Unraveling the Forces at Play

Once again, Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) is experiencing a nosedive of nearly 6% in after-hours trading, despite reporting a double beat for Q4 2023. This pattern eerily mirrors the decline witnessed after Q3 2023 earnings. Back then, Alphabet stock took a hit, prompting a modest “Buy” rating at ~$130, as the company grappled with major odds amidst macroeconomic uncertainty.

Heading into a potential recession, my overall outlook for “Magnificent 7” big tech stocks is bearish. However, Alphabet looks fairly valued in light of its post-Q3 sell-off. In the event of a hard landing, I would expect to get a sizable discount on GOOGL stock, but as a long-term investor, I continue to like the business and intend to hold my long position in Alphabet stock for years to come. While I won’t be buying here due to my current allocation being at target weight, I will probably start accumulating shares around the 200-DMA level at ~$115-120 if GOOGL stock were to get there.

The long-term risk/reward for Alphabet remains attractive with a five-year expected CAGR of 14%. In light of its Q3 report, I continue to see Alphabet as a reasonable “safe haven” to hide out in this uncertain macroeconomic environment, with the added bonus of participation in the secular growth mega-trend of artificial intelligence.

Key Takeaway: I continue to rate Alphabet a modest “Buy” at $130, with a strong preference for slow, staggered accumulation.

Source: Google Q3: Double Beat Foiled By Cloud Deceleration And Capex Spend Guidance

Having previously been a fervent Google bull during its $90s phase, my exuberance for GOOGL stock has somewhat mellowed with its staggering ascent to new all-time highs above $150 per share.

In this piece, we shall swiftly analyze Alphabet’s Q4 2023 report, re-evaluate its long-term risk/reward, and determine whether the recent dip in GOOG stock presents a lucrative buying opportunity.

A Succinct Overview of Alphabet’s Q4 2023 Report

Initial projections for Alphabet, Inc. expected revenues and normalized EPS for Q4 2023 to hover around $85.28B and $1.60, respectively. However, despite beating estimates on both parameters, with revenue at $86.31B (a 13.5% year-on-year increase) and normalized EPS at $1.64 (a colossal 56.2% year-on-year surge), Alphabet stock is presently down approximately 6% to $143 per share.

Given that Alphabet stock had previously been significantly outstripping TQI’s fair value estimate of ~$120 per share, the adverse market reaction to these results is not entirely unexpected. Nonetheless, the report showcases a notable upswing in Alphabet’s quarterly financial performance, evident in the surge of revenue growth to +13.5% year-on-year, the expansion of operating margins to 27% (with operating income witnessing a 30% year-on-year growth), and the breathtaking 56% year-on-year surge in diluted EPS.

Despite falling shy of the consensus street expectations by $300 million, Alphabet’s advertising business displayed remarkable resilience in Q4 2023, as both Search and YouTube exhibited robust double-digit year-on-year growth.

Looking forward, the digital advertising market is on an upturn, and Alphabet is reaping the fruits of its monopolistic dominance in Search, which is fueling a robust re-acceleration, countering the prior deceleration in Google’s Cloud business, as evidenced by a growth rate spike from ~22% in Q3 to ~26% in Q4 2023.

Overall, Alphabet’s Q4 2023 report reveals a 13.5% year-on-year revenue surge, propelled by the formidable performance of Search, YouTube, and Cloud, which is driving a renewed acceleration in the company’s top-line growth. As previously discussed, opportunities in the realm of artificial intelligence could very well unlock the next wave of growth for Alphabet.

Let’s now delve into Alphabet’s profitability.

A resurgence in ad spending, combined with management’s cost-cutting strategies, is bolstering Alphabet’s operating income and margins. In Q4 2023, Alphabet’s operating income soared by 30% year-on-year to $23.7B, reflecting an operating margin of ~27.5% (compared to ~23.9% in Q4 2022).

In addition to the promising resurgence in top-line growth in Q4 2023, Google Cloud achieved yet another quarter with positive operating income, boasting an operating margin of +9.4%!

However, a shadow falls on Alphabet’s otherwise stellar Q4 report, as its employee headcount has diminished by a mere 4% year-on-year, despite management reiterating their focus on restructuring Alphabet’s cost base. As you may be aware, the early months of 2024 saw Alphabet laying off hundreds, with CEO Sundar Pichai hinting at more job cuts in the pipeline. This is especially poignant, given Alphabet’s inflated…

Alphabet’s Financial Outlook: A Deep Dive into Q4 2023 Earnings

Once again, Pichai & Co find themselves at a critical juncture, facing the need to re-engineer Alphabet’s cost base amidst the 2024 outlook for increased CAPEX spend on GenAI technical infrastructure. As Alphabet’s management heralds the improvement GenAI has brought to their core products, there is a resounding call for further investment. However, amidst this push, voices abound advocating for stern cost-cutting measures, particularly in terms of employee headcount and real estate, to enhance bottom line performance.

Indeed, the landscape appears shifting, mark by a significant drop-off in Alphabet’s free cash flow to $7.8B in Q4 2023. A stark contrast from the $16B in Q4 2022. Yet, flanking this apparent vulnerability is a one-time tax payment of $10.5B as per management, casting its shadow over Alphabet’s previously robust free cash flow generation.

Nevertheless, with Alphabet’s net cash balance standing at almost $98B, the company boasts a balance sheet of fortress-like proportions, unrivaled among big tech companies for its dearth of long-term debt.

Given Alphabet’s monopolistic dominance in the digital advertising market, colossal AI growth potential, robust free cash flow generation, and solid balance sheet, the stage appears set for Alphabet’s leadership team to deliver healthy and stable shareholder returns over the next five years.

Assessing Alphabet’s Prospects Post-Q4 2023 Earnings Release

To ascertain the trajectory of Alphabet, a re-evaluation through TQI’s Valuation model becomes essential, bolstered by conservative assumptions for long-term growth and margins. With Alphabet currently growing at low to mid-single-digit rates, a re-acceleration to double-digit growth seems implausible, though AI could potentially unlock vast new revenue avenues. Notably, Alphabet’s business resumed an +11% y/y growth in Q3 2023, lending credence to the conservative 10% sales CAGR assumption.

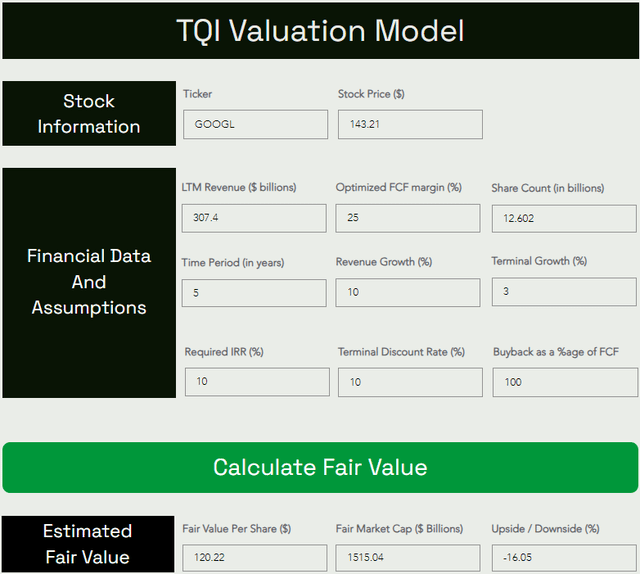

With the ongoing re-acceleration across Alphabet’s segments, particularly in the Cloud segment, the presumed 10% sales CAGR may well prove to be conservative. Thus, steadfastness to the existing model assumptions is warranted.

Alphabet’s fair value is approximately $120 per share (or $1.51T market cap), depicting an overvaluation by ~20% against the current trading price of around $143 per share. However, factoring in the net cash balance nudges the overvaluation slightly. Forecasting a base case P/FCF (exit) multiple of ~20x for 2028, Alphabet’s stock may potentially rise from ~$143 to ~$250 per share at a CAGR rate of 11.77% over the next five years.

However, with Alphabet’s expected CAGR return dipping significantly below the investment hurdle rate of 15%, enthusiasm wanes for purchasing Alphabet at existing levels. Despite this, Alphabet remains a viable option for long-term investors amenable to slightly lower returns (~12% per annum) in exchange for reduced stock volatility.

On a technical note, Alphabet’s stock had been “overbought” going into earnings, with the after-hours pullback representing a necessary reset of technical conditions for GOOGL stock.

Amidst the fluctuations, doubts arise, hinting at the possibility of a considerable corrective pullback down to its fair value of $120 per share in the near-to-medium term. Notwithstanding, the long-term risk/reward from this secular growth compounder remains acceptable, thus maintaining a modest “buy” rating for Alphabet.

Not to mention, Alphabet’s expected 5-year CAGR remaining >10% endorses a slow, staggered accumulation of Alphabet stock, and thus, a steadfast modest “buy” rating is warranted.

If contemplating between Alphabet’s tickers, discerning the better buy becomes imperative:

- GOOG Vs. GOOGL Stock: 2 Ways To Buy Alphabet, One Of Them Is Always Better

Thank you for reading, and may your investment endeavors be fruitful. Please feel free to share your thoughts, concerns, and/or questions in the comments section below.