Flowserve Corporation FLS stands to benefit from strength across its businesses, focus on operational excellence and a sound liquidity position. The company remains focused on investing in growth opportunities and strengthening its long-term market position.

Image Source: Zacks Investment Research

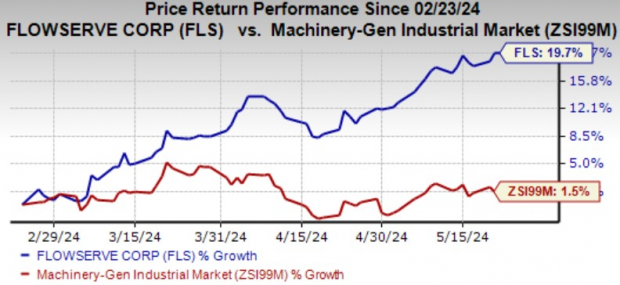

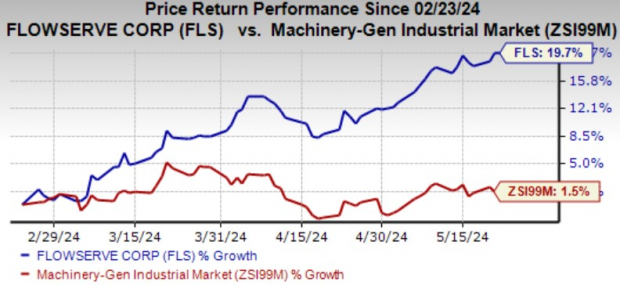

It has a market capitalization of $6.6 billion. Over the past three months, it has gained 19.7% compared with the industry’s 1.5% growth. FLS currently carries a Zacks Rank #2 (Buy).

Let’s delve into the factors that have been aiding the firm for a while now.

Solid Booking Level: The company has been benefiting from robust bookings driven by strong maintenance, repair, operations and aftermarket activity. Solid booking levels supported by strong demand for bill and gas, and chemicals augur well for the company. FLS’ Diversify, Decarbonize and Digitize strategy has also been supporting its growth. Notably, its first-quarter 2024 bookings of $1.04 billion marked the ninth consecutive quarter of more than $1 billion bookings.

Business Strength: Solid momentum in the original equipment and aftermarket businesses are supporting both the Flowserve Pump Division (revenues increased 9.9% year over year in the first quarter) and Flow Control Division (revenues grew 13.8% year over year in the first quarter) segments. For 2024, the company projects revenues to grow in the range of 4-6% from the year-ago levels. It anticipates adjusted earnings per share between $2.50 and $2.70.

Shareholder-Friendly Policies: Management remains focused on rewarding its shareholders through dividend payouts. The company paid dividends of $105 million in 2023. In the first quarter, it used $27.7 million for distributing dividends.

Solid Liquidity Position: In the first three months of 2024, the company generated net cash of $62.3 million from operating activities, up from $26.6 million in the year-ago period. Exiting the first quarter, its cash and cash equivalents were $532 million, much higher than the current maturities of $66.4 million.

However, Flowserve has been grappling with escalating costs and expenses over time. In 2023, its cost of sales jumped 16.1% year over year due to higher input costs. Also, the metric jumped 9.5% year over year in the first quarter of 2024 due to higher input costs.

Other Stocks to Consider

Some other top-ranked stocks from the same space are discussed below.

Luxfer Holdings LXFR presently sports a Zacks Rank #1 (Strong Buy). It has a trailing four-quarter average earnings surprise of 122.5%. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for LXFR’s 2024 earnings has increased 13.5% in the past 60 days.

Crane Company CR presently carries a Zacks Rank of 2. It delivered a trailing four-quarter average earnings surprise of 15.2%.

In the past 60 days, the Zacks Consensus Estimate for CR’s 2024 earnings has risen 3.3%.

Tennant Company TNC currently carries a Zacks Rank of 2. TNC delivered a trailing four-quarter average earnings surprise of 38%.

In the past 60 days, the Zacks Consensus Estimate for its 2024 earnings has inched up 1.9%.

Free – 5 Dividend Stocks to Fund Your Retirement

Zacks Investment Research has released a Special Report to help you prepare for retirement with 5 diverse stocks that pay whopping dividends. They cut across property management, upscale outlets, financial institutions, and a couple of strong energy producers.

5 Dividend Stocks to Include in Your Retirement Strategy is packed with unconventional wisdom and insights you won’t get from your neighborhood financial planner.

Download Now – Today It’s FREE >>

Flowserve Corporation (FLS) : Free Stock Analysis Report

Crane Company (CR) : Free Stock Analysis Report

Luxfer Holdings PLC (LXFR) : Free Stock Analysis Report

Tennant Company (TNC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.