BJ’s Wholesale Club Overview

While Costco Wholesale (NASDAQ: COST) continues its reign as a beloved investment choice, its smaller competitor, BJ’s Wholesale Club (NYSE: BJ), might just be the dark horse in the race for investors’ attention. Striking similarity in the perks offered to members, BJ’s Wholesale Club brings a lucrative deal to the table with a substantially lower price tag compared to its formidable counterpart.

BJ’s impressive member growth trajectory paints a promising picture. From boasting over 5 million paid memberships at its IPO in early 2018, the figure surged to beyond 7 million by the close of fiscal 2023. The company’s sturdy member retention rate of 90% illustrates its ability to hold on to its faithful patrons in a fiercely competitive market, nudging ahead of Costco that recorded a slightly higher renewal rate of 93% in its recent quarter.

The Rise of BJ’s

BJ’s strategic focus on enhancing its privately owned brands has been a key driver of member value. Back in 2017, these brands accounted for 19% of total sales, a figure that increased to almost 26% in 2023. With ambitions to push this metric to 30% in the long run, BJ’s is in for a compelling value proposition to fuel consistent high renewal rates.

Expanding its footprint steadily, BJ’s has been opening new club locations at a measured pace. With 244 club locations as of end-2023 and plans to unveil 12 more this year, BJ’s growth trajectory seems solid against the backdrop of Costco’s mammoth 900 locations, indicating ample room for continued expansion.

Investment Outlook

Generating significant profits from membership fees, BJ’s fiscal 2023 earnings showcased the allure of this revenue stream. With membership-fee revenue totaling $421 million out of a $524 million annual net income, the company’s growth lies in amplifying its member base – a path already in motion.

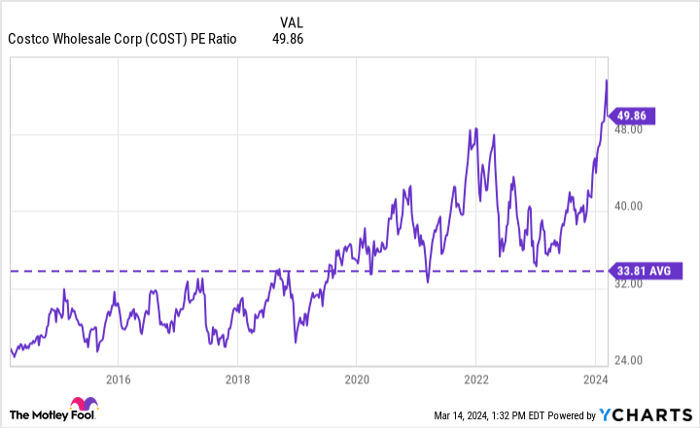

While Costco undoubtedly shines as an industry titan, BJ’s resonates as a sound investment option with a more favorable valuation. Trading at a rational price, BJ’s offers a safer stock bet compared to the premium-toting Costco. The odds of securing market-beating returns are brighter with BJ’s cheaper entry point and growing membership base.

Warren Buffett’s timeless advice of seeking a margin of safety in investments holds true here. Costco’s lofty valuation poses risks for new entrants, while BJ’s accessible price beckons those eyeing a promising yet prudent investment opportunity.

For long-term prosperity, BJ’s relentless pursuit of expanding its member base remains paramount. For investors looking beyond the numbers, BJ’s upward-trending paid memberships make it a compelling buy in the present market scenario.

Curious to invest $1,000 in BJ’s Wholesale Club?

Before diving into BJ’s Wholesale Club stock, it’s worth noting that the Motley Fool Stock Advisor team is backing other promising stocks for potential mammoth returns in the years ahead. While BJ’s isn’t on their top 10 list, exploring their picks offers a roadmap to success, outperforming the S&P 500 threefold since 2002.*

Explore the 10 recommended stocks now for your investment journey.

*Stock Advisor returns as of March 11, 2024

Jon Quast holds no position in any of the mentioned stocks, and The Motley Fool divulges involvement with and endorsement of Costco Wholesale, following a strict disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.