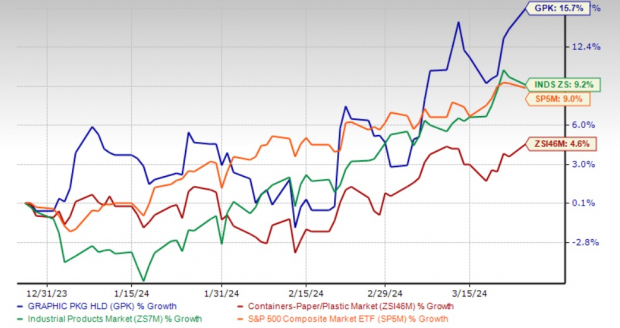

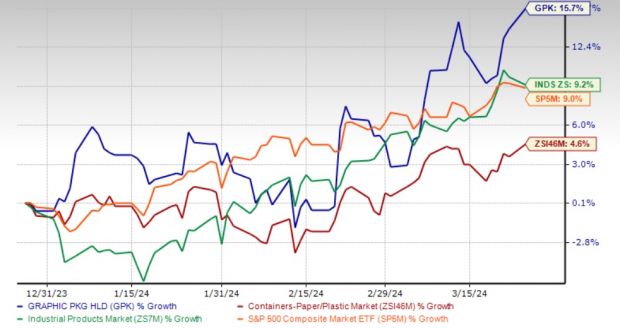

The last three months have been a wild ride for Graphic Packaging Holding Company (GPK), with shares surging 15.7% – a remarkable feat when stacked against the industry’s 4.6% growth. In this relentless tide of the market, the Industrial Products sector rose by 9.2%, while the Zacks S&P 500 composite rode the wave up by 9%.

With a market capitalization hovering around $8.8 billion, GPK proudly carries a Zacks Rank #3 (Hold).

The momentum began building for Graphic Packaging after it released its fourth-quarter 2023 results on Feb 20, 2024. The company reported an impressive 27% year-over-year increase, with fourth-quarter adjusted earnings per share standing at 75 cents. The full year wasn’t too shabby either, with 2023 adjusted earnings per share hitting $2.91, marking a 25% uptick from the previous year.

Image Source: Zacks Investment Research

Despite a 6% and 0.1% year-over-year revenue decline in the fourth quarter of 2023 and 2023, respectively, Graphic Packaging pivoted admirably. Organic sales growth faced a grim negative 4% in 2023, but the company’s strategic maneuvers like higher pricing, cost savings from continuous improvement programs, and new product offerings fueled the surge in earnings.

Recent upticks in volumes have bolstered the company’s outlook, hinting at a return to positive organic sales growth in the current year. Graphic Packaging set its adjusted EBITDA guidance ranging from $1.750 billion to $1.950 billion, with adjusted earnings per share poised between $2.50 to $3.00.

Adding a cherry on top, on Feb 20, Graphic Packaging announced the sale of its Augusta, GA bleached paperboard manufacturing facility to Clearwater Paper for an estimated value of $700 million, contingent upon regulatory nods. The deal is set to close in the second quarter of 2024.

Graphic Packaging’s prowess in churning out innovative fiber-based consumer packaging solutions is a key revenue driver. With a diversified portfolio spanning food & beverage (61%), foodservice (22%), household products (13%), and health care & beauty (4%), the company has positioned itself for solid results.

As consumer demand tilts towards sustainable packaging, Graphic Packaging is stepping up by investing in groundbreaking packaging solutions. Over the past three years, the company has sealed several acquisitions and shows no signs of slowing down on its growth trajectory.

Exploring Promising Stocks

In the Industrial Products sector, stocks like Cadre Holdings, Inc. (CDRE), Applied Industrial Technologies (AIT), and AptarGroup (ATR) shine bright. CDRE flaunts a Zacks Rank #1 (Strong Buy), while AIT and PRLB sport a Zacks Rank #2 (Buy). For an in-depth look at today’s Zacks #1 Rank stocks, explore the complete list here.

The Zacks Consensus Estimate for Cadre Holdings’ 2024 earnings stands at $1.15 per share. Over the past 60 days, the consensus estimate has made a 6% northward journey, suggesting a robust year-over-year growth of 16.7%. With a trailing four-quarter average earnings surprise standing at 33%, CDRE shares have witnessed a 7% uptrend in the last three months.

Applied Industrial showcases a solid trailing four-quarter earnings surprise of 13.9%. Their 2024 earnings are estimated at $9.43 per share, signaling a respectable year-over-year growth of 7.8%. While estimates remained stable for the past 60 days, AIT shares made a 12% leap in the last three months.

AptarGroup’s 2024 earnings estimate per share hits $5.19, with the consensus estimate trending 3% higher over the past 60 days, projecting an 8.6% year-over-year growth. The company boasts a trailing four-quarter average earnings surprise of 7.8%, coupled with a 14% share upturn over the past year.

Investing in Potential Winners

These are the top picks selected by Zacks experts as the #1 favorite stocks poised to gain over 100% in 2024. Prior recommendations have witnessed impressive surges of +143.0%, +175.9%, +498.3%, and +673.0%.

Flying under Wall Street’s radar, these stocks present a golden opportunity to enter the market early.

Discover These 5 Potential Moneymakers Today >>

The perspectives articulated herein represent the thoughts and opinions of the author alone and do not necessarily mirror those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.