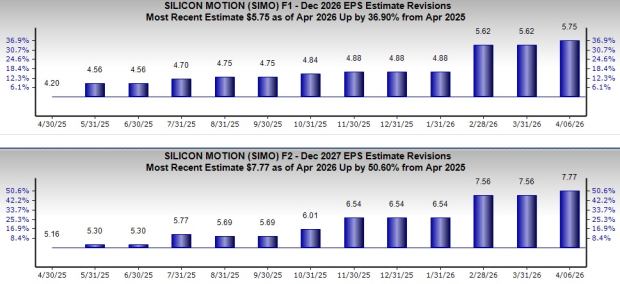

Silicon Motion Technology Corporation (SIMO) has experienced a significant uptick in earnings estimates, with projections for 2026 rising by 36.9% to $5.75, and for 2027 increasing by 50.6% to $7.77. This surge in estimates reflects a bullish sentiment towards the company’s growth potential.

Operating based on a fabless business model, Silicon Motion specializes in designing SSD controllers and has recently initiated mass production of the world’s first PCIe Gen5 client SSD controller, the SM2508, which boasts 50% lower power consumption than its 12nm counterparts. The company has shipped over 5 billion controllers in the last decade, averaging over 750 million NAND controllers annually.

Despite achieving a remarkable 199.1% stock increase over the past year compared to the industry’s 145.5%, challenges persist including fierce competition, high R&D costs, and geopolitical tensions affecting market stability. These factors may hinder long-term profitability, prompting caution among investors.