Iron Mountain Set to Announce Q3 Earnings: Analysts Predict Positive Growth

Iron Mountain Incorporated (IRM), based in Boston, Massachusetts, is a prominent player in storage and information management services. With a focus on secure data storage, records management, and information destruction, the company boasts a market cap of $36.9 billion. Investors are eagerly awaiting the release of its Q3 earnings, which is scheduled for Wednesday, Nov. 6, before the market opens.

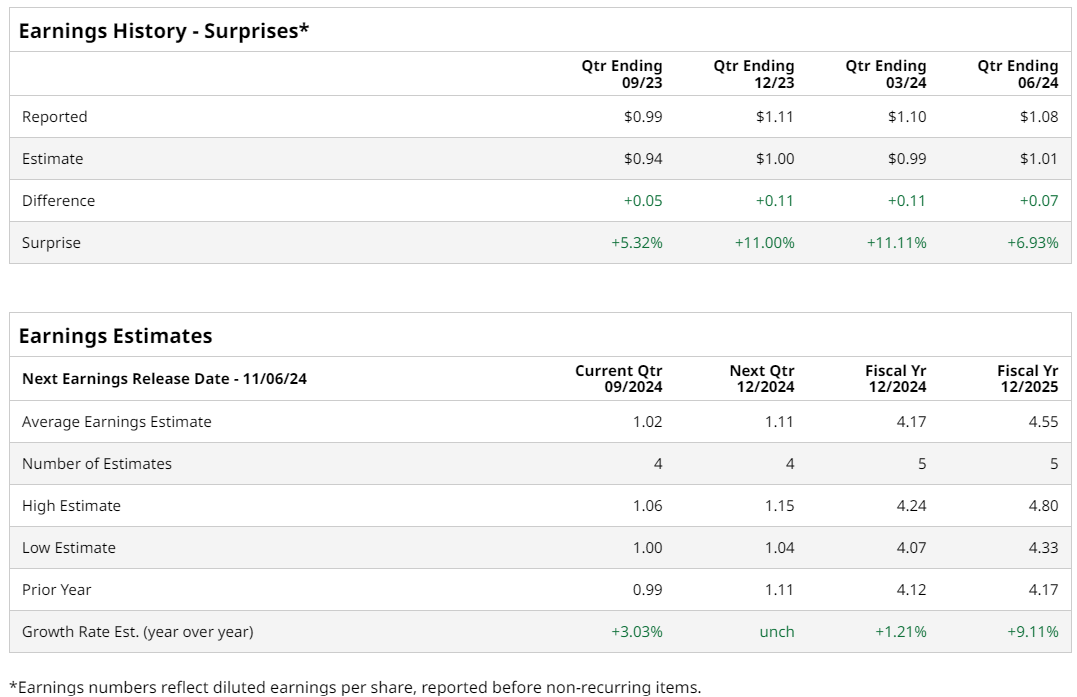

Analysts Forecast Solid Earnings Increase

Analysts project that IRM will report funds from operations of $1.02 per share, marking a 3% increase from $0.99 per share during the same quarter last year. Remarkably, Iron Mountain has consistently outperformed Wall Street’s earnings expectations over the past four quarters.

Impressive Last Quarter Performance

In the previous quarter, the company achieved an adjusted FFO of $1.08 per share, which exceeded the consensus estimate by 6.9%. This impressive performance was driven by the successful implementation of its Project Matterhorn strategy, leading to record Q2 revenue and EBITDA.

Future Outlook for 2024

Looking ahead to fiscal 2024, analysts anticipate that IRM will report an FFO of $4.17, reflecting a 1.2% increase from $4.12 in fiscal 2023. Investors will be keen to see if the company can maintain this upward trajectory.

IRM Stock Performance and Analyst Ratings

Year-to-date, IRM stock has increased by 79.7%, significantly outperforming the broader S&P 500 Index, which has gained 23%, and the iShares Cohen & Steers REIT ETF’s 12.3% gain.

Recent news also highlights positive developments for IRM. On September 23, the stock rose by over 2% after Stifel increased its price target from $117 to $140. Additionally, on August 1, shares jumped more than 6% following the announcement of Q2 revenue of $1.53 billion, which exceeded expectations.

Analyst Consensus and Future Recommendations

The general sentiment on IRM stock is moderately bullish, reflected in an overall “Moderate Buy” rating. Out of seven analysts covering the stock, five recommend a “Strong Buy,” one suggests a “Moderate Buy,” and one advises a “Strong Sell.”

Currently, the average analyst price target stands at $111.50, indicating that the stock trades at a premium relative to this outlook.

On the date of publication, Rashmi Kumari did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.