Performance Evaluation

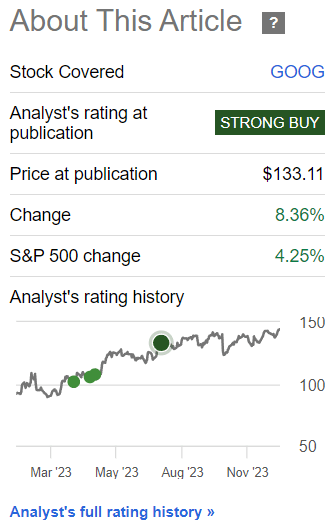

I have held a ‘Strong Buy’ position in Google/Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG) since mid last year. Since the publication of the last article on the stock, the total shareholder return has been +8.36%, compared to +4.25% in the S&P 500 (SPY) (SPX), implying an alpha of +4.11%:

Assessment

Today, I am altering my position to a ‘Neutral/Hold’ due to the following reasons:

- A bullish thesis based on search revenue growth is now less compelling

- Revenue backlog visibility is increasing

- Google Cloud margin progress is stalling

- There is no significant margin of safety in valuation

A Less Compelling Search Revenue Growth Thesis

In my previous analysis of Google, I had noted that:

Google’s advertising engine remains well-positioned and is set to gain momentum with the eventual sectoral rebound.

– Hunting Alpha’s view in the last article on Google

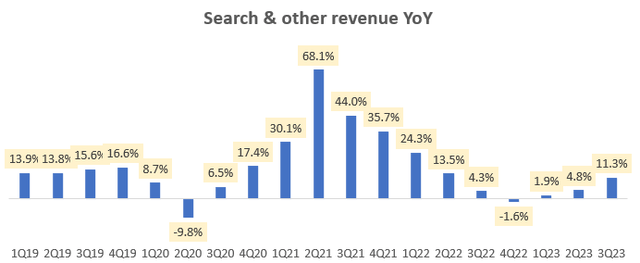

Q3 FY23 results confirmed this view, witnessing a year-over-year growth uptick to 11.3%:

Management attributed this growth to strong performance in the retail vertical, particularly in the value sector:

“We’ve seen 4x deals queries during the holidays versus other periods; 75% of users say they’ll shop with those offering free shipping.”

Senior VP & Chief Business Officer Philipp Schindler in the Q3 FY23 earnings call

CIO and CFO Ruth Porat confirmed a “stabilization in spending by advertisers,” aligning with industry research predictions.

I believe the most effective thesis arguments for a stock are those where the anticipated event’s uncertainty diminishes. When these events start to unfold even before they materialize fully, the alpha opportunity diminishes. For instance, this is why the bullish thesis on Palantir’s (PLTR) inclusion in the S&P 500 became obsolete when the company met all inclusion criteria, even though the event had not occurred.

I see a similar trend with the bullish Search revenues thesis for Google. It is showing signs of progress, thus reducing uncertainty about a more favorable advertising environment. Therefore, I find the opportunity less compelling now.

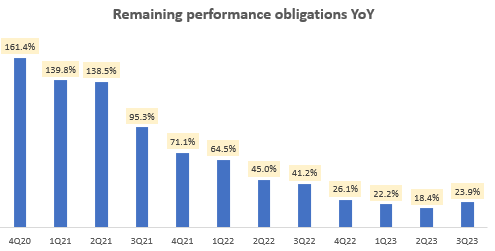

Increasing Revenue Backlog Visibility

Google’s remaining performance obligations (RPO), representing the revenue backlog primarily for the Cloud business, are showing growth acceleration after 10 consecutive quarters of moderated growth. In the latest quarter, there was a 23.9% year-over-year growth:

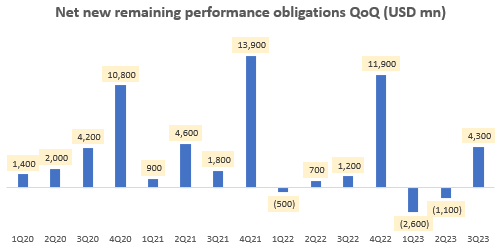

The company experienced a significant net increase of $4.3 billion in quarter-over-quarter new RPO terms, offsetting the previous 2 quarters’ total decline of $3.7 billion:

While this is a positive signal, it remains to be seen if it will result in sustainable growth. Clues from management suggest that although customers have been optimizing their cloud-related expenditures, the Google Cloud Platform [GCP] showed growth rates “above the overall Cloud growth rate.” This could be an early indicator of a rebound in Cloud spending.

Google Cloud Margin Progress Stalls

The chart above reflects my estimate of Cloud EBIT margins after adjustment for a like-for-like comparison between quarters. This neutralizes the impact of accounting adjustments related to the increase in server useful life assumptions. I published a more detailed piece on the “The Hidden Truth Behind Accounting Boosts” earlier last year.

Management identified an increase in data center and operational costs as reasons for the declining margin profile in the Cloud business. It is unclear whether these higher costs have stabilized.

Lack of Margin of Safety in Valuation

Alphabet is trading at a 1-year forward PE of 22.2x, right at the median level over the last 6 years. Given the mixed fundamental arguments and the lack of clarity on a strong bullish thesis, I interpret the current valuations as a lack of margin of safety to support compelling buys.

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing principles of Flow, Location, and Trap.

Regime Change in the Cost Control Culture at Google: What This Means for Investors

Analyzing the technicals on the relative monthly chart of GOOGL against the S&P 500, it is evident that the last major completed swing has been downwards. The current order flow’s rebound has the potential to form a new range, with the relative ratio prices currently trading in the upper half of this likely range, signaling a reduced margin of safety for believing in continued alpha generation.

To establish a clearer bullish outlook on the alpha potential of GOOGL vs the S&P 500 from a technical perspective, one might await the ratio prices to react from the bottom end of the anticipated range or for an impulse push past the top end of the potential range with strength and a successful retest of the highs.

Operational Margin Concerns

In a previous view on Alphabet, it was suggested that Ruth Porat might be able to reduce the bleeding in the Other Bets segment. However, in Q3 FY23, the EBIT margins in this segment deteriorated further.

It is essential to note that it has only been 1 quarter since Porat became the CIO, hence drawing early conclusions must be approached with caution. Margin expansion stands as a key risk to any ‘Neutral/Hold’ thesis, as it amplifies the chances of an omission error.

Porat addressed various operational margin improvement programs within the company, including headcount growth control, real estate footprint savings, gross margin enhancements, AI-generated productivity improvements, and a honing of the focus in the Other Bets portfolio.

Marking a regime change in the cost control culture at Google, there’s clear evidence of much more subdued additions to headcount in the latest quarter compared to the usually substantial increases during 2019 – 2022.

While management highlighted that some of these operational cost control improvements would be offset by higher traffic acquisition costs going forward, the risk of a margin surprise toward the mid-35% EBITDA levels on a normalized basis stands apparent.

Outlook and Positioning

An earlier bullish view on Alphabet/Google has successfully played out, generating an alpha of +4.11% vs the S&P 500. However, the stance is now being shifted to a ‘Neutral/Hold’ as earlier catalysts such as a rebound in Search revenues have materialized, making it more challenging to build a case for compelling incremental anticipation.

Bullish signs of an increased revenue backlog, particularly in the Cloud business, are acknowledged. Nonetheless, this may be counteracted somewhat by higher data center costs pressuring Cloud margins.

The valuations exhibit limited margin of safety, and while the technicals relative to the S&P 500 don’t indicate clear bearishness, the likelihood of continued alpha generation is presently lower. The company has numerous opex-focused margin expansion initiatives in play, constituting a recognized upside risk.

Overall, with reduced confidence in the alpha-generation potential for Google, it is deemed appropriate to commence scaling out and reinvest the proceeds in either the S&P 500 or in other bullish ideas.

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for these views is multiple quarters to around a year. It is not set in stone; however, updates on changes in stance will be shared in a pinned comment to this article, and may also be published in a new article discussing the reasons for the change in view.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.