Snowflake’s Growth Outpaces Technology Sector Amid Strong Q1 Projections

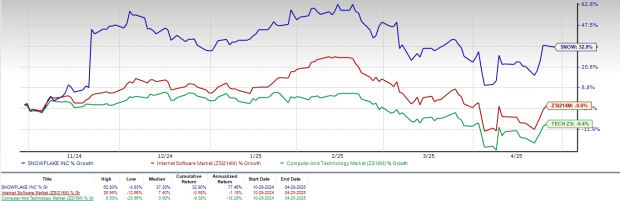

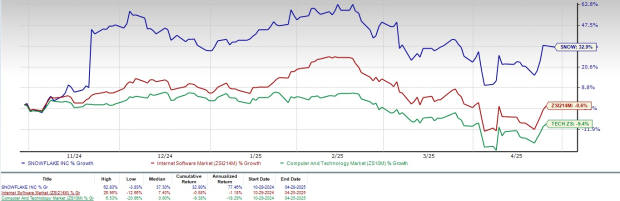

Snowflake (SNOW) shares increased by 32.9% over the past six months, significantly outperforming both the Zacks Computer and Technology sector, which fell by 9.4%, and the Zacks Internet Software industry, which saw a slight decline of 0.6%.

This remarkable performance is tied to Snowflake’s solid product offerings and its growing customer base. As of January 31, 2025, the company had 11,159 customers, a rise from 9,384 one year earlier. Among these clients, 745 are from the Forbes Global 2000 and contributed 45% of Snowflake’s projected fiscal 2025 revenues of $3.6 billion, representing a 29% year-over-year increase.

The strong adoption and usage of Snowflake’s platform is reflected in a net revenue retention rate of 126% as of January 31, 2025. Additionally, the number of customers generating over $1 million in trailing 12-month product revenue increased from 455 in 2024 to 580 in 2025.

Recent Stock Performance of SNOW

Image Source: Zacks Investment Research

Expanding Portfolio Drives Growth

Snowflake’s diverse portfolio has been instrumental in its progress. Products such as Apache Iceberg, Hybrid tables, Polaris, and Cortex Large Language Model have attracted new customers.

In April 2025, Snowflake enhanced its AI Data Cloud by integrating its core functionalities with Apache Iceberg tables. This development allows for more seamless open lakehouse strategies, improved query performance, and better security and data sharing, alongside advancements in open-source contributions.

Investments in artificial intelligence (AI) and machine learning, particularly through the introduction of Cortex AI and its integration with models from OpenAI and Anthropic, have boosted customer engagement. Weekly, over 4,000 clients are utilizing these AI and ML technologies.

Strategic Partnerships Fuel SNOW’s Growth

Snowflake’s robust partnerships with industry giants like Microsoft (MSFT), Amazon (AMZN), and NVIDIA (NVDA) are a significant factor in its success. These collaborations drive customer innovations and broaden industry-specific solutions.

In April 2025, Snowflake announced an extended partnership with Microsoft, integrating OpenAI’s models into Snowflake Cortex AI via Azure OpenAI Service. This integration empowers enterprises to create AI-driven applications.

Meanwhile, the partnership with NVIDIA allows businesses to create tailored AI data applications using both Snowflake Cortex AI and NVIDIA AI Enterprise software, enhancing overall AI performance.

Additionally, Snowflake’s collaboration with Amazon Web Services (AWS) has expanded, focusing on customer-centric innovations and increased collaborative efforts to support more than 6,000 joint customers, many of whom are Fortune 500 companies.

In a noteworthy achievement, Snowflake secured Department of Defense (DoD) Impact Level 5 Provisional Authorization on AWS GovCloud US-West in April 2025. This authorization supports secure solutions for handling Controlled Unclassified Information across DoD entities.

Positive Financial Guidance for Q1 and FY26

Looking ahead, for the first quarter of fiscal 2026, Snowflake predicts product revenues will range between $955 million and $960 million, representing a year-over-year growth of 21% to 22%.

For the full fiscal year 2026, Snowflake anticipates a 30% increase in product revenues from fiscal 2025, totaling $3.46 billion.

The Zacks Consensus Estimate for Q1 fiscal 2026 revenues stands at $1 billion, indicating a projected 21.13% year-over-year growth. The consensus estimate for earnings is 22 cents per share, showing a 57.14% increase over the past year.

Snowflake Inc. Stock Price and Consensus Estimates

Snowflake Inc. price-consensus-chart | Snowflake Inc. Quote

The Zacks Consensus Estimate for SNOW’s fiscal 2026 revenues is set at $4.44 billion, reflecting a year-over-year growth of 22.47%. The earnings consensus is pegged at $1.15 per share, unchanged in the past 30 days, indicating a 38.55% increase year-over-year.

Valuation of SNOW Stock

Currently, Snowflake shares appear overvalued, which is evident from its Value Score of F.

The SNOW stock carries a forward 12-month Price/Sales ratio of 11.2X, compared to the industry average of 4.86X.

Price/Sales Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Investment Considerations for Snowflake Stock

Snowflake’s solid product offerings and its growing partner network support its impressive growth potential. These attributes contribute to the company’s premium valuation.

SNOW currently holds a Zacks Rank #2 (Buy) and a Growth Score of B, suggesting a favorable investment opportunity based on proprietary metrics.