The homebuilding sector, akin to a slumbering giant, is awakening from a prolonged hibernation. Engulfed in a two-year torpor induced by the Federal Reserve’s unyielding interest rate hikes, the industry now shows signs of life.

Surging mortgage rates and escalating costs of raw materials and labor delivered a series of punches to the gut of the homebuilding market. Potential buyers stood on the sidelines, cautious in the face of robust demand but prohibitive expenses.

Positive Growth Triggers

However, a silver lining emerged as the clouds of recession began to dissipate. With inflation rates ebbing, the Fed put a halt to its interest rate ascent in July of 2023. Moreover, during the March FOMC meeting, whispers of three forthcoming rate cuts of 25 basis points each in 2024 set hearts aflutter.

The prospect of a lower risk-free market interest rate heralded a decline in mortgage rates since November 2023. This descent bears ripe fruit for homebuyers and sellers alike, breathing fresh air into the industry and infusing it with vitality.

According to the Commerce Department’s insightful data from March 19, housing starts leaped by a notable 10.7% in February, surpassing market expectations and painting a vivid picture of growth. Not to be outdone, residential building permits followed suit, climbing 1.9% in the same month, signaling positive momentum in construction activities.

After over a decade of under-building relative to population expansion, the lacuna of new homes widened, creating a fertile ground for profits amidst high mortgage rates and low supply.

Efficient Cost Strategies

Faced with a surge in raw material prices, industry players embarked on a voyage of cost control, steering their ships towards newfound efficiency. By optimizing their construction processes and negotiating competitive rates for materials and labor, they navigated the stormy seas of financial uncertainty and discovered the beacon of higher operating leverage.

Many firms targeted the burgeoning demand for entry-level homes, addressing affordability concerns in the U.S. housing market. Through strategic acquisitions and a shift towards dynamic pricing models, companies sought to enhance their market presence and bolster profitability.

Leading Contenders

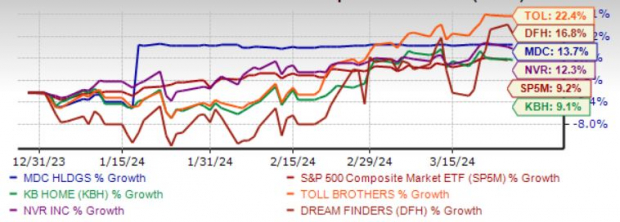

In the realm of promising homebuilders, five stand out as the vanguards of growth for 2024. These handpicked entities have witnessed upward revisions in earnings estimates over the past 60 days, each brandishing either a Zacks Rank #1 (Strong Buy) or 2 (Buy).

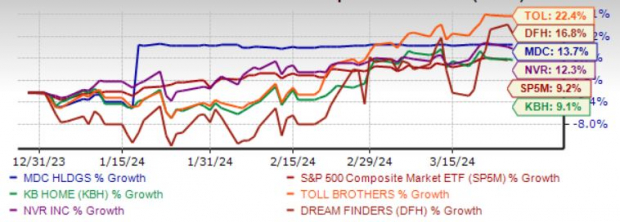

The accompanying chart illustrates the year-to-date price performance of these elite five.

Image Source: Zacks Investment Research

Toll Brothers Inc. embarks on a journey marked by enhanced market demand and a commitment to expanding its supply of spec homes while honing operational efficiency. Their strategic focus on affordable luxury communities and a build-to-order approach augur well for the future.

Since the dawning of spring amidst mid-January, Toll Brothers Inc. has witnessed a surge in demand. Foreseeing an upward trajectory, the company aims for home deliveries of 10,000-10,500 units in fiscal 2024, an upswing from the previous fiscal year.

The enigmatic NVR Inc. has harnessed the prevailing scarcity of existing homes and reduced average selling prices of new orders to drive growth momentum. With a business model centered around acquiring finished building lots, the company navigates the cyclical industry landscape with finesse.

Dream Finders Homes Inc., a beacon of hope in the homebuilding firmament, dazzles with its diversified brand portfolio catering to varied needs in the market. Through a blend of innovation and astute market insights, the company charts a path to sustained growth.

The resilient KB Home flourishes by embracing the build-to-order model and curating a bouquet of mortgage concessions. With a keen eye for improving cycle times and stimulating demand, the company anticipates an uptick in housing revenues for fiscal 2024.

The Resilience of M.D.C. Holdings Inc. in the Homebuilding Market

Strategic Shifts Fuel Profitability

M.D.C. Holdings Inc., or MDC, has demonstrated remarkable resilience in a tumultuous market, enjoying a stock increase of 2.6% in the last week. This ascension is no stroke of luck but the result of astute strategic maneuvers. The company has deftly adapted to the challenging economic landscape by concentrating on entry-level homes. By pivoting towards a more spec-driven model, MDC has cleverly aligned itself with the demands of first-time homebuyers.

Enticing Opportunities for Buyers

Moreover, MDC is not content with mere mediocrity but strives for excellence. The provision of enticing opportunities for build-to-order buyers, such as long-term interest rate lock programs and special incentives, showcases the company’s commitment to customer satisfaction. This unwavering dedication to customer needs sets MDC apart in the fiercely competitive homebuilding market.

Robust Growth Prospects

Ranked as a strong Zacks Rank #2 company, M.D.C. Holdings is not resting on its laurels. With an anticipated revenue growth rate of 7.1% and an earnings growth rate of 1.7% for the current year, MDC continues to forge ahead. The Zacks Consensus Estimate for current-year earnings has even seen a positive uptick of 2.1% over the past two months, signaling a promising trajectory for the company.

Looking Towards the Future

While the homebuilding market has weathered its fair share of storms, MDC’s steadfastness remains unwavering. As the company navigates the ever-changing landscape, its land acquisition strategies and high liquidity provide a solid foundation for future growth. These initiatives, coupled with a sharp focus on customer needs and a proactive approach to industry challenges, position MDC as a force to be reckoned with in the market.