Pinterest Reports 12.5% Decline Amidst Competitive Pressure

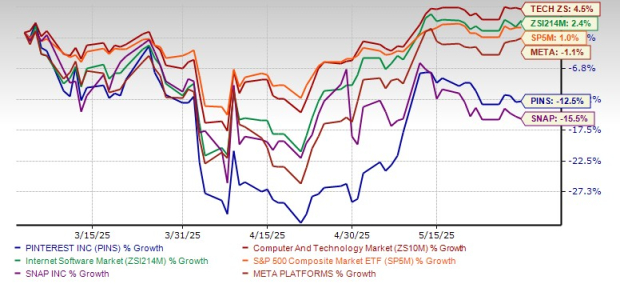

Pinterest, Inc. (PINS) has experienced a 12.5% drop in share price over the past three months, contrasting with the Internet – Software sector’s modest growth of 2.4%. Additionally, PINS has underperformed compared to the Zacks Computer & Technology sector and the S&P 500, which saw increases of 4.5% and 1%, respectively.

Image Source: Zacks Investment Research

In comparison to its peers, Pinterest fared better than Snap Inc. (SNAP), which saw a decline of 15.5%, but lagged behind Meta Platforms, Inc. (META), which fell by 1.1% in the same timeframe.

Key Growth Catalysts for PINS

Pinterest aims to enhance user engagement by targeting multiple sectors, such as retail, consumer goods, travel, finance, and automotive. The company recently partnered with the New York Liberty, a WNBA champion team, to offer exclusive content and experiences on its platform, catering to the growing interest in women’s basketball. This initiative is expected to create new monetization opportunities within sports marketing.

The implementation of advanced AI models is positioned to bolster relevance and personalization on the platform, contributing to long-term growth. Pinterest is also developing new advertising tools and formats designed to enhance monetization capabilities, allowing advertisers to better gauge campaign effectiveness.

Its innovative visual search feature allows users to begin searches with images rather than keywords. Users can filter searches by color, style, and fabric, utilizing cutting-edge AI to improve discovery. This integration is likely to enhance user engagement significantly.

Strong revenue growth is linked to Pinterest’s focus on monetization. In Q1 2025, international Shopping ad revenues surged three times faster than overall revenue growth. The AI-enabled Performance+ suite is boosting ad efficiency for advertisers and retailers as Pinterest integrates AI into its operations.

Image Source: Zacks Investment Research

Major Challenges for PINS

Pinterest primarily relies on advertising revenue, making it susceptible to shifts in the advertising landscape, changing advertiser preferences, and economic downturns. While ad impressions grew by 49% in Q1, ad pricing decreased by 22% year-over-year, mainly due to lower rates in new international markets.

Intense competition from firms such as Meta, Google, and TikTok poses significant challenges. Competing entities often possess greater financial resources. To counter this, Pinterest must invest increasingly in new tools, which pressures profit margins. Total costs surged to $890.5 million in Q1 from $794.4 million a year earlier, with R&D expenses climbing to $331.7 million from $280.3 million.

Macroeconomic volatility is affecting certain sectors, particularly consumer-packaged goods. Additionally, some Asia-based e-commerce retailers are reducing U.S. ad spending due to tariff changes, raising more concerns for Pinterest.

Image Source: Zacks Investment Research

Estimate Revision Trend of PINS

Pinterest is experiencing a decline in earnings estimates. Projections for 2025 have decreased by 1.62% to $1.82, and 2026 estimates dropped by 2.3% to $2.12. This negative revision trend suggests bearish sentiment regarding the stock’s growth prospects.

Image Source: Zacks Investment Research

Key Valuation Metric of PINS

From a valuation perspective, Pinterest shares appear relatively inexpensive compared to industry peers. Currently, the price/sales ratio is 4.8 forward sales, lower than the industry average of 5.44 and the stock’s mean of 5.21.

Image Source: Zacks Investment Research

End Note

Pinterest continues to grow its monthly active users across various regions. The company’s strong focus on enhancing shoppability and monetization, alongside the adoption of advanced AI tools, serves as potential growth drivers. However, macroeconomic issues, geopolitical instability, and tariff shifts are hindering ad spending in certain areas. Increased operational costs due to expansion efforts are impacting profit margins as well. Given the stiff competition from other consumer internet firms, Pinterest holds a Zacks Rank of #3 (Hold), suggesting cautious trading for new investors.

Zacks Names #1 Semiconductor Stock

For further insights, explore the market potential of a leading semiconductor stock positioned to benefit from growing demand in AI, machine learning, and IoT sectors.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.