Dell and HPE: Navigating AI Server Demand Amid Soft PC Sales

Dell Technologies DELL and Hewlett Packard Enterprise HPE have partnerships with Nvidia NVDA to create advanced computer servers focused on artificial intelligence, drawing investor interest.

Both companies have enjoyed growth in AI servers and networking, with Dell recently posting strong Q3 results. Meanwhile, Wall Street looks ahead to Hewlett Packard’s quarterly report on Thursday, December 5.

Despite the rising demand for AI servers, traditional PC sales have faltered, leading investors to consider the timing for purchasing stock in DELL or HPE.

Insights from Dell’s Q3 Results

In Q3, Dell’s sales, driven by its Infrastructure Solutions Group (ISG), rose 10% year over year to $24.36 billion, falling slightly short of Zacks’ expected $24.56 billion. Notably, ISG segment sales reached a record $11.4 billion, growing 34% due to server and networking revenue, which surged 58% to $7.4 billion from last year.

Earnings also showed positive trends, with Q3 earnings of $2.15 per share, a 14% increase from $1.88 in the same quarter last year, surpassing expectations of $2.06. Remarkably, Dell has beaten the Zacks EPS Consensus for 11 consecutive quarters, averaging a 10.44% earnings surprise in its last four reports.

Image Source: Zacks Investment Research

Concerns About Dell’s PC Demand

With Hewlett Packard’s results on the horizon, investors should note Dell’s cautious revenue guidance. Due to weak sales in traditional PCs and heightened competition, Dell projects Q4 sales of $24-$25 billion, falling short of analyst expectations, which are at $25.27 billion representing a growth of 13%.

HPE’s Q4 Forecast

Hewlett Packard is expected to report Q4 sales growth of 12%, reaching $8.23 billion, up from $7.35 billion last year. Earnings are anticipated to increase by 6% to $0.55 per share, compared to $0.52 in the previous period.

Additionally, HPE’s server revenue surged 35% during its fiscal Q3 to $4.3 billion. Overall, Q3 sales also rose 10% year over year to $7.71 billion, exceeding estimates of $7.66 billion. HPE has consistently exceeded earnings expectations for nine successive quarters, achieving an average EPS surprise of 7.48% in its last four quarterly results.

Image Source: Zacks Investment Research

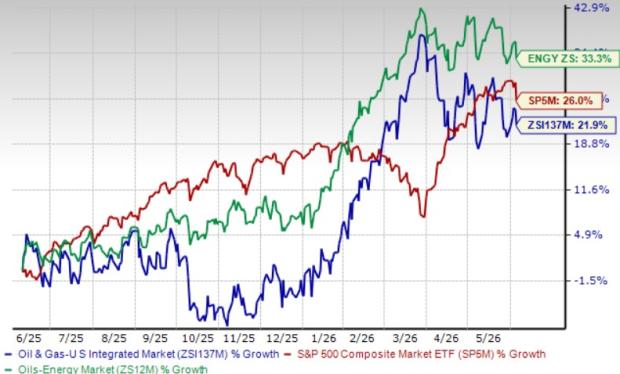

Stock Performance of DELL and HPE

This year, Dell’s stock has risen over 60%, while Hewlett Packard’s shares have gained about 25%. Both companies have outperformed broader market indices over the past three years, largely due to positive investor sentiment around their collaborations with Nvidia.

Image Source: Zacks Investment Research

With attractive valuations, DELL trades at 15.8 times forward earnings, while HPE is at 9.9 times, compared to Nvidia’s 46.2 times. Both are positioned favorably against the S&P 500’s 25.3 times forward earnings multiple and remain well below the ideal sales level of under 2 times.

Image Source: Zacks Investment Research

Conclusion

Although weakened PC demand may be a concern for Dell and Hewlett Packard, their stocks remain appealing for those wishing to invest in AI. Currently, both companies hold a Zacks Rank #3 (Hold), indicating that server growth may position them as solid investments heading into 2024 and the years ahead.

Discover Opportunities in Nuclear Energy

The demand for electricity is increasing significantly while efforts to reduce reliance on fossil fuels like oil and natural gas continue. Nuclear energy presents a viable alternative.

Recently, leaders from the US and 21 other nations pledged to triple the world’s nuclear power capacity. This ambitious initiative could lead to substantial returns for nuclear-related stocks, especially for investors who act promptly.

Our urgent report, Atomic Opportunity: Nuclear Energy’s Comeback, outlines major players and technologies involved, featuring three key stocks positioned to gain the most from this shift.

Download Atomic Opportunity: Nuclear Energy’s Comeback free today.

Dell Technologies Inc. (DELL): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Read the full article on Zacks.com.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.