Universal Health Services, Inc. (UHS): A Closer Look at Stock Valuation and Growth Potential

Valuation Snapshot of UHS

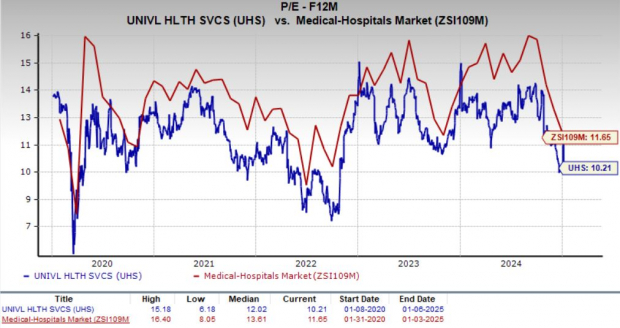

Based in King of Prussia, PA, Universal Health Services, Inc. (UHS) is currently exhibiting a compelling valuation offer. The stock’s forward earnings multiple of 10.21X significantly falls below its five-year median of 12.02X and the medical hospital industry average of 11.65X. Comparatively, peers like Tenet Healthcare Corporation (THC) and HCA Healthcare, Inc. (HCA), which have forward 12-month P/E ratios of 11.06X and 11.96X, respectively, make UHS appear more budget-friendly. The company also holds a Value Score of A, making it a prime candidate for value-seeking investors.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Performance Review

In the past year, shares of Universal Health have increased by 17.2%, which outpaces the industry average gain of 4.5%. However, it has not kept pace with the broader S&P 500 Index.

Stock Price Performance – UHS, THC, HCA, Industry & S&P 500

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Given the stock’s current discount, it’s essential to explore UHS’s growth drivers and potential hurdles to assess if it is an attractive investment opportunity for cautious investors.

Growth Factors for Universal Health Services

Universal Health continues to experience revenue growth, particularly in its Acute Care Hospital Services and Behavioral Health Care Services divisions. This growth is supported by rising adjusted admissions and patient days. Specifically, adjusted admissions in the Acute Care segment increased 8.8% year over year in 2021, 5.7% in 2022, 6.5% in 2023, and 4% in the first three quarters of 2024. In the Behavioral Health Care service, adjusted patient days saw yearly increases of 0.6% in 2021, 1.1% in 2022, 1.7% in 2023, and 1.8% in the first nine months of 2024.

These statistics highlight the growing demand for UHS’s services. To manage this increased demand, UHS is actively pursuing strategic acquisitions, which play a significant role in its growth strategy. Additionally, the company’s sound financial footing bolsters these expansion efforts.

In 2023, UHS generated $1.3 billion in operating cash flow, marking a 27.3% year-over-year rise. In the first nine months of 2024, operating cash flow surged by an impressive 72.8% year over year. UHS also maintains a long-term debt-to-capital ratio of 40.9%, significantly lower than the industry average of 85.3%, showcasing its effective financial management.

The strong cash generation further enables UHS to enhance shareholder value, as evidenced by share repurchases totaling about $349 million in the first nine months of 2024. By September 30, 2024, the company had approximately $1.1 billion remaining in its share repurchase capacity, demonstrating its commitment to returning value to shareholders.

Earnings Estimates and Performance History

Currently, the Zacks Consensus Estimate projects that UHS’s adjusted earnings for 2024 will reach $15.88 per share, reflecting a 50.7% year-over-year increase. The estimate for 2025 suggests an additional growth of 11.4%. These earnings estimates have remained stable over the past month. Revenue estimates for 2024 and 2025 indicate year-over-year growth of 9.9% and 6.1%, respectively.

UHS has outperformed earnings estimates in three of the last four quarters, registering an average surprise of 12.1%.

Universal Health Services Stock Price and EPS Surprise

Universal Health Services, Inc. price-eps-surprise | Universal Health Services, Inc. Quote

Investment Outlook for UHS Stock

Despite its discounted trading position, UHS stock may not be the best fit for new investors at this moment. Current shareholders could benefit from its lower valuation, growing revenues, and solid financial performance; however, prospective buyers might want to hold off for now.

The broader hospital industry faces several obstacles, including the government’s push to reduce spending and potential policy changes that threaten hospital profitability in the short term. Additionally, uncertainties regarding decreased hospital funding and the end of insurance subsidies amplify concerns within the sector.

A notable surge in operating expenses also represents a significant challenge for UHS. Over the years 2021 through the first three quarters of 2024, operating expenses rose 10.6%, 9.9%, 5.7%, and 7.9% year over year, respectively. With ongoing increases in resource utilization, salaries, supply costs, and others, operating expenses are expected to escalate further.

Furthermore, UHS enjoys a Return on Invested Capital of 9.54%, which is beneath the industry average of 12.89%. This indicates UHS is lagging in generating competitive returns on its invested capital in comparison to its rivals.

In conclusion, while UHS displays robust financial health and growth potential, investors should be wary of the outlined challenges. Presently rated with a Zacks Rank #3 (Hold), it might be prudent for new investors to stay on the sidelines until a more favorable entry point emerges. You can view today’s complete list of Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, past recommendations have seen increases of +143.0%, +175.9%, +498.3%, and +673.0%.

Most of the stocks in this report are not widely followed, presenting a great opportunity for early investment.

Discover These 5 Potential Home Runs >>

Universal Health Services, Inc. (UHS): Free Stock Analysis Report

Tenet Healthcare Corporation (THC): Free Stock Analysis Report

HCA Healthcare, Inc. (HCA): Free Stock Analysis Report

For the complete article on Zacks.com, click here.

The views and opinions expressed herein are those of the author alone and do not necessarily reflect the views of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.