Hancock Whitney Corp. is navigating through a tumultuous financial landscape, capitalizing on the surge in loan demand amidst escalating expenses. The company’s strategic positioning, bolstered by robust interest rates and calculated expansion moves, has generated a wave of revenue growth, alleviating concerns surrounding its expense structure and the sluggish mortgage banking sector.

Riding the Loan Demand Wave: A Strategy for Growth

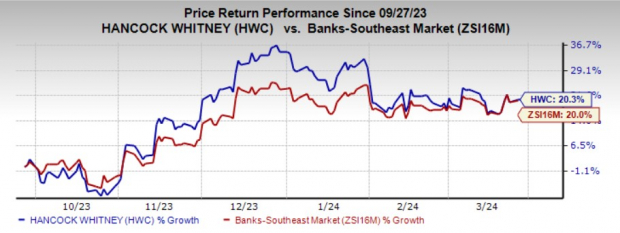

With a keen eye on expanding its revenue streams, Hancock Whitney orchestrated the acquisition of MidSouth Bancorp in 2019, a move that significantly boosted its financial standing. The ensuing five-year compound annual growth rate (CAGR) for revenues (tax-equivalent basis) stood at an impressive 4%, aligning with a 3.6% CAGR for total loans.

The company is poised for sustained top-line expansion, driven by the interplay of high interest rates, burgeoning loan requests, and well-orchestrated fee income enhancement strategies. Projections paint a promising picture, with anticipated revenue and total loan CAGRs of 2.7% and 2.1% over the upcoming three-year period until 2026.

Battle of the Margins: Navigating High Costs

Despite witnessing the elevation of its net interest margin (NIM) to 3.34% in 2023, Hancock Whitney faced headwinds in the form of escalating funding costs. This situation, compounded by the Federal Reserve’s stance on maintaining high rates, exerted pressure on the NIM expansion rate. However, the company’s strategic maneuvers, encompassing bond restructuring and balance sheet optimization, are set to revitalize NIM growth, with management eyeing a incremental uptick in coming years.

Staying Afloat: Capital Sustainability Amidst Stormy Seas

By reporting total debt figures of $1.39 billion as of December 2023, with a substantial portion being short-term borrowings, Hancock Whitney has fortified its capital structure. Accompanied by investment-grade ratings from leading agencies and a robust liquidity foundation, the company is well-equipped to navigate economic uncertainties while meeting its near-term financial obligations seamlessly.

Optimism on the Horizon: Capital Distribution and Investment Outlook

Hancock Whitney’s upbeat capital distribution plans, including an elevating quarterly dividend trajectory and an ongoing share repurchase program, underscore its long-term financial stability. The company’s diligent focus on maintaining a strong liquidity position augurs well for its sustained commitment to rewarding shareholders and steering through market vagaries.

Challenges Ahead: Wrangling with Mortgage Banking and Rising Costs

However, the outlook for Hancock Whitney’s mortgage banking segment appears cloudy, with volatile mortgage rates contributing to a decline in secondary mortgage income. Moreover, the company is contending with persistent concerns related to its elevated expense structure, influenced by inflationary pressures, strategic expansion endeavors, and technological investments.

Exploring Alternatives: Diversifying Investment Portfolios

Investors eyeing potential opportunities in the banking sector might find solace in exploring other top-performing stocks like Bank7 Corp. and Popular Inc., each boasting a Zacks Rank of 1 (Strong Buy). The buoyant financial performances of these entities underscore a consistent growth trajectory and promising returns for prospective investors.