CrowdStrike (NASDAQ: CRWD) CEO George Kurtz’s bold stance during the recent quarterly conference call has sparked enthusiasm among investors, propelling the market’s positive response. As a result, the shares of the top endpoint-cybersecurity software provider have managed to maintain a significant portion of their over 200% surge since the beginning of 2023.

Kurtz took a subtle jab at several cybersecurity rivals in the latest earnings update, with references to Palo Alto Networks (NASDAQ: PANW), as CrowdStrike’s integrated platform endeavors to carve out its share of a fiercely competitive security-software domain. (It’s worth noting that Palo Alto’s CEO, along with the co-founders and CEOs of Zscaler (NASDAQ: ZS) and Cloudflare, also tend to critique their peers during quarterly investor calls.)

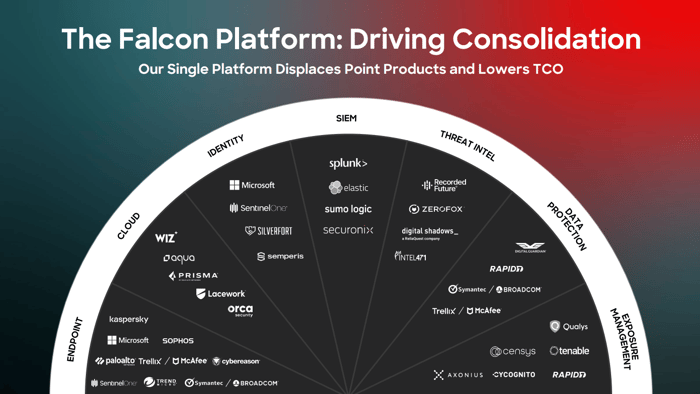

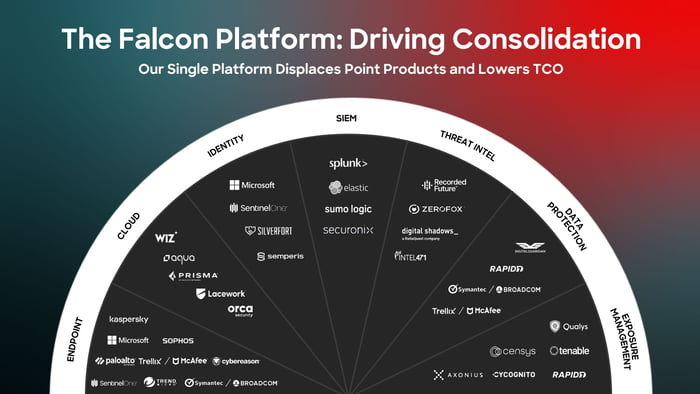

An Industry Primed for Consolidation

The cybersecurity market leaders are championing the concept of “platforming” in the sector, aiming to streamline the array of cybersecurity vendors available to organizations. CrowdStrike, specializing in endpoint security, alongside Palo Alto Networks, Fortinet (NASDAQ: FTNT) in legacy network security, and Zscaler in cloud-based network security, are expanding their offerings to provide clients with comprehensive security solutions. Consolidation not only simplifies security management but also enhances overall outcomes for organizations.

CrowdStrike stands out in this realm due to its single platform approach that caters to various software security needs, ensuring ease of security monitoring in contrast to managing multiple modules and disparate data dashboards.

Chart source: CrowdStrike.

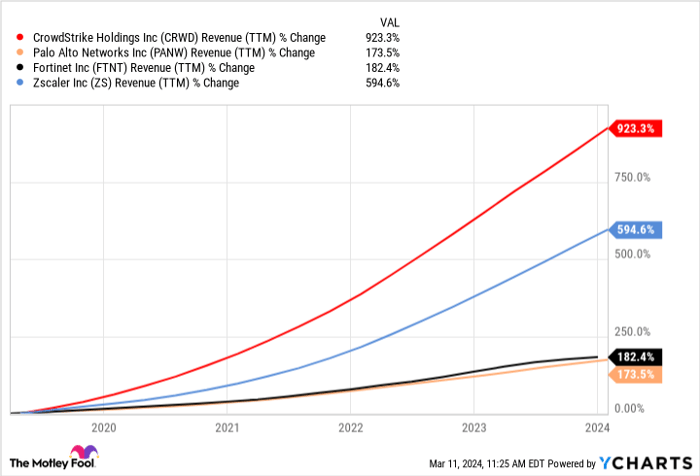

It’s evident that the major players in the cybersecurity domain have been outpacing the industry’s growth rate consistently, with CrowdStrike boasting stellar sales growth figures, recently crossing the $3 billion sales threshold for the first time in five years.

Data by YCharts.

CrowdStrike’s Enduring Advantage in the Security Software Arena

Despite its remarkable growth trajectory, CrowdStrike faced skepticism from a broad investor base post its IPO in 2019, primarily due to sustained losses under generally accepted accounting principles (GAAP) until the second half of fiscal 2024.

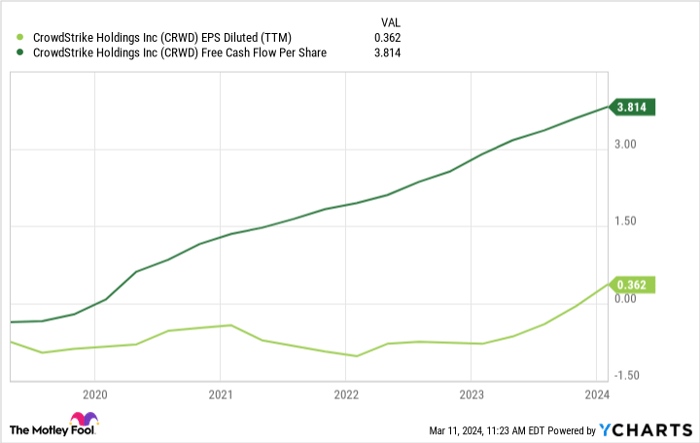

However, with positive and rising free cash flow (FCF) and attaining profitability across key metrics, including addressing concerns over high employee stock-based compensation, CrowdStrike has positioned itself favorably to win over a new cohort of investors. The argument that stock-based compensation dilutes shareholder value has subsided considerably on a per-share basis, factoring in the growing share count.

Data by YCharts.

Looking beyond CrowdStrike’s technological prowess, metrics signaling profitability validate the company’s sustainable business model. Though the stock may not be considered cheap, trading at over 80 times this year’s anticipated GAAP earnings per share and over 60 times next year’s early earning projections, its expected revenue growth of 30% in calendar year 2024 presents an attractive proposition for long-term investors. Personally, I’ve added to my holdings and will keep a close eye on this stock.

Is investing $1,000 in CrowdStrike a wise choice right now?

Prior to investing in CrowdStrike, it’s prudent to consider the insights of the Motley Fool Stock Advisor analyst team, who have identified what they deem the top 10 stocks for investors currently. While CrowdStrike didn’t make the cut, the selected 10 stocks are expected to yield substantial returns in the foreseeable future.

Stock Advisor equips investors with a straightforward roadmap to success, providing portfolio building advice, analyst updates, and two new stock suggestions monthly. Since 2002, the Stock Advisor service has outperformed the S&P 500 returns threefold.

Explore the 10 recommended stocks

*Stock Advisor returns as of March 11, 2024

Nicholas Rossolillo and his clients hold positions in CrowdStrike, Fortinet, and Palo Alto Networks. The Motley Fool holds positions in and recommends CrowdStrike, Fortinet, Palo Alto Networks, and Zscaler. The Motley Fool maintains a disclosure policy.

The views and opinions expressed herein are the author’s own and do not necessarily reflect those of Nasdaq, Inc.