Amazon and Apple Post Mixed Results Amid Market Disappointment

The markets have struggled to maintain the momentum that investors anticipated following the recent quarterly results from Amazon AMZN and Apple AAPL reported last Thursday.

While both companies met or exceeded expectations for revenue and earnings, their forecasts fell short compared to the more positive guidance provided by other major tech firms such as Meta Platforms META and Microsoft MSFT.

Amazon’s Q1 Review

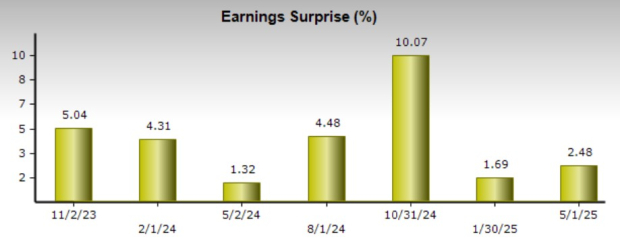

Amazon expressed its commitment to keeping prices low despite rising tariffs affecting its marketplace. In the first quarter, Amazon’s sales increased by 10% year over year, reaching $155.66 billion, surpassing forecasts of $154.56 billion. Significantly, its cloud computing arm, AWS, contributed to 19% of total Q1 sales, growing 17% year over year to $29.3 billion.

On the earnings side, the company reported an EPS of $1.59, exceeding expectations of $1.35 by 17% and showing a 40% increase from $1.13 per share a year earlier. Notably, Amazon has beaten sales expectations in three of its last four quarterly reports and has consistently surpassed earnings estimates for ten consecutive quarters.

Image Source: Zacks Investment Research

Apple’s Q2 Review

For its fiscal second quarter, Apple reported sales of $95.35 billion, a 5% increase from the previous year, exceeding estimates of $94.26 billion. The company also noted that its services segment achieved a record revenue of $26.7 billion, reflecting a 12% rise year-over-year. This growth stemmed from strong performances in Apple Music, Apple TV+, and iCloud.

Apple’s Q2 EPS of $1.65 represents an 8% increase from the prior period’s $1.53, exceeding expectations of $1.61 per share by 2%. Moreover, Apple has surpassed top and bottom-line expectations for nine consecutive quarters.

Image Source: Zacks Investment Research

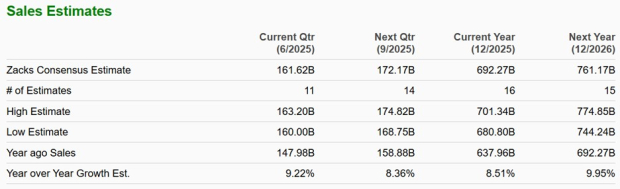

Amazon & Apple’s Guidance

Looking ahead, Amazon projects Q2 sales between $159 billion and $164 billion. The current Zacks Consensus stands at $161.62 billion, indicating a 9% growth. However, the company noted that the external environment remains challenging, with operating income guidance for Q2 between $13 billion and $17.5 billion, falling short of analysts’ expectations of $17.8 billion.

Image Source: Zacks Investment Research

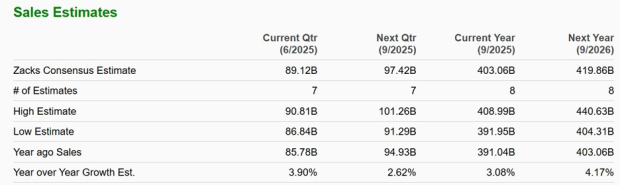

On the other hand, Apple anticipates low to mid-single-digit growth in Q3 sales, with a Zacks Consensus of $89.12 billion, translating to about 4% growth. Investor sentiment has been dampened by the expectation of $900 million in tariff-related costs at a 16% tax rate, although Apple expects its Q3 gross margins to range between 45.5% and 46.5%.

Apple projects operating expenses for Q3 between $15.3 billion and $15.4 billion. Additionally, the company plans to source 19 billion chips from various states this year, including tens of millions of advanced chips manufactured in Arizona, which should alleviate some tax-related pressures from relying heavily on international production in China, Taiwan, and India.

Image Source: Zacks Investment Research

What the Zacks Rank Suggests

Investors might be tempted to buy into the 14% drop in Amazon’s stock and a 20% decline in Apple’s year-to-date performance. However, the Zacks Rank indicates that more favorable buying opportunities could still arise. Although both companies show appealing EPS growth, forecasts for fiscal 2025 and FY2026 earnings estimates have been loosening over the past 30 days.

Currently, Amazon and Apple hold a Zacks Rank of #3 (Hold), suggesting they may present long-term value to shareholders now. That said, further declines in EPS estimates could trigger sell ratings, while significant increases could prompt buy ratings—though this may be unlikely at this time given their less-than-optimistic guidance.