As the market saturates with articles touting the virtues of long-term dividend investments, it’s essential for investors not to succumb to the pressure. While dividends have their appeal, they come with the encumbrance of double taxations for many companies, making them less attractive. However, it’s vital to note that there are numerous non-dividend paying companies with substantial growth potential. One such standout is Google (NASDAQ:GOOGL). This article delves into Google’s unrivaled prowess in software engineering, infrastructure, and assets that ensure its sustained cash flow well into the future.

Google’s Financial Performance

Amidst market volatility, Google has demonstrated unwavering financial fortitude. The company’s upcoming earnings report, due in under two weeks, is highly anticipated.

Investors are keen on continued revenue growth, especially in segments facing competition such as YouTube and Google Search. Forecasts expect a double-digit growth trend, building on the company’s previous robust performance.

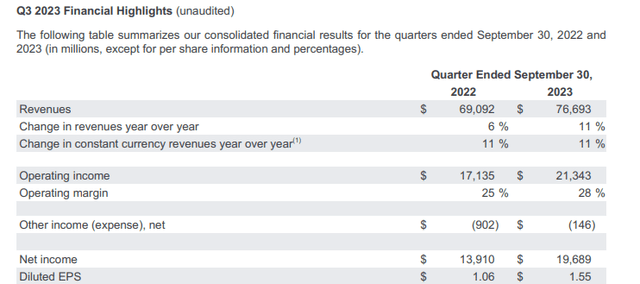

The recent quarter saw Google rake in an impressive $77 billion in revenue, marking a double-digit year-over-year uptick. This continual improvement bodes well, especially with the company’s strategic focus on cost-cutting, resulting in a substantial 28% operating income margin that amounted to $21.3 billion.

The net income surged to nearly $20 billion, a staggering 50% EPS increase from under $14 billion, illustrating the tremendous benefits derived from augmented revenue and improved margins.

Segment Performance

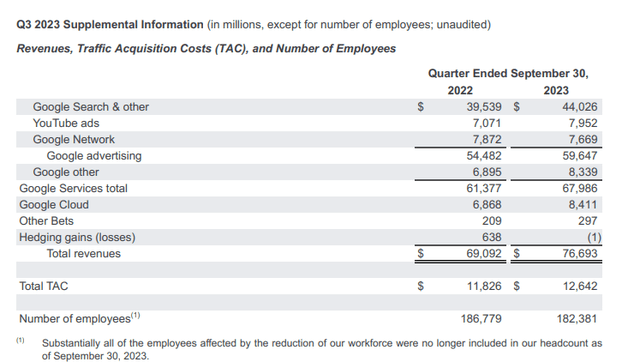

Google’s core businesses, notably Google Search and YouTube, have exhibited steadfast revenue growth, underscoring the company’s resilience in competitive landscapes. Despite a dip in Google Network revenue, the robust performance in Google Cloud has been a significant highlight, showcasing the company’s technological acumen in the cloud markets.

The “other bets” segment, although constituting a small revenue share, witnessed an impressive nearly 50% growth, contributing to overall strong revenue growth. Notably, the Traffic Acquisition Costs (TAC) remained manageable relative to revenue growth, with the company also streamlining its workforce, albeit via layoffs.

Operationally, the company embarked on an extensive balance sheet cleanup, resulting in an upswing in operating income from core services. Notably, Google Cloud transitioned from a major negative impact to a significant positive influence, while costs across the “other bets” segment also plummeted.

The strategic move of reallocating Google DeepMind + Research (Brain) to its corporate costs division, despite incurring a quarterly loss, signifies the scale of the company’s AI investment, a feat only achievable by a handful of global giants.

This substantial cleanup effort underscores the enduring robustness of Google’s business operations.

Shift in Shareholder Returns

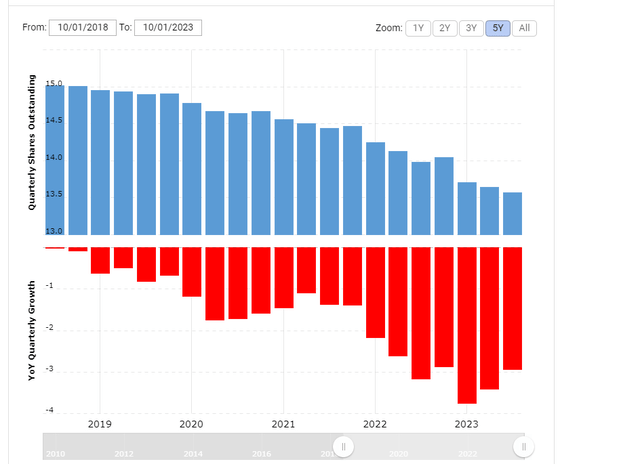

Google has redirected its focus towards enhancing shareholder returns, as evidenced by the recent announcement of $70 billion in share buybacks for 2023, carrying forward the trend from 2022.

Despite issuing shares to employees, the company has aggressively repurchased its stock, leveraging its $1.8 trillion market capitalization to repurchase nearly 4% of its outstanding shares annually.

Furthermore, with a $118 billion cash reserve earmarked for shareholder returns, Google’s renewed commitment to long-term shareholder value reflects its financial soundness. This pivot towards prioritizing shareholder returns over indiscriminate growth at any cost corroborates its stature as a compelling investment prospect.

Google’s Assets and Artificial Intelligence Dominance

Google has continually spearheaded technological innovation since its inception. The company’s DeepMind division stands undisputed as a frontrunner in artificial intelligence, with its pioneering language models representing a substantial edge, despite its challenges in commercialization compared to ChatGPT.

The Technological Goliath: Google’s Undisputed Dominance in Tech

It is a widely held belief that Google operates at the apex of the technological revolution. This view is vindicated by the internet behemoth’s unsurpassed dominance, as evidenced by the pervasive influence of its open-source projects.

- Android – Operating system for mobile devices, commanding over 70% market share globally.

- Angular – Front-end development software, powering a staggering 63% of websites.

- TensorFlow – The premier machine learning software and data training platform, capturing 37% of the market.

- Go – A programming language designed to streamline development, boasting a 7% market share.

- Kubernetes – Software for managing container deployment, with an overwhelming market share of 99%.

The ferocious competition in the technology sphere will always pose a challenge to Google. Nevertheless, as long as the company continues to harness and finance brilliant engineers, its dominance is virtually assured. Google may not always spearhead innovative concepts, but it has proven its mettle in swift adaptation, making it a formidable force in the sector.

Navigating Turbulent Waters

Despite our confidence in Google’s ability to confront the threats posed by artificial intelligence, the sheer enormity of the competition cannot be discounted. The company faces formidable adversaries, amongst the wealthiest and most influential entities globally, and their relentless pursuit remains a considerable risk.

A Worthwhile Investment

Google’s technological prowess is irrefutable. While the company’s tech assets may not portray the diversified facade often anticipated by investors, it has stealthily asserted supremacy in various technological segments. Even the specter of formidable contenders such as ChatGPT cannot diminish its core AI assets, which continue to lead the market with unmatched competitiveness.

The company’s resilience is further underscored by its robust cash flow, enabling the sustenance of substantial shareholder returns through relentless share buybacks. With the capacity to maintain an annual pace of $70 billion in share buybacks, Google’s value as an investment is unequivocal.