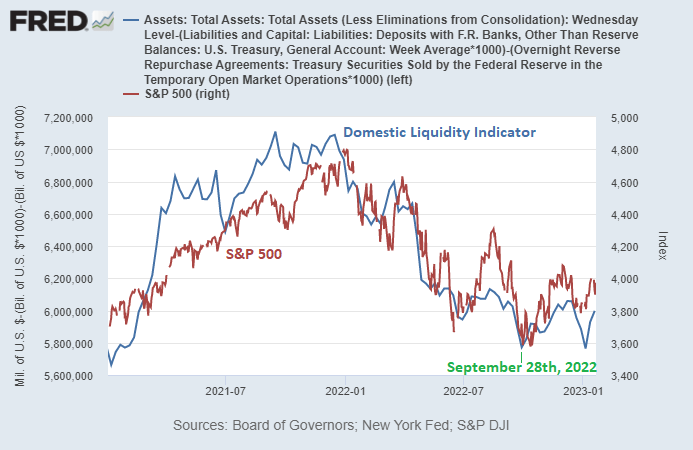

Domestic liquidity in the United States has been rather sideways since the start of Q4 2022. This metric (blue line below) represents the Fed’s balance sheet minus the Treasury General Account and minus reverse repos, with the S&P 500 (red line below) shown for comparison purposes:

The Fed has been the primary reducer of liquidity as it lets bonds mature off of its balance sheet each month, which is a form of quantitative tightening. On the other hand, as the Treasury Department has drawn down its Treasury General Account since mid-2022, this has added some liquidity back into the market. The net result has been rather sideways liquidity lately.

Going forward, this sideways liquidity situation is likely set to continue for the next few months. The Fed is still reducing its balance sheet (negative for liquidity) while the debt ceiling issue is likely to result in lower Treasury General Account balances (ironically positive for liquidity) until the debt ceiling is resolved, as described in the next section.

-January 8, 2023 Stock Waves Report

The Power of Fiscal Dominance

This was where being nimble with my view was important. Back in 2022 I had originally doubted that the Fed would be able to raise rates past 3%, but seeing all of these actions and impacts by the U.S. Treasury starting in Q4 2022 and then moving into 2023 balanced out my view. It’s important to respect the power of fiscal dominance.

In my April 2023 article, I laid out some of the forward paths for when the debt ceiling is lifted. The main question is what would happen to liquidity in June 2023 when the debt ceiling impasse was resolved, and I laid out three primary options. The answer ended up being Option 2), where the Treasury issues an atypically large ratio of T-bills:

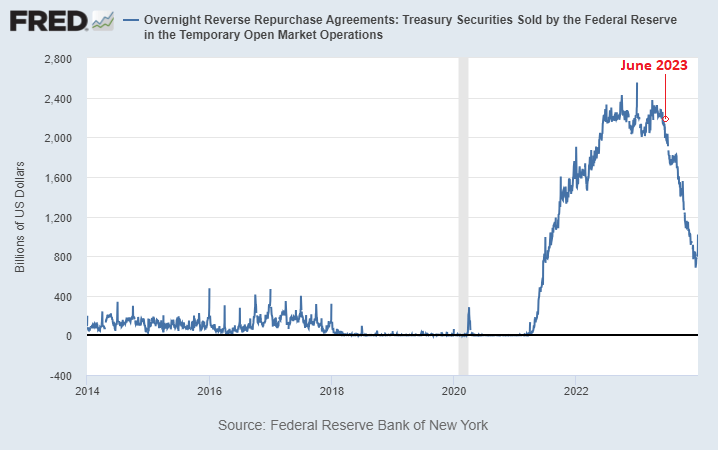

Option 2) The U.S. Treasury Department could issue a ton of T-bills to refill its general account, rather than issue long-duration bonds. This would reduce the average duration of government debt, and is currently the most expensive part of the Treasury curve to issue debt on, but it would likely suck cash out of reverse repos and allow the Treasury to refill its account without damaging commercial bank liquidity. There is about $2.3 trillion in reverse repos that could find a home in T-bills specifically. The Treasury Department could also keep its cash balance low for a while and try to refill it very gradually.

-April 2023, “Navigating the Debt Ceiling Impasse”

The following chart shows the Fed’s reverse repo facility being drained. As it falls back down, it pushes liquidity back into the financial system:

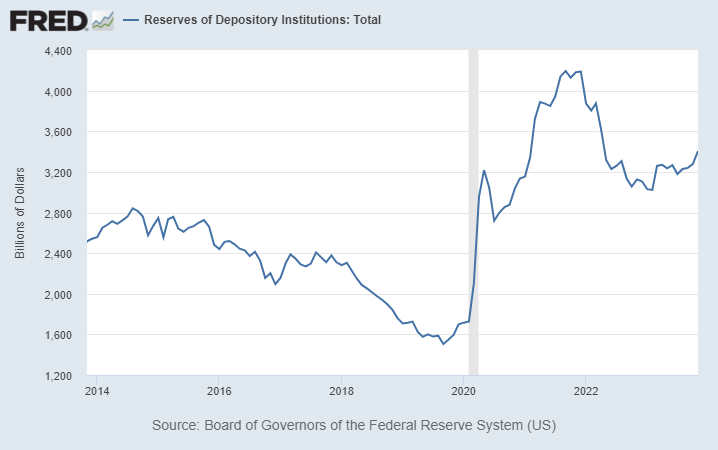

And commercial bank liquidity has indeed avoid being damaged. Bank reserves reached a local bottom in Q1 2023 just prior to the March 2023 banking crisis, and have been on a mild uptrend since then:

Ever since the fourth quarter of 2022, and extending all throughout 2023, the U.S. Federal Reserve and

Liquidity Tug-of-War: How Treasury and Fed Policies Vie for Control

The U.S. Treasury and the Federal Reserve have been executing sharply contrasting tactics, effectively creating a seesaw in the financial world. As the Fed works to tighten monetary policy, the Treasury is pulling its own levers to inject liquidity back into the financial system. This dynamic interplay has significant implications for investors and the broader economy.

Treasury’s Maneuvers in the Financial System

From September 2022 through May 2023, the Treasury deftly siphoned its own cash reserves into the financial system, effectively offsetting the Fed’s actions. However, a shift occurred from June 2023 onwards, with the Treasury fervently escalating T-bill issuance as a percentage of their debt issuance. This strategic move drained reverse repos back into the financial system, once again counterbalancing the Fed’s initiatives.

The resulting chart presents the dichotomy between the Fed and Treasury’s liquidity operations in year-over-year change terms. The Fed, depicted in blue, has diligently sought to reduce liquidity in the financial system since early 2022. Conversely, the Treasury, portrayed in red, has been proactively increasing liquidity in the financial system since late 2022.

The cumulative effect of these divergent strategies has stabilized domestic liquidity following a period of decline, with a slight upward turn taking place from Q4 2022 onwards.

Impact of Liquidity on the Economy

Liquidity, a pivotal factor in financial markets, also exerts a nuanced influence on the real economy. U.S. manufacturing activity experienced a slowdown throughout 2022, dipping into mild contraction before tentatively stabilizing in 2023. Similarly, the Conference Board’s comprehensive suite of leading indicators reflects this trend, illustrating a fluctuating trajectory.

Contrary to popular belief, economic performance does not unilaterally dictate equity prices; the converse relationship – equity prices shaping economic performance – is equally impactful. Furthermore, fluctuations in liquidity typically precede these interconnected dynamics.

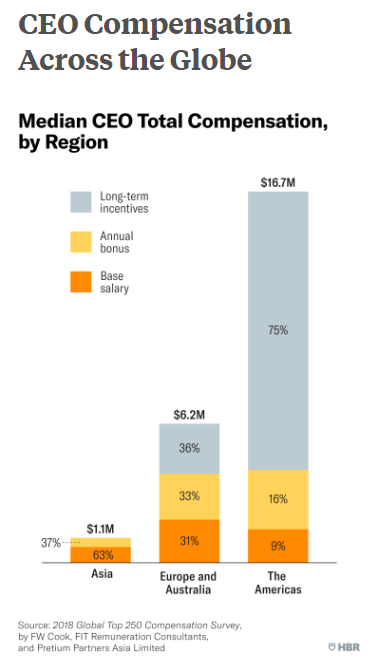

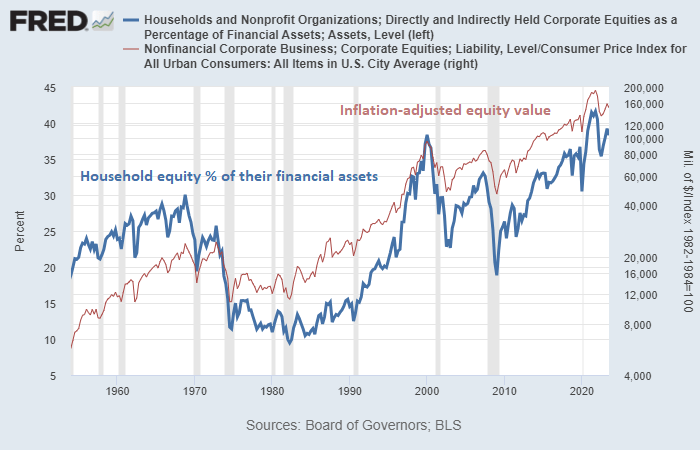

The immense influence of equity prices on wealth distribution is a stark reality. The top 1% of the U.S. population commands 32% of total net worth, with the subsequent 9% controlling an additional 36%. This collective group holds a staggering 68% of overall net worth.

Equity composition further skews this distribution, with the top 1% owning 54% of equities and the broader top 10% possessing a whopping 92%. Consequently, the fluctuation of equity values significantly impacts the spending, investments, tax payments, and overall financial decisions of this privileged cohort.

Given that a substantial portion of affluent individuals’ net worth is susceptible to changes in equity prices, any fluctuations reverberate across their annual income. Notably, the remuneration structure for CEOs and executives, predominantly comprising stock rewards and options, links their earnings closely to equity performance, outlining the profound impact of liquidity dynamics on top earners.

In conclusion, the intricate interplay between the Treasury and the Fed not only reverberates across financial markets but also ripples into the real economy, ultimately shaping economic performance and wealth distribution.

The Tumultuous Relationship Between Fiscal Policy, Monetary Policy, and Financial Markets

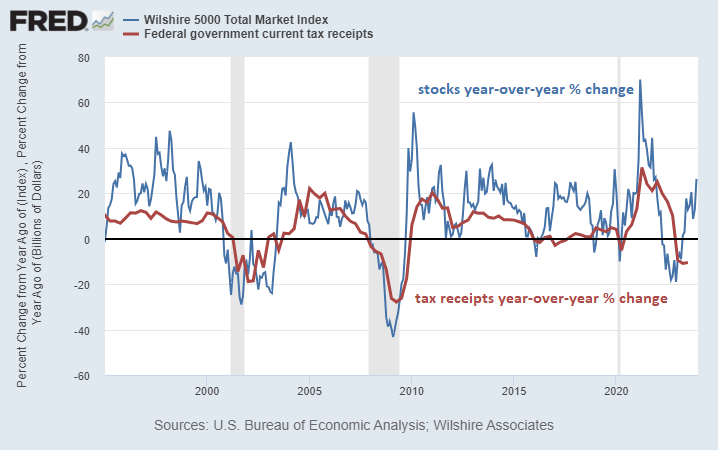

The interconnection between U.S. tax receipts and stock performance has persisted over the years. This correlation creates a feedback loop, wherein equity prices influence fiscal deficits and vice versa. As these deficits swell, they can impact the equity market and overall economy, further reinforcing the relationship. This mechanism has only grown stronger with time, as debts, deficits, and the stock market’s relative size to GDP have increased. Notably, the U.S. stock market has surged from being valued at roughly 70% of GDP three decades ago to approximately 170% of GDP today.

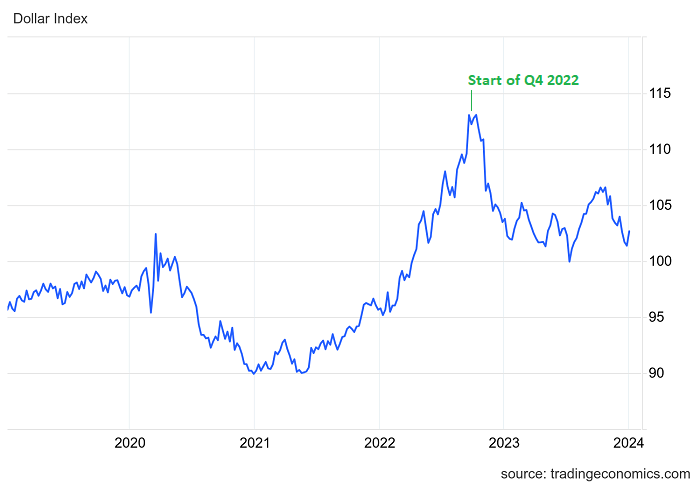

Moreover, the global economy holds an overwhelming $13 trillion in dollar-denominated debt outside the U.S., primarily owed to non-U.S. creditors. Notably, a fluctuating dollar significantly impacts the servicing of this debt for various countries, consequently influencing their economic conditions. The recent peak of the dollar index, coinciding with the trough in global liquidity and asset prices, serves as a poignant example of its far-reaching implications.

The Divergence of Economic Blocs

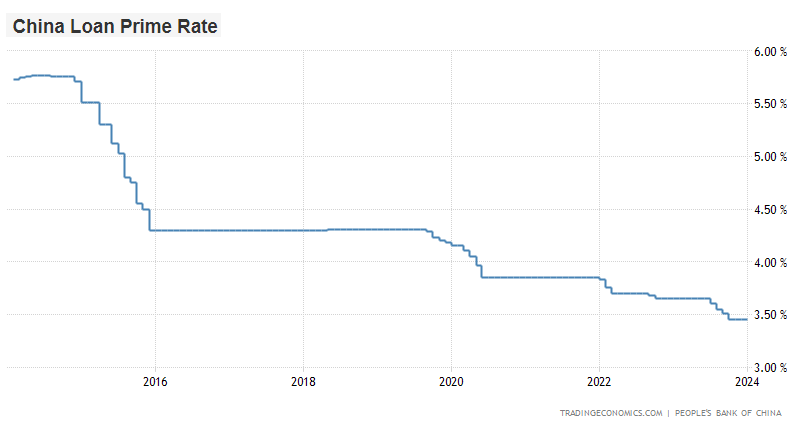

Throughout 2023, the economic policies and outcomes of the United States, Europe, and China have markedly diverged. The U.S. pursued loose fiscal policies paired with tight monetary measures, while China adopted tighter fiscal policies alongside loosening monetary strategies. This contrast highlighted the contrasting impact of fiscal versus monetary policy on economic performance.

Conversely, Europe bore the brunt of these disparities, grappling with tight fiscal and monetary policies, compounded by soaring energy costs. The fallout from Germany’s heavy reliance on Russian gas and the closure of nuclear plants, coupled with the exodus of energy-intensive industries, further darkened the long-term economic outlook for the continent.

Summing This All Together

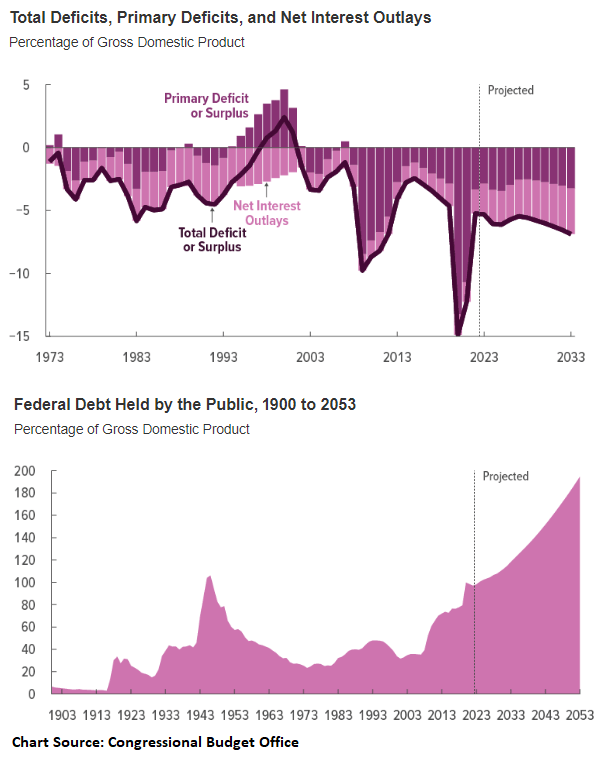

The influences of centralized forces, such as monetary and fiscal policies, extend beyond financial markets to significantly mold economic performance. Recent years have underscored the potency of fiscal policy relative to monetary measures, particularly amidst mounting debts and deficits and the prevalence of unconventional monetary policy. In the past few decades, the role of fiscal policy has steadily expanded, altering the economic and market landscape. Anticipating this trend to persist through the 2020s and into the 2030s seems prudent, given the continuation of structural deficits.

Moreover, the outlook for the 2020s portends a robust performance for real assets globally, including energy, infrastructure, commodities, hard monies, and select emerging market equities. On the other hand, the S&P 500 and other financialized assets may register lackluster real-term growth, given their elevated valuations, extensive U.S. household equity allocations, and substantial foreign investments.

Furthermore, the ballooning proportion of U.S. household financial assets allocated to stocks, in conjunction with inflated equity values, amplifies the challenges of attracting fresh capital into U.S. equity markets.

Navigating Through Financial Analysis

Financial analysts and investors often debunked unconventional viewpoints only to be caught off-guard by ensuing economic shifts. This rigidity of perspective hampers their ability to adapt to evolving market conditions and prognosticate accurately. Notably, macroeconomic cycles unfold at a deliberate pace, defying expectations and evading complete apprehension. While historical frameworks prove instructive, the need to assimilate new variables and embrace a fluid, responsive approach remains pivotal for sound financial analysis.

The free Daily Market Overview 250k traders and investors are reading