Investors can rejoice as Huntsman Corporation (HUN) stands tall amid challenging times, fortified by its strategic investments in downstream businesses and pioneering product innovation. Emerging like a sturdy oak tree in a storm, Huntsman persists despite headwinds from demand softness and pricing pressures.

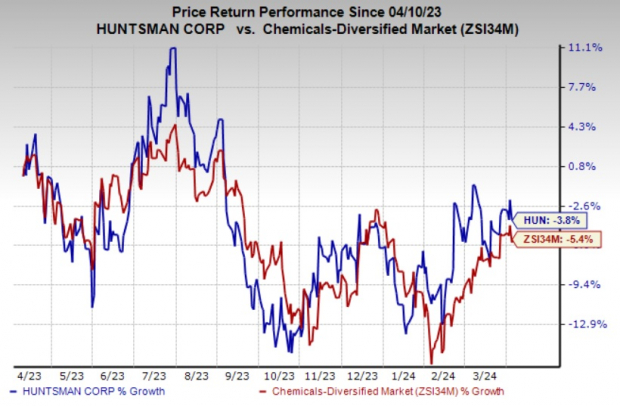

The journey so far has been a rollercoaster, with the company’s shares witnessing a modest 3.8% decline over the past year, outperforming its industry’s 5.4% dip.

Image Source: Zacks Investment Research

Let’s delve into why this Zacks Rank #3 (Hold) stock remains a valuable asset in the current climate.

Navigating Downstream Expansion & Synergies

Huntsman persists in enhancing its downstream specialty and formulation businesses, transitioning its MDI business to sophisticated systems with elevated margins and lower volatility. Like a craftsman honing his masterpiece, Huntsman refines its Polyurethanes segment, poised for exponential growth by expanding its high-value differentiated downstream portfolio. The company’s focus on substituting MDI with superior materials proves to be a vital catalyst for the MDI unit.

The acquisitions of CVC Thermoset and Gabriel Performance Products have further boosted Huntsman’s Advanced Materials segment. These strategic moves have enabled the company to realize over $280 million in run rate savings by 2023, with an additional $60 million anticipated this year through a relentless pursuit of cost efficiencies.

With a hawkish eye on expanding margins and driving returns to shareholders, Huntsman repurchased approximately 2.1 million shares in Q4 2023, underlining its commitment to maximizing value. The recent increment in quarterly dividend marks its dedication to shareholder rewards.

Challenges Amid Soft Demand & Pricing Woes

However, Huntsman faces hurdles stemming from softened demand, notably stemming from the tumultuous economic environment in Europe and Asia. The ripple effects of weakened construction activities and pandemic-induced restrictions continue to hamper growth prospects.

Moreover, the brutal pressure of competitive pricing looms large over Huntsman, evident in lower selling prices across its segments, thereby impacting margins in the latest quarter.

A Glimpse into Potential:

While Huntsman maneuvers through these turbulent waters, there are other shining stars in the basic materials landscape worthy of attention. Companies like Carpenter Technology Corporation (CRS), Denison Mines Corp (DNN), and Innospec Inc (IOSP) present compelling cases for consideration.

The growth prospects for these entities are promising, setting the stage for potential substantial returns.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.