The Resilient Rise of Iron Mountain Incorporated

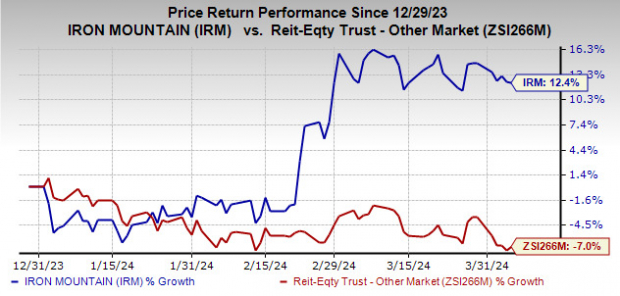

Iron Mountain Incorporated (IRM) has seen a remarkable 12.4% surge in its stock year to date, a stark contrast to the industry’s 7% decline. This Boston-based real estate investment trust (REIT) has continued to thrive due to its dependable core storage and records management operations, positioning itself as a steadfast player in a volatile market. The company’s strategic acquisitions and robust expansion into the data center business have undoubtedly played a significant role in this success.

Financial Growth and Performance

February 2024 saw the company exceed expectations as it reported fourth-quarter 2023 adjusted funds from operations (AFFO) per share of $1.11, soaring past the Zacks Consensus Estimate of $1.05. This 8.8% year-over-year increase underscores Iron Mountain’s solid performance across various segments, including storage, services, and data centers. The company’s projected 2024 AFFO per share of $4.39-$4.51 aligns closely with the Zacks Consensus Estimate of $4.42, reflecting a confident outlook.

Image Source: Zacks Investment Research

Let’s delve deeper into the factors fueling the growth in Iron Mountain’s stock price.

Iron Mountain’s steady revenue streams stem predominantly from fixed periodic storage rental fees, offering consistency and reliability in an uncertain market. The company’s organic storage rental revenues surged by 10% year over year in Q4 2023, driven by strong pricing, volume trends, and data center expansions.

With over 225,000 clients spanning various industries and regions, Iron Mountain boasts a diverse revenue base, with no single customer contributing more than 1% of revenues in 2023. This diversification fortifies the company’s financial standing and mitigates risks associated with dependency on a few key clients.

In the fourth quarter of 2023, IRM achieved an impressive 92.9% retention rate in its records management business, coupled with robust customer retention in the global data center segment. Such performance indicators signal a positive trajectory for the company’s cash flows in the upcoming quarter, with storage rental revenues expected to grow by 11.3% in 2024.

Iron Mountain has strategically expanded into fast-growing areas, notably the data center segment, bolstering its performance and market presence. The company’s data center revenue jumped by 23.4% in Q4, outperforming projections by leasing 124 megawatts of data center capacity in 2023, a testament to its successful growth initiatives.

Financial Stability and Future Prospects

The company’s robust balance sheet and financial flexibility have empowered Iron Mountain to seize long-term growth opportunities effectively. With a total liquidity of $2.8 billion as of December 31, 2023, and manageable debt maturities extending to 2027, Iron Mountain stands on solid financial ground. Its prudent leverage management, evident from a net total lease-adjusted leverage of 5.1X in 2023, positions the company favorably amidst market fluctuations.

Iron Mountain’s anticipated cash flow growth of 4.46%, compared to the industry’s projected -5.32%, underscores its financial strength and operational efficiency. The company’s substantial return on equity and prudent dividend policy further enhance shareholder value, with its recent 5.1% dividend hike showcasing commitment to sustainable growth and investor confidence.

Given its healthy financial footing, projected AFFO growth, and industry-leading dividend payouts, Iron Mountain’s latest dividend increase is poised to deliver long-term value and stability to investors, a testament to the company’s enduring performance.

Exploring Diversified Investment Opportunities

For investors seeking diversified options in the REIT sector, other top-ranked stocks like Host Hotels & Resorts (HST) and Gladstone Commercial (GOOD) offer compelling prospects. Both companies currently hold a Zacks Rank #1, with positive forecasts for revenue and growth.

The Zacks Consensus Estimate for HST’s 2024 FFO per share has seen a 2.6% uptick in the past month, while GOOD’s current-year FFO per share estimate has surged by 5.3% over the last two months, reflecting strong momentum and investor confidence in the broader real estate market.

As we navigate the intricacies of REIT investing, remember that earnings presented in this context refer to funds from operations (FFO), a pivotal metric in assessing the performance and viability of REIT investments.

Follow Zacks Investment Research for timely updates on market trends and stock recommendations to guide your investment decisions effectively. Discover hidden gems and potential winners before they make it to the mainstream, providing you with a unique edge in the dynamic world of finance.

Stay informed, stay ahead with Zacks Research. Explore your options and uncover the next big opportunities in the market – seize your chance to shine today!

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.