Rayonier Inc. radiates promise with its timberland portfolio sprawled across prime timber-growing havens in the United States South, the Pacific Northwest, and New Zealand. Bright-eyed analysts are optimistic about this Zacks Rank #2 (Buy) gem, especially with the Zacks Consensus Estimate for the company’s 2024 earnings per share sweetly climbing 2.1% to 48 cents in the past month.

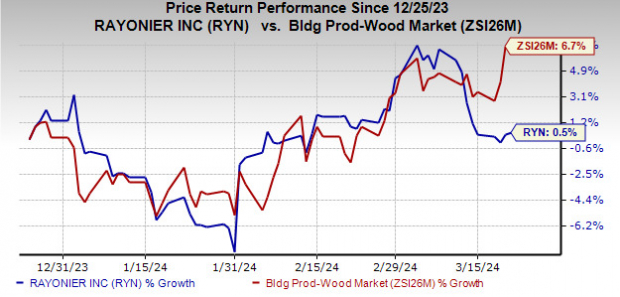

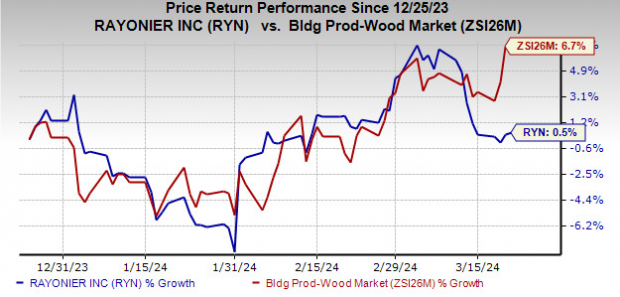

Despite only a 0.5% rise in RYN’s shares over the past three months compared to the industry’s 6.7% surge, the sturdy fundamentals of this company forecast significant growth, making any downturn a potential doorway of opportunity.

Image Source: Zacks Investment Research

Rayonier’s Timber Tale

Rich Harvest & Market Magic: Rayonier stands tall as the premier “Pure Play” timber REIT, deriving a hefty 74% of its 5-year average EBITDA from timber operations, unlike the peer group’s modest 27%. With a sprawling portfolio encompassing 1.85 million acres in the U.S. South, 418,000 acres in the U.S. Pacific Northwest, and 421,000 gross acres in New Zealand, Rayonier’s oak roots run deep.

The company is well-positioned to reap the fruits of the burgeoning lumber production in the U.S. South. Though the markets may see a mild demand lull, the upcoming period spells a construction catharsis, potentially fueling pricing in the Pacific Northwest. A twinkle of 2.5% is anticipated in adjusted EBITDA for 2024.

Forest Finesse: Rayonier is a master conductor, orchestrating harmonious symphonies across its timberlands with a keen eye on alternative High-and-Better-Use (HBU) development potentials. The golden zones of Florida and Georgia’s coastal corridor beckon, promising long-term value unlock for this timber titan.

Biogenetic Boon & Cloning Chronicles: Rayonier’s foliage flourishes amidst the biogenetic and cloning revolutions, nurturing accelerated tree growth to deliver optimal wood extraction rates.

Fortified Finances: Rayonier boasts a robust balance sheet with $207.7 million of cash reserves exiting the fourth quarter of 2023. A solid credit rating ensures favorable debt market access, underpinned by its BBB-/Stable rating from S&P and Baa3/Stable rating from Moody’s, providing a springboard for future growth pursuits.

Finding the Forest Through the Trees

A Grove of Opportunities: In a playground rich with budding stocks, do consider flourishing prospects like Host Hotels & Resorts and Iron Mountain, both flaunting a Zacks Rank #1 (Strong Buy) label. Host Hotels & Resort’s 2024 FFO per share stands at an anticipated $1.97, spelling out a growth melody of 2.6%. Similarly, Iron Mountain’s 2024 FFO per share envisions a 7.3% uptick to $4.42.

Note: The earnings reflected in this piece allude to funds from operations (FFO), a key metric in the REIT realm.

Kindly note, dear investors, that the insights here reflect the author’s views and not the Nasdaq, Inc.