Palantir Technologies Faces Diverging Analyst Predictions Amid AI Hype

Since the beginning of 2023, artificial intelligence (AI) has sparked significant excitement among investors. This technology empowers software and systems to reason, act autonomously, and evolve, presenting a captivating potential for growth that Wall Street has eagerly recognized. According to estimates from PwC, AI could enhance global gross domestic product (GDP) by 26% by 2030, translating to over $15 trillion in economic impact. However, not all companies will equally benefit from this transformative trend.

Start Your Mornings Smarter! Receive Breakfast News in your inbox every market day. Sign Up For Free »

Nvidia has been seen as a leader in the AI sector, but some argue that data-mining specialist Palantir Technologies (NASDAQ: PLTR) has taken its place as Wall Street’s favorite AI stock. In February, Palantir’s shares surged, approaching a trailing two-year gain of nearly 2,000% at their peak.

Image source: Getty Images.

Yet, like many innovators, Palantir finds itself amidst conflicting views from analysts. Depending on their forecasts, Palantir’s stock could climb as high as $125 (a 46% increase) or drop to $40 (a 53% decline). Let’s explore both perspectives to see which is more plausible.

Palantir’s Primary Bull Predicts 46% Upside

One of Palantir’s staunchest supporters, Mark Schappel of Loop Capital Markets, has a buy rating and sets a target price of $125 per share. This projection implies a 46% upside based on the stock’s closing price of $85.85 on March 28. Notably, this target aligns with the stock’s peak from February 18.

Analysts see Palantir’s unique market positioning as a reason for potential growth. The company operates two primary platforms—Gotham and Foundry—both lacking direct large-scale competitors. While Palantir faces some competition, its AI-driven software-as-a-service solutions are distinct, allowing for predictable sales and cash flow.

Additionally, analysts are impressed by the profitability and consistent double-digit growth of the Gotham platform, serving federal governments with data analysis and military mission planning. Palantir often secures multiyear contracts with the U.S. government, enhancing cash-flow visibility.

Schappel is particularly optimistic about Palantir’s opportunity with Foundry. This newer and rapidly expanding platform helps businesses analyze their data for efficiency improvements. Foundry’s capabilities include data integration, supply chain optimization, and automating decision-making processes, which can significantly enhance business operations.

Palantir’s Top Skeptic Predicts 53% Decline

In contrast, Rishi Jaluria from RBC Capital Markets maintains a bearish stance on Palantir, rating it underperform with a target price of $40. If his forecast holds, it would signify a 53% drop from last week’s close.

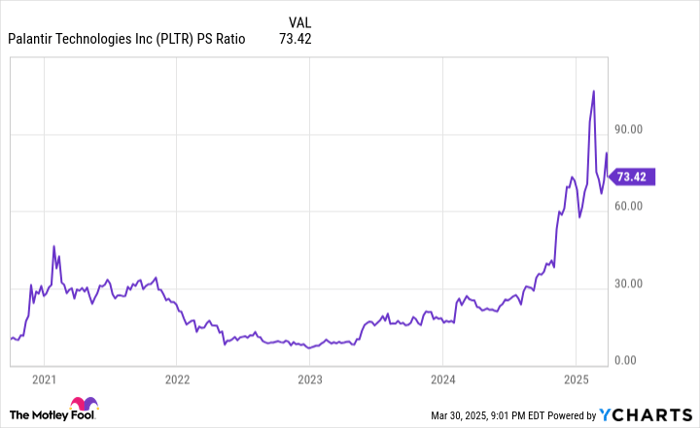

Jaluria has raised concerns about Palantir’s high valuation. Despite being a premium player in its niche, the company’s price-to-sales (P/S) ratio was approximately 100 at its February height—a metric he argues is unsustainable historically for companies benefiting from the latest innovation trends.

PLTR PS Ratio data by YCharts.

Additionally, he cites potential U.S. defense budget cuts as a significant risk. As the Pentagon may cut 8% of its budget over the next five years, reducing spending by roughly $50 billion annually, these trends threaten Palantir’s reliance on defense contracts for revenue.

Jaluria highlights that Gotham, while a crucial profit generator for Palantir, is limited to U.S. and allied countries. This restriction could cap the platform’s growth potential. Furthermore, Jaluria notes a new trading plan for CEO Alex Karp that permits him to sell close to 10 million shares by mid-September, raising concerns over downward pressure on the stock.

Price Target Showdown: Will Palantir Climb or Fall?

The critical question remains: which analyst’s price prediction is more realistically achievable?

While Palantir has technically met Schappel’s price target during intraday trading, historical trends suggest that Jaluria’s bearish view may prove more accurate. Many disruptive technologies over the past three decades have faced significant bubbles that ultimately burst, leading to unmet high expectations among investors.

Image source: Getty Images.

The positive aspect for Palantir is its multiyear government contracts through Gotham, which may offer stability, but its longer-term outlook remains uncertain in this competitive landscape.

Understanding Palantir Technologies’ Valuation and Market Sentiment

Palantir Technologies operates as a subscription-driven segment, but the potential for an AI market downturn raises questions about its future sales performance. Historically, sentiment-driven trading tends to pressure companies with inflated valuation premiums, even if sales don’t drop immediately.

Concerns Regarding Valuation Sustainability

One significant concern is Palantir’s valuation. Last summer, Nvidia reached a peak price-to-sales (P/S) ratio of 42 before its decline. Similarly, leading companies before the dot-com bubble burst exhibited P/S ratios between 31 and 43. Currently, Palantir boasts a P/S ratio around 100, which is not sustainable given historical trends. It’s even reported to be over 70 at present, raising further doubts about its market valuation.

Market Dynamics and Historical Context

Moreover, the S&P 500 has witnessed its Shiller price-to-earnings ratio reach the third-highest level during this prolonged bull market as of December. High valuations like these often indicate impending market corrections for the Stock market.

While Palantir may deserve some valuation premium for its position in the market, it’s important to note that its Stock price could decrease by 50% and still reflect aggressive expectations for future growth.

Should You Invest $1,000 in Palantir Technologies Right Now?

Before making any investment in Palantir Technologies, consider this:

The Motley Fool Stock Advisor team’s analysis has revealed their picks for the 10 best stocks to buy now, and Palantir Technologies is not included. The selected stocks potentially promise significant returns in the upcoming years.

Take Nvidia, for instance. It made the list on April 15, 2005. If you had invested $1,000 then, it would have grown to $664,271!*

Stock Advisor equips investors with a clear and succinct blueprint for investing success, offering insights on portfolio construction, timely analyst updates, and two fresh Stock recommendations monthly. Since 2002, the Stock Advisor has more than quadrupled the S&P 500’s return.* Access the latest top 10 stocks by joining Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of April 1, 2025

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Palantir Technologies. For more information, refer to the Motley Fool’s disclosure policy.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.