Five Below, Inc. (FIVE) reported strong fourth-quarter fiscal 2024 results, with both revenue and earnings exceeding the Zacks Consensus Estimate. Despite an increase in net sales, earnings saw a slight decline compared to the previous year. These results contributed to a 12.6% rise in FIVE’s shares during after-market trading following the announcement.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Five Below concluded the fiscal year with sales and earnings that exceeded expectations. During the holiday season, the company focused on introducing new, trend-forward, value-oriented products while improving its operational execution and store experience. Early indicators of success from these strategies have set a positive tone for fiscal 2025.

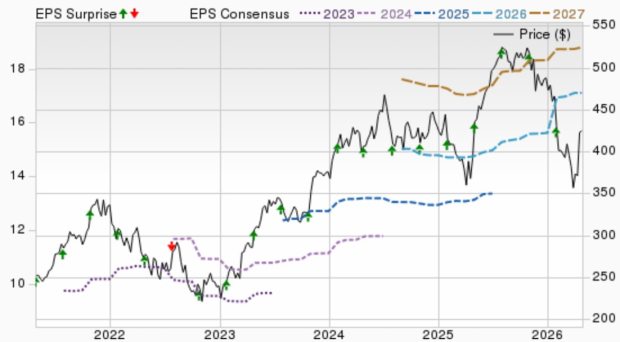

Five Below, Inc. Price, Consensus and EPS Surprise

Five Below, Inc. price-consensus-eps-surprise-chart | Five Below, Inc. Quote

Analysis of Five Below’s Q4 Performance

For the fiscal fourth quarter, Five Below reported adjusted earnings per share of $3.48, surpassing the Zacks Consensus Estimate of $3.38. This figure is a slight decrease of 0.6% from $3.65 in the same quarter last year.

Net sales reached $1,390.9 million, reflecting a 4% year-over-year increase and exceeding the Zacks estimate of $1,372 million. However, comparable sales dropped 3% due to a 1.9% decrease in comparable transactions and a 1% decline in the comparable average ticket.

Margins and Cost Overview of FIVE

Adjusted gross profit increased by 2.1% year over year, amounting to $563.2 million. The adjusted gross margin declined approximately 70 basis points to 40.5%, better than the anticipated 40.3%. This decline largely resulted from fixed cost deleverage due to negative comps and specific timing of product costs, partially offset by reduced shrink attributed to last year’s reserve true-up.

Meanwhile, selling, general, and administrative (SG&A) expenses rose by 8.5% to $267 million. As a percentage of net sales, SG&A expenses increased by roughly 80 basis points to 19.2%. Factors influencing this rise included fixed cost deleverage from negative comps, higher store wages, and additional store hours, although these were partially counterbalanced by lowered incentive compensation. We had previously predicted a 10.8% increase in SG&A for this quarter.

Adjusted operating income fell to $253.3 million, down from $268.4 million in Q4 of fiscal 2023, leading to an adjusted operating margin decrease of about 190 basis points to 18.2%, compared to our estimate of a decline to 17.9%.

Financial Snapshot of FIVE: Cash and Equity

At the end of the fourth quarter, Five Below reported cash and cash equivalents totaling $331.7 million, alongside short-term investment securities of $197.1 million. Total shareholders’ equity was valued at $1.81 billion as of February 1, 2025. The company repurchased approximately 267,000 shares in fiscal 2024, totaling about $40 million.

Five Below’s Recent Store Developments

In the latest quarter, Five Below opened 22 net new stores, bringing its total to 1,771 locations across 44 states. This represents a 14.7% increase in store count compared to the end of the previous fiscal quarter. The company plans to open about 150 additional stores by the end of fiscal 2025, aiming for a total of 1,921 stores.

Looking Ahead: Q1 Expectations for FIVE

For the first quarter of fiscal 2025, Five Below anticipates total sales between $905 million and $925 million, reflecting a midpoint growth of 12.7% compared to last year’s first quarter. The company expects to open approximately 50 new stores and forecasts comparable sales growth of 0% to 2%.

The adjusted operating margin is projected at 4% at the midpoint, a decline from 4.7% reported in the previous year, primarily due to SG&A deleverage from increased investments in store labor. Nevertheless, this decline is being counteracted by anticipated gross margin improvement of 40 basis points thanks to lower aged inventory reserves.

Net income is estimated between $25 million and $31 million, while adjusted net income is expected to range from $28 million to $34 million. Earnings per share are projected between 44 cents and 55 cents, with adjusted earnings per share predicted to range from 50 cents to 61 cents, compared with 60 cents in the same quarter last year.

Five Below’s Fiscal 2025 Guidance

For fiscal 2025, the company expects sales between $4.21 billion and $4.33 billion, indicating a 10.1% increase at the midpoint. Comparable sales are expected to remain flat to rise by 3%.

The adjusted operating margin is projected to be approximately 7.3%, which marks an anticipated decline of about 180 basis points year over year due to the impact of tariffs. Net income is forecasted between $216 million and $250 million, while adjusted net income is expected to range from $227 million to $261 million. Earnings per share estimates fall between $3.90 and $4.52, with adjusted earnings per share anticipated to be between $4.10 and $4.72, down from $5.04 reported in fiscal 2024.

For capital expenditures, the company projects a range of $210 million to $230 million, excluding tenant allowances, incorporating new store openings and investments in systems and infrastructure.

In the previous three months, shares of this Zacks Rank #3 (Hold) company have declined by 24.1%, compared to a 13.9% decline in the industry.

Top Stock Alternatives

Other stocks that are ranked better include The Gap, Inc. (GAP), Urban Outfitters Inc. (URBN), and Deckers Outdoor Corporation (DECK).

The Gap operates as a prominent international specialty retailer with a diverse clothing and accessory line. It currently holds a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for The Gap’s fiscal 2025 earnings and revenues indicates growth of 7.7%.

Retailers Show Promising Growth in Earnings Estimates for 2025

GAP reported a projected growth in earnings and revenues of 1.6% for fiscal 2025, based on the company’s performance in fiscal 2024. Over the past year, GAP has delivered an impressive trailing four-quarter average earnings surprise of 77.5%.

Urban Outfitters, a specialty lifestyle retailer known for its fashion apparel, accessories, and home décor, carries a Zacks Rank of 1. The company reported a notable earnings surprise of 16.9% in its latest quarter. Analysts forecast that URBN will see its earnings and revenues grow by 11.8% and 6%, respectively, in fiscal 2025, compared to fiscal 2024. URBN has a trailing four-quarter average earnings surprise of 28.4%.

Deckers Outdoor Corporation, a leading designer and producer of niche footwear and accessories, currently holds a Zacks Rank of 2 (Buy). The Zacks Consensus Estimate indicates that DECK’s fiscal 2025 earnings and revenues are expected to increase by 21% and 15.6%, respectively, from the previous year’s actuals. Deckers has delivered a trailing four-quarter average earnings surprise of 36.8%.

Zacks Highlights Leading Semiconductor Stock

In the semiconductor sector, a new top chip stock has emerged, significantly smaller than NVIDIA, which has seen extraordinary growth of over 800% since being recommended. While NVIDIA remains a strong player, this new stock has the potential for even greater expansion.

As demand for Artificial Intelligence (AI), Machine Learning, and the Internet of Things (IoT) surges, this semiconductor stock is well-positioned to benefit. Global semiconductor manufacturing is expected to grow dramatically, from $452 billion in 2021 to an estimated $803 billion by 2028.

See This Stock Now for Free >>

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Urban Outfitters, Inc. (URBN): Free Stock Analysis Report

The Gap, Inc. (GAP): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.