# Semiconductor Industry Thrives Amid Technological Advancements and Market Dynamics

Companies in the Semiconductor – General industry are at the forefront of a technological revolution driven by high-performance computing (HPC), artificial intelligence (AI), electrified and automated driving, and the Internet of Things (IoT). The semiconductors produced by these firms are essential for cloud operations and transforming large volumes of data into actionable insights that enhance operational efficiency. This robust growth outlook has led to rising share prices and strong valuations. Despite potential recession concerns, companies like NVIDIA Corp. (NVDA) and Texas Instruments (TXN) remain strong contenders in the market.

Additionally, 2024 is exhibiting better-than-expected results. This can be attributed to the semiconductor and technology sectors, which play a crucial role in counterbalancing broader economic slowdowns. Recent reports from WSTS, often cited by the Semiconductor Industry Association (SIA), indicate that global semiconductor sales are expected to grow by 11.2% this year, building on a 19% increase in 2024.

IDC forecasts double-digit growth fueled by the demand for high-end logic process chips and high-bandwidth memory (HBM) driven by AI workloads. The capacity for advanced nodes (below 20nm) is projected to rise by 12%, with utilization rates remaining above 90%. Most growth activity is anticipated in Taiwan, the U.S., and Korea.

In terms of mature nodes, utilization is expected to increase from 70% in 2024 to over 75% this year. Wafer production is predicted to rise by 7%. Gartner forecasts a 13.8% uptick in semiconductor sales this year, following an 18.8% increase in the previous year, primarily due to a steady demand for AI-related semiconductors and a rebound in electronics manufacturing, despite lingering weaknesses in automotive and industrial markets.

Looking at end-markets, PC growth will also be driven by AI innovations and the phase-out of Windows 10 support, leading to increased deployment in commercial and enterprise settings. Furthermore, the IoT market is set for steady growth driven by improved Internet connectivity and technology advancements such as sensor networks and AI adoption globally.

According to iMARC, the industrial IoT (IIoT) sector alone is expected to grow at a compound annual growth rate (CAGR) of 12.7% from 2025 to 2033. By 2025, Gartner predicts that 25% of industrial companies will either adopt or invest in an industrial IoT platform. Combined, AI and IoT will continue to revolutionize industrial operations, driving major shifts in auto electrification, industrial automation, and data center efficiency. The potential for semiconductor growth appears expansive.

The U.S. government’s efforts to reduce reliance on China and onshore critical manufacturing will have significant implications for this industry.

About the Industry

The companies within the Semiconductor – General category develop a wide array of semiconductor devices, both integrated and discrete. This includes microprocessors, graphics processors, embedded processors, chipsets, motherboards, and connectivity products, serving various end-markets. Key players include NVIDIA, Texas Instruments, Intel, and STMicroelectronics.

Major Themes Shaping the Industry

- Artificial Intelligence (AI) as the Primary Driver: AI stands as the leading force behind growth in the semiconductor industry, enhancing efficiency, cost-effectiveness, and safety across sectors. With ongoing advancements in machine learning and urbanization, semiconductor demand looks set to increase for years, positioning AI technology as a vital investment across industries.

- Geopolitical Factors Favoring Growth: Current geopolitical tensions amplify semiconductor demand as countries seek cutting-edge technology for defense and infrastructure. The U.S.-China tariff battle and concerns about Taiwan as a manufacturing hub add urgency to onshoring initiatives. The CHIPS Act is facilitating domestic semiconductor production in response to these security concerns.

- Economic Concerns and Consumer Behavior: Although the long-term outlook remains positive, near-term macroeconomic challenges are evident. Tariffs are impacting consumer confidence, offsetting benefits from low inflation and interest rates. The automotive electronics segment is evolving with the shift to electric vehicles (EVs), but declining consumer confidence may hinder demand for premium offerings. Automation trends are promising, yet the industrial sector remains vulnerable to economic fluctuations.

- Supply Chain Adjustments: Semiconductor supply chains have improved efficiency over the years. However, reliance on just-in-time models has made them susceptible to external disruptions, such as those during the pandemic. Consequently, companies are diversifying supply chains to reduce dependence on China, a process expected to unfold over several years.

Zacks Industry Rank Indicates Positive Prospects

The Zacks Semiconductor-General Industry is part of the broader Computer and Technology sector, holding a Zacks Industry Rank of #92, placing it in the top 37% of nearly 250 industries classified by Zacks.

This rank reflects the average performance of the member stocks and suggests favorable near-term prospects for the industry.

Positive Outlook for Semiconductor Industry Amid Strong Earnings Growth

Prospects for the semiconductor industry are improving. Research reveals that the top 50% of Zacks-ranked industries outperform the bottom 50% by a factor of 2 to 1. An industry’s position in the top 50% indicates a strong aggregate earnings outlook for its companies, while the reverse applies to the bottom 50%. For example, the aggregate earnings estimate for 2026 has increased by 35.1% compared to last year, and estimates for 2027 reflect a 55.5% rise.

Before highlighting some noteworthy stocks, let’s review the recent performance and valuation of the semiconductor sector.

Strong Stock Market Performance

The Zacks Semiconductor – General Industry has shown robust performance over the past year, consistently trading at a premium compared to both the broader Zacks Computer and Technology Sector and the S&P 500 index. This industry has gained 22.5% in the past year, surpassing the technology sector’s 8.1% increase and the S&P 500’s 10% gain.

One-Year Price Performance

Image Source: Zacks Investment Research

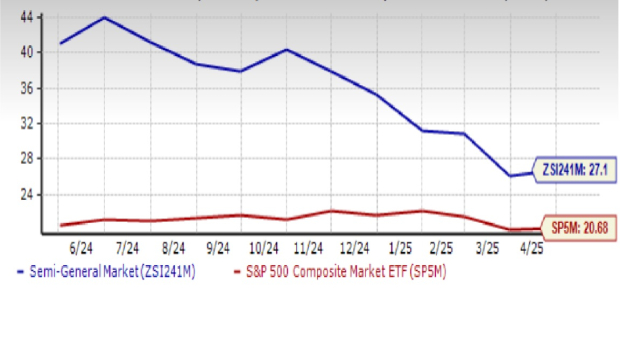

Current Valuation: Industry Appears Overvalued

Analyzing the forward 12-month price-to-earnings (P/E) ratio, the industry is currently trading at a multiple of 27.10X. While this is below its median value of 37.86X, it significantly exceeds the S&P 500’s 20.68X and the sector’s 23.70X valuation, suggesting overvaluation.

Over the last decade, the industry’s valuation closely aligned with the sector, initially trailing behind, followed by slight outperformance. However, since mid-2022, the industry has surged, likely due to heightened demands for foundational technologies in AI, autonomous driving, and defense.

Forward 12 Month Price-to-Earnings (P/E) Ratio

Image Source: Zacks Investment Research

Stock Picks for Consideration

The semiconductor industry remains promising and benefits from anticipated interest rate cuts, which typically draw more investment into riskier assets. Key technology firms in this space are fundamental to modern computing, fostering optimism for long-term growth, although valuation concerns persist. Notably, we recommend close attention to NVIDIA and Texas Instruments.

NVIDIA Corp. (NVDA)

Based in Santa Clara, California, NVIDIA specializes in graphics, compute, and networking solutions across various markets. Renowned for its dominant position in the gaming GPU sector, NVIDIA is also a leader in enterprise, data center, cloud, and automotive technology.

The rise of generative AI is significantly boosting computing needs, with a shift towards NVIDIA’s energy-efficient products. Its offerings, including GPUs and AI enterprise software, are driving growth opportunities globally. Major cloud service providers such as AWS, Microsoft Azure, and Google Cloud Platform are among NVIDIA’s largest customers.

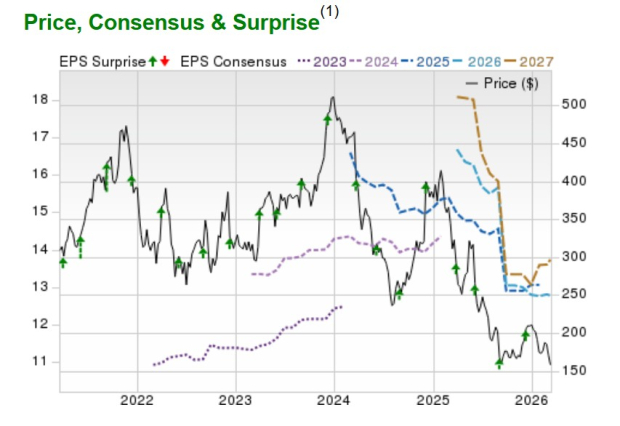

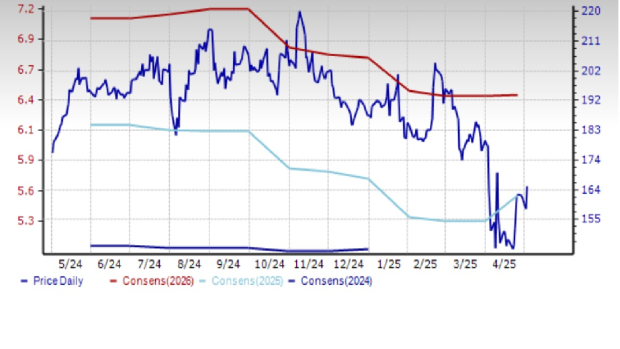

In recent months, the Zacks Consensus Estimate for 2026 earnings has slightly dipped to $4.24, down 3.9% from earlier projections. Nonetheless, projections indicate a robust 48.2% revenue growth and a 41.8% earnings increase for 2026, followed by 24.2% revenue and 26.7% earnings growth in 2027. Currently rated Zacks Rank #3 (Hold), NVIDIA’s stock has increased by 30.1% in the past year.

Price & Consensus: NVDA

Image Source: Zacks Investment Research

Texas Instruments, Inc. (TXN)

Headquartered in Dallas, Texas Instruments manufactures analog and embedded processing chips utilized across various applications, including industrial and automotive sectors. While the U.S. is its primary market, China accounts for nearly 20% of revenues, subject to geopolitical fluctuations.

In response to supply chain disruptions from the pandemic and evolving geopolitics, TI has shifted its manufacturing strategy to internalize wafer production, aiming for over 95% self-sourcing by 2030. The company is expanding its manufacturing capabilities, with significant investments related to U.S. semiconductor production incentivized by government support.

Initially, capacity expansion can negatively impact margins due to underutilization. However, TI has improved its direct sales to customers, enhancing insights into projects and driving market share gains. With projections indicating 2025 revenues and earnings growth of approximately 11.0% and 6.7%, respectively, followed by an 8.8% revenue and 13.9% earnings increase in 2026, the stock maintains a promising outlook.

This Zacks Rank #3 stock remains a worthy consideration in a competitive market landscape.

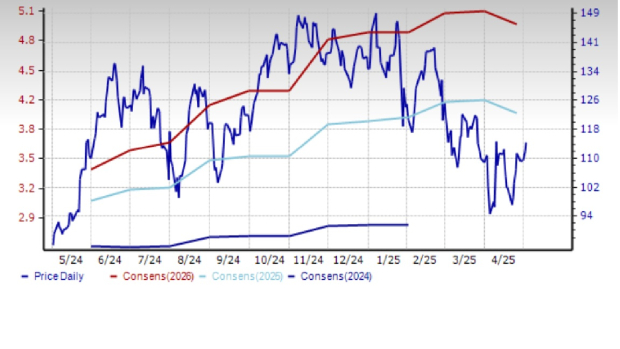

# Texas Instruments Faces 10% Decline Amid Market Fluctuations

## One-Year Price Performance Overview: TXN

Texas Instruments Incorporated (TXN) has recently seen its stock price slump by 10%. Analysts are closely monitoring the company’s fluctuations as they assess its longer-term performance.

Image Source: Zacks Investment Research

## Insights on Investment Opportunities

In the current market, five stocks have been identified with the potential to double in value. These selections are handpicked by industry experts, aiming for substantial gains of 100% or more in 2024. Historical recommendations have already seen impressive surges, with previous gains recorded at +143.0%, +175.9%, +498.3%, and +673.0%.

Investors may find enticing prospects among stocks that remain under the radar, presenting an opportunity for early investment.

## Additional Resources

For those interested in exploring potential growth stocks, further insights and recommendations can be found through various financial platforms. Staying informed about trending stocks and market shifts can help guide investment strategies.

**Disclaimer:** The views expressed in this article represent the author’s perspectives and do not necessarily reflect those of Nasdaq, Inc.