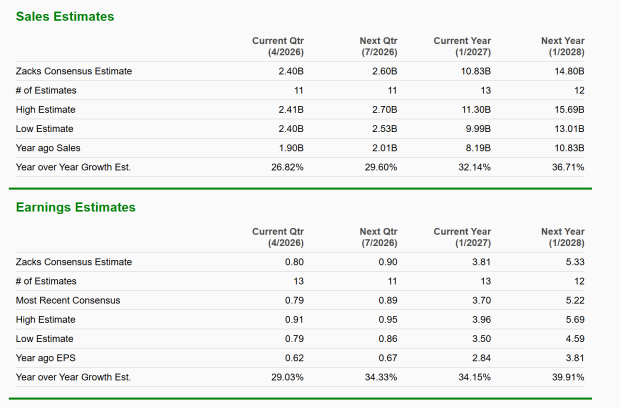

Nvidia and AI: Exploring Alternative Investment Opportunities

Nvidia (NASDAQ: NVDA) has become a leader in the artificial intelligence (AI) sector over the past two-and-a-half years. Its GPUs are integral to major data center projects, particularly among hyperscale cloud clients investing significant capital into AI. This demand has driven substantial revenue and earnings growth for Nvidia during this period.

Investors have been rewarded handsomely, as Nvidia’s stock price surged 239% in 2023 and an additional 171% in 2024. This remarkable increase briefly propelled Nvidia to the top of the most valuable companies list. However, following a recent stock market sell-off, shares are now approximately 25% below their all-time high set in January.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Alternative AI Investment Opportunities

As many investors consider purchasing Nvidia’s shares at a lower price, two other AI companies appear poised for long-term success. Each possesses competitive advantages that ensure resilience, regardless of how AI developments unfold.

Image source: Getty Images.

1. Meta Platforms

Meta Platforms (NASDAQ: META) stands out as a significant long-term beneficiary of generative AI advancements globally, and the company is notably investing in this vision. Management forecasts capital expenditures may reach as much as $65 billion in 2023 to maximize generative AI’s potential through substantial data center expansions.

This investment strategy underscores the belief in a sizable opportunity for business growth. Meta has already started to see positive returns from its AI developments, applying insights from large language model creation to enhance its recommendation systems. This initiative has increased user engagement and the time spent on its platforms.

Moreover, Meta reports robust growth in its AI-driven advertising tool, Advantage+ Creative, with 4 million advertisers utilizing it. The expansion of generative AI could allow small businesses to effectively manage ads with minimal resources or experience. As CEO Mark Zuckerberg stated during Meta’s second-quarter earnings call last year, “Over the long term, advertisers will basically just be able to tell us a business objective and a budget, and we’re going to do the rest.” Such capabilities could significantly broaden Meta’s advertiser base and enhance ad efficiency, leading to higher revenue.

Additionally, Meta is innovating AI chatbots for WhatsApp and Messenger aimed at enabling scalable customer service and sales for businesses. The economic potential of each company employing a range of AI agents via WhatsApp might be valued at around $100 billion, as suggested by some analysts, unlocking tremendous value and revenue growth for Meta.

As a software company, Meta benefits from high operating leverage, meaning its AI advancements can provide value across billions of users. As the AI services continue to scale and generate additional revenue, Meta should experience significant profit growth.

Despite these opportunities, much of the anticipated value from AI advancements is not yet reflected in Meta’s stock price, which trades at about 21.2 times forward earnings at this time. However, with increasing engagement and a growing array of top-tier advertising products, substantial earnings growth could be on the horizon as the company develops its AI capabilities.

2. Taiwan Semiconductor Manufacturing

Nvidia’s current success can be attributed, in part, to the capabilities of Taiwan Semiconductor Manufacturing (NYSE: TSM), or TSMC. This chip manufacturer leads the industry, controlling over two-thirds of semiconductor fabrication spending, a share that continues to increase.

Companies are increasingly turning to TSMC as it is the only manufacturer that can produce the world’s most advanced chips at scale amid rising demand. Its technological lead and significant output capacity enable TSMC to create chips at lower costs compared to its competitors. This leads to a positive feedback loop where TSMC gains more contracts from leading designers, allowing further investment into technology and manufacturing capabilities, widening the gap between TSMC and its competitors.

Due to this competitive edge, TSMC enjoys exceptional stability. While tariffs may temporarily threaten semiconductor demand by raising prices for end users, long-term demand is expected to grow. TSMC is well-positioned to capture a substantial share of this demand, especially from cloud customers who require advanced chips for efficient data center management.

Despite the competitive landscape, there is no guarantee that Nvidia will maintain its dominance in supplying the majority of AI accelerators to hyperscale customers. In fact, many of Nvidia’s largest clients are developing proprietary silicon solutions and exploring alternatives to Nvidia’s high-cost chips. Regardless of the chip designs pursued, TSMC remains the primary manufacturer for these advanced chips.

This situation suggests TSMC should avoid margin erosion, allowing the company to uphold its gross margin target of 53% or more. Presently, TSMC stock trades at just 17.4 times forward earnings, placing it at one of its lowest valuations since the start of the AI boom.

Should You Invest $1,000 in Meta Platforms?

Is Meta Platforms a Smart Investment Right Now?

Before purchasing stock in Meta Platforms, it’s essential to evaluate the recommendations from experts. The Motley Fool Stock Advisor analyst team has identified what they consider the 10 best stocks to buy currently, and surprisingly, Meta Platforms is not included in this select group. The stocks that made the cut are projected to yield significant returns over the next few years.

To put this into context, consider Netflix, which was recommended on December 17, 2004. If you had invested $1,000 then, your investment would have grown to $524,747! Similarly, Nvidia joined the list on April 15, 2005, and a $1,000 investment at that time would now be worth $622,041!*

Furthermore, it’s important to note that Stock Advisor boasts an impressive average total return of 792%, vastly outperforming the S&P 500, which stands at just 153%. Don’t overlook the latest top 10 stock picks available to members of Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of April 14, 2025

Randi Zuckerberg, former director of market development at Facebook and sister to Meta Platforms CEO Mark Zuckerberg, sits on The Motley Fool’s board of directors. Adam Levy holds positions in Meta Platforms and Taiwan Semiconductor Manufacturing. The Motley Fool endorses Meta Platforms, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool maintains a disclosure policy.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.