Williams-Sonoma, Inc. WSM continues to thrive due to its resilient operating model, robust e-commerce platform, and strategic B2B endeavors. The company’s digital focus and global outreach plans are propelling it toward success, especially in emerging markets like India, where the brand’s growth has exceeded expectations.

Yet, amidst its upward trajectory, concerns loom over macroeconomic fluctuations and geopolitical tensions, potentially affecting the company’s growth trajectory.

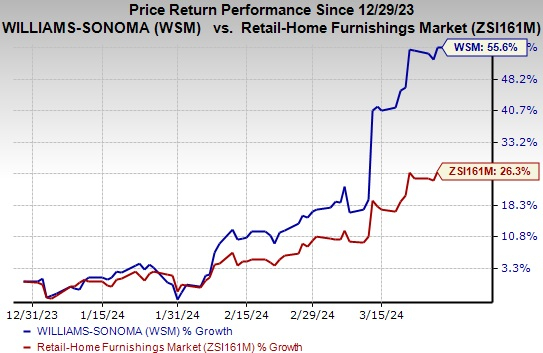

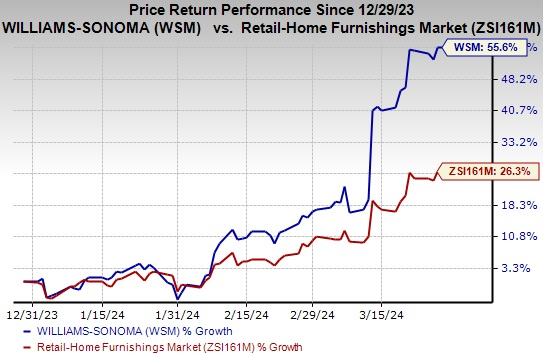

Over the past three months, this premium home products’ multi-channel retailer has surged by 55.6%, outperforming the Retail – Home Furnishings industry’s growth of 26.3%. Analysts predict an upward trend, with the Zacks Consensus Estimate for fiscal 2025 earnings for this Zacks Rank #3 company climbing to $15.37 per share from $14.69 in the last month, indicating a solid growth trajectory.

Image Source: Zacks Investment Research

The company’s positive outlook is underscored by its impressive VGM Score of A, driven by an A in Momentum and Growth, and a B in Value. This favorable rating reflects optimistic analyst sentiment, sturdy fundamentals, and an expected sustained outperformance in the short term.

Factors Fueling Growth

Focus on E-commerce Channel: Williams-Sonoma has emerged as one of the leading e-commerce retailers in the United States. Its commitment to innovation has led to significant e-commerce growth. The company’s e-commerce penetration is on the rise, supported by its cutting-edge tech platform, rapid experimentation initiatives, content-rich online presence, and targeted marketing efforts.

With a core focus on enhancing its retail business, Williams-Sonoma continues to elevate in-store experiences by offering inspirational products and top-notch design services. The company’s ongoing efforts to optimize its retail presence have resulted in streamlining its locations for profitability and strategic positioning.

Looking ahead to 2024, WSM’s capital allocation strategy prioritizes investments in business operations and long-term expansion. A considerable portion of the $225 million planned capital expenditure is allocated toward bolstering its e-commerce dominance and refining supply chain efficiency.

Digitalization Efforts: Delving into the digital realm, Williams-Sonoma diligently manages ad expenses, channeling investments into productive avenues while allowing room for experimentation with engaging formats to reach new audiences. As a major player in the e-commerce arena, the company is continuously enhancing its proprietary e-commerce technology stack, positioning itself as a tech leader in the retail sector through the integration of AI in tech capabilities.

Noteworthy progress was witnessed in WSM’s Canada business during the fourth quarter of fiscal 2023, driven by a relentless focus on enhancing the online and in-store customer experience. The company’s digital initiatives in Canada are generating traction, attracting fresh clientele and delivering positive outcomes for its brands. As Williams-Sonoma expands its omnichannel footprint globally, countries like India, Mexico, and Canada emerge as pivotal growth hubs.

B2B Strategy Driving Growth: Bolstering its growth agenda, B2B remains a cornerstone of Williams-Sonoma’s strategy. The company operates in both trade and contract segments, witnessing a remarkable 31% increase in its contract business in fiscal 2023 despite an overall 1% year-over-year business growth. The upsurge was propelled by strong performance in hospitality and residential sectors, with promising developments in burgeoning areas like health care, gaming, and senior living indicating further growth potential. The company is steadfast in its efforts to expedite its contract business expansion, exhibiting encouraging momentum.

Challenges Ahead

Williams-Sonoma’s performance is currently impacted by mounting occupancy costs, coupled with escalating operational and general expenses. Additionally, global geopolitical uncertainties pose ongoing challenges for the company.

In fiscal 2023, selling, general, and administrative expenses, as a percentage of net revenues, rose to 26.6% from 25.1% in fiscal 2022. This uptick can be attributed to escalating employment costs, driven by higher performance-based incentives in fiscal 2023 compared to the previous year, aligning with business performance.

Continued macroeconomic pressures are weighing on WSM’s global operations. As the company eyes 2024, sustained macroeconomic ambiguity is anticipated. While lower interest rates could potentially stimulate the housing sector and redirect consumer spending to home-related purchases, the timing and impact of these factors remain uncertain. Variables like global geopolitical tensions and the upcoming election further contribute to this air of uncertainty.

Top Recommendations

Here are some top contenders in the Retail-Wholesale sector:

Brinker International, Inc. EAT holds a Zacks Rank #1 (Strong Buy), boasting an average trailing four-quarter earnings surprise of 212.7%. EAT shares have surged by 36.6% in the past year, with promising growth prospects indicated by the Zacks Consensus Estimate projecting a 4.9% rise in 2024 sales and a 30.7% upsurge in EPS compared to the prior year.

Texas Roadhouse, Inc. TXRH, holding a Zacks Rank #2 (Buy), indicates a trailing four-quarter average negative earnings surprise of 3.9%. However, its stock has seen an impressive 42.9% uptick in the last year, with the Zacks Consensus Estimate suggesting a 14% increase in 2024 sales and a 25.1% rise in EPS from the corresponding period in the previous year.

Shake Shack Inc. SHAK carries a Zacks Rank #2, with a trailing four-quarter average earnings surprise of 92.6%. SHAK shares have soared by 93.8% over the past year, and the Zacks Consensus Estimate anticipates a 14.6% surge in 2024 sales and a remarkable 91.9% growth in EPS compared to the year-ago period.

Zacks Reveals ChatGPT “Sleeper” Stock

One little-known company is at the heart of an especially brilliant Artificial Intelligence sector, slated to have a monumental economic impact of $15.7 Trillion by 2030.

Providing an exclusive report, Zacks reveals this explosive growth stock and four other essential picks. Plus more.

Download Free ChatGPT Stock Report Right Now >>

The opinions expressed in this article belong to the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.