Adobe Expands AI Capabilities Amid Competitive Landscape

Adobe (ADBE) introduced its Firefly Video Model-powered Generative Extend in Premiere Pro on Tuesday. This innovative feature uses AI to generate and lengthen video and audio clips in real-time. With AI-powered Media Intelligence, users can swiftly locate specific clips within vast terabytes of footage. Both Adobe Generative Extend and Media Intelligence are now generally available, complemented by upgrades like AI-powered Caption Translation in Premiere Pro.

Additionally, Adobe has released a new version of After Effects, which includes a high-performance preview playback engine, robust 3D motion design tools, and HDR monitoring. The latest Frame.io V4 upgrades feature expanded storage that scales with team needs, eliminating workflow disruptions and enabling seamless sharing, management, and organization of work-in-progress and finished assets.

Adobe Enhances AI Portfolio to Strengthen Market Position

Adobe continues to broaden its AI portfolio with Adobe GenStudio and Firefly Services, aimed at facilitating collaboration between brands and their agency partners on marketing campaigns. The company plans to launch a comprehensive suite of web, mobile, and desktop applications through various subscription tiers designed for creative professionals.

With intentions to monetize standalone subscriptions for Firefly, Adobe will introduce multiple Creative Cloud offerings that incorporate Firefly tiering. Furthermore, the integration of AI Assistant into Acrobat, Reader, and Express supports Adobe’s strategic growth direction.

ADBE is embedding Generative AI innovations throughout its portfolio, with various AI-first standalone and add-on products such as Acrobat AI Assistant, Firefly App, and GenStudio for Performance Marketing. These developments may drive significant top-line growth.

Fiscal Year 2025 Guidance Shows Growth Potential

For fiscal 2025, Adobe anticipates Digital Media Annual Recurring Revenue growth of approximately 11%. Estimated revenues for the Digital Media segment are expected to fall between $17.25 billion and $17.40 billion. Meanwhile, the Digital Experience segment revenues are forecasted to be between $5.8 billion and $5.9 billion, with Digital Experience subscription segment revenues projected between $5.375 billion and $5.425 billion.

Adobe reaffirmed its total revenue guidance for fiscal 2025, expected to be between $23.30 billion and $23.55 billion, compared to $21.51 billion in fiscal 2024. Non-GAAP earnings are forecasted to fall between $20.20 and $20.50, up from $18.42 per share in the previous fiscal year.

Revisions in Estimates Signal Positive Momentum

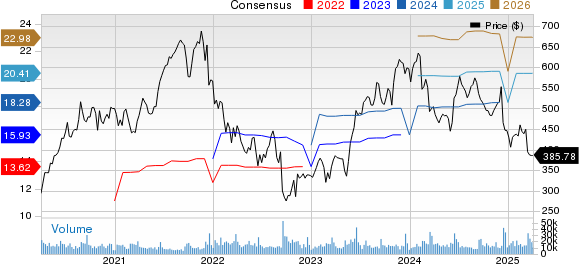

The Zacks Consensus Estimate for Adobe’s earnings in fiscal 2025 is currently $20.41 per share, reflecting a modest increase over the past month. This estimate suggests a growth rate of 10.8% compared to fiscal 2024.

For the second quarter of fiscal 2025, the earnings estimate remains steady at $4.97 per share, which indicates a projected growth of 10.94% from the same quarter last year.

Analyzing Adobe’s Pricing and Consensus Performance

Adobe Inc. price-consensus-chart | Adobe Inc. Quote

ADBE has consistently exceeded the Zacks Consensus Estimate in all four previous quarters, achieving an average surprise of 2.53%.

Find the latest EPS estimates and surprises on Zacks earnings Calendar.

ADBE Stock: An Investment Assessment

Adobe’s growing focus on Generative AI presents a significant catalyst for growth. However, shares have seen a decline of 11% year-to-date (YTD), largely influenced by intense competition from firms like Microsoft (MSFT)-backed OpenAI, along with challenges in monetizing its AI solutions.

In comparison to its peers, Adobe’s AI business remains relatively small. Microsoft is reaping benefits from its Intelligent Cloud revenues driven by Azure AI services and its AI Copilot business. Alphabet’s Google Cloud continues to experience growth in AI infrastructure and enterprise AI platform Vertex while Synopsys (SNPS) effectively penetrates the expanding AI chip market.

Looking at share price performance, Microsoft and Synopsys have outperformed Adobe, yet Alphabet has lagged behind this year. Microsoft and Synopsys shares have declined by 9.4% and 8%, respectively, while Alphabet’s shares have dropped by 17.1%.

Currently, ADBE holds a Zacks Rank #3 (Hold), indicating that investors may want to wait for a more opportune time to accumulate shares of the company.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks’ Research Chief Identifies High-Potential Stock

Our expert team has highlighted five stocks with a high likelihood of gaining 100% or more in the coming months. Among them, Director of Research Sheraz Mian has pointed out a standout stock that is expected to show significant growth.

This leading pick belongs to an innovative financial firm with over 50 million customers and a range of cutting-edge solutions, positioning it for substantial upward movement. While not every elite pick has succeeded, this stock could outperform previous Zacks Stocks that saw significant gains, such as Nano-X Imaging, which increased by 129.6% in just over nine months.

Free: See our Top Stock and four runners-up.

Stay informed with Zacks Investment Research’s latest recommendations. Download your free copy of the report featuring the 7 Best Stocks for the Next 30 Days. Click here.

Microsoft Corporation (MSFT): Free stock analysis report.

Adobe Inc. (ADBE): Free stock analysis report.

Synopsys, Inc. (SNPS): Free stock analysis report.

Alphabet Inc. (GOOGL): Free stock analysis report.

This article was originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.