Illinois Tool Works Inc. ITW has been reaping the benefits of a sturdy presence in the Automotive OEM segment and proactive enterprise strategies, even amid challenges like a sluggish semiconductor market and currency fluctuations.

Driving Forces Behind ITW’s Success

Business Resilience: Illinois Tool Works has thrived on consistent demand and optimized supply chains. Remarkable market share and expansion strides in the burgeoning EV sector fuel revenue growth in the Automotive OEM division. Concurrently, the Food Equipment segment prospers from upswings in institutional, retail, and service end markets.

Fueled by robust segmental performances, the corporation has issued a favorable outlook for 2024. ITW anticipates organic revenue growth of 1-3% and total revenue ascent of 2-4% year over year in 2024. Additionally, the company projects adjusted earnings per share for 2024 to range from $10.00-$10.40, reflecting a 5.1% increase at the midpoint.

Strategic Focus: The company’s concentration on cost efficiency and enterprise initiatives bolsters its margin metrics. Notably, in 2023, ITW witnessed a 1.2% reduction in the cost of sales year over year. During the same period, the operating margin escalated by 130 basis points to 25.1%, with enterprise initiatives contributing 130 basis points. For 2024, ITW projects an operating margin in the 25.5–26.5% range, compared to 25.1% in 2023, with enterprise initiatives expected to contribute 100 basis points to the margin.

Hands-on Returns: ITW remains dedicated to rewarding its shareholders generously. In 2023, the company disbursed dividends totaling $1.6 billion and repurchased 6.4 million common stock shares for roughly $1.5 billion. Furthermore, ITW raised its dividend by 7% to $1.40 per share in August 2023, alongside greenlighting a new $5 billion buyback initiative.

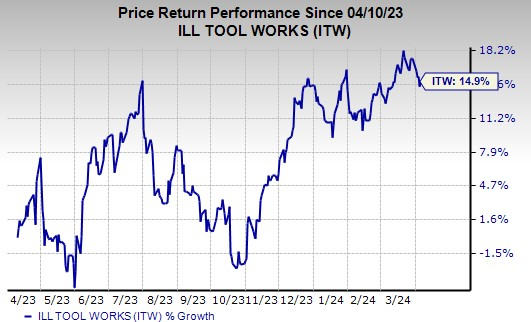

In light of these evident positives, retaining ITW stock, as indicated by its current Zacks Rank #3 (Hold), appears prudent. Over the past year, the stock has surged by 14.9%.

Image Source: Zacks Investment Research

Stocks to Watch

Consider looking into these promising companies from the Industrial Products sector:

Applied Industrial Technologies, Inc. AIT currently boasts a Zacks Rank #1 (Strong Buy) with a four-quarter average earnings beat of 10.4%. Their fiscal 2024 earnings estimate has surged by 2.5% in the last 60 days, with the stock witnessing a 48.3% climb in the last year.

Belden Inc. BDC carries a Zacks Rank #2 (Buy) alongside a solid average earnings surprise of 12.3% over the past four quarters. Earnings estimates for 2024 have remained steady, with the stock showing a 10.5% uptick in the past year.

A. O. Smith Corporation AOS, holding a Zacks Rank of 2, boasts a remarkable four-quarter earnings surprise average of 12%. Their 2023 earnings estimate has grown by 0.5% in the last 60 days, and the stock has soared by 33.7% in the past year.

5 Stocks Set to Double

Handpicked by a Zacks analyst, these top-rated stocks are primed to achieve over 100% growth in 2024. With an impressive track record of recommendations soaring by +143.0%, +175.9%, +498.3%, and +673.0%, this report unveils remarkable opportunities often overlooked by Wall Street.