Hewlett Packard Enterprise Company shareholders faced a turbulent Tuesday as the tech giant’s stock plummeted by 8.5%. The trigger? A startling $1.35 billion stock offering intended to finance its upcoming acquisition of Juniper Networks, Inc. JNPR. This unexpected move raised red flags among investors, sparking worries about earnings dilution and straying from HPE’s original plan to bankroll the deal through cash reserves. Now, market participants are left pondering – what’s the prudent course of action amid this market frenzy?

The Root of Unease: Earnings Dilution and Stock Pressure

The nosedive in Hewlett Packard Enterprise’s shares is inextricably intertwined with apprehensions surrounding earnings dilution. The issuance of 27 million shares of Series C Mandatory Convertible Preferred Stock foreshadows looming dilution effects. Come September 2027, these preferred shares will morph into common shares, amplifying shareholder equity complexity.

This deviation from HPE’s cash-backed acquisition strategy cast a shadow of doubt on the firm’s financial prudence. The introduction of preferred shares means divvying out dividends to preferred shareholders, potentially strangling cash flow until these shares metamorphose into common stock.

Mandatory convertible preferred stock offerings often sound alarm bells for investors due to their dilutive impact on existing equity, spelling probable downward pressure on earnings per share (EPS) in the imminent years.

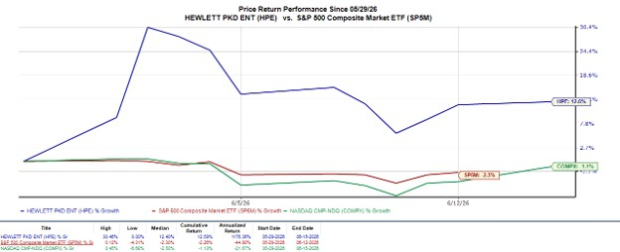

Price Perception: The Battle for Earnings

Hewlett Packard Enterprise Company price-consensus-chart | Hewlett Packard Enterprise Company Quote

Fortifying Future Growth: The Juniper Enhancement

Beneath the market tremors lies a strategic victory for Hewlett Packard Enterprise – the acquisition of Juniper Networks. This move promises vital AI-powered networking solutions, auguring well for HPE’s edge-to-cloud portfolio. The surge in hybrid cloud adoption fuels the demand for secure, high-speed networking solutions – a niche where Juniper Networks’ expertise shines, making it a coveted ally in HPE’s ecosystem.

By weaving Juniper Networks’ AI-driven automation and security tools into its GreenLake platform, HPE amplifies its capacity to deliver cloud-native, AI-infused services. With Juniper’s solid foothold in data centers and cloud service providers, HPE gains new growth horizons and cross-selling prospects.

Furthermore, this acquisition is poised to boost Hewlett Packard Enterprise’s margins, leveraging Juniper Networks’ high-margin business model. Faring well in a booming networking sector, Juniper’s expertise equips HPE to stand tall against rivals like Cisco Systems, Inc. CSCO and Arista Networks, Inc. ANET.

Cisco Systems currently dominates the enterprise networking market with a staggering market share exceeding 40%, while Arista Networks and Hewlett Packard Enterprise boast minimal market presence. With Juniper Networks now in its arsenal, HPE leaps to claim the second spot in the enterprise networking solutions landscape, just after Cisco Systems.

Predicting the Future: HPE’s Growth Trajectory

Beyond the present turmoil, Hewlett Packard Enterprise’s bright future gleams with promise. Shifting steadily from mundane hardware sales to cutting-edge cloud, AI, and data services, HPE’s metamorphosis is already yielding fruits.

The soaring adoption of HPE’s GreenLake platform, offering optimized hybrid cloud management, serves as a testament to this shift. Its recurring revenue model secures a steady cash inflow, soon reinforced by the infusion of Juniper Networks’ products.

Additionally, poised to capitalize on the snowballing demand for AI and machine learning solutions, Hewlett Packard Enterprise aligns well with the ascending trend of data-driven decision-making in the business world. The Juniper Network pact beautifully dovetails with HPE’s overarching vision of leading in the AI-fueled cloud infrastructure arena.

Final Verdict: A Hold Call for HPE Stock

As ripples from the recent stock offering reverberate, fears of earnings dilution and near-term stock fluctuation loom large. Yet, amidst the frenzy, the allure of HPE’s appealing valuation and potent long-term growth prospects shines bright. The stock’s current forward 12-month price-to-earnings and price-to-sales multiples stand at 7.87X and 0.67X, dwarfing Zacks Computer – Integrated Systems industry averages of 18.46X and 1.92X, respectively.

Embracing Juniper Networks will fortify HPE’s competitive stance in the cloud and networking arenas, laying the groundwork for future expansion. Positioned as a Zacks Rank #3 (Hold), Hewlett Packard Enterprise’s strategic moves hint at a promising growth trajectory. To explore today’s Zacks #1 Rank (Strong Buy) stocks, delve into the complete list.

Decoding the Future: Unveiling Unearthed Gems

From a swarm of stocks, 5 Zacks maestros flex their muscles, each touting a top pick destined to skyrocket +100% or more in the ensuing months. Steering through the clutter, Director of Research Sheraz Mian anoints one as the pole star of explosive potential.

Targeting the millennial and Gen Z cohorts, this company struck gold, raking in nearly $1 billion in revenue last quarter alone. Riding on a recent slump, the opportune moment beckons to hop aboard. Amidst a melange of elite selections, this beacon could outshine prior Zacks’ Stocks Set to Double like Nano-X Imaging, which catapulted +129.6% in little over 9 months.

Free: A Glimpse of Top Stock And 4 Runners Up

Catch the full article on Zacks.com by clicking here.

Cisco Systems, Inc. (CSCO) : Uncover Free Stock Analysis Report

Juniper Networks, Inc. (JNPR) : Unveil Free Stock Analysis Report

Arista Networks, Inc. (ANET) : Discover Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE) : Explore Free Stock Analysis Report

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.