I’m quite sure you can’t recall the exact activities you were engaged in on December 6, 2017.

However, it is interesting to note that according to historical records, on that day “Rockstar” by Post Malone was dominating the U.S music charts and “Havana” by Camila Cabello was making waves in the U.K.

While these musical interludes were happening, other significant events were in motion, including the swearing in of Andrej Babiš as the Czech Republic’s prime minister and President Donald Trump’s announcement regarding Jerusalem’s status.

Amidst all this, a piece of financial insight was published – “A Textbook Catalyst That Should Move This REIT’s Multiple” – highlighting the potential impact of catalysts on stock values.

The concept of catalysts is crucial in the stock market; however, I always advocate for investments that can thrive independently, regardless of external forces.

The Role of Catalysts

Ignoring the potential of a catalyst is akin to turning a blind eye to an opportunity ripe for the taking. While every catalyst may not be suitable for every investor, it’s essential to be aware of what’s in play.

“A catalyst refers to an event that has occurred in a company… that would significantly increase its valuation.

“The value of a company is based on its future ability to generate free cash flow. Therefore, a catalyst usually improves free cash flow, resulting in a higher implied valuation both because of the better future performance and because of a better implied multiple.”

A catalyst propels a business forward in terms of its marketing, capability, and income generation, leading to increased valuation.

However, there’s a crucial distinction between actual catalysts and potential catalysts, as the latter may not materialize and can lead to financial losses. The discernment of a true catalyst is critical, as it hinges on substantive justification, not mere speculation.

Identifying Potential Profit Catalysts

Catalysts were a focal point of discussion when I was interviewed by Seeking Alpha in late October 2023. The profound impact of artificial intelligence on data center REITs was highlighted. While this trend continues to hold potential, much of its influence has already been factored into stock prices.

To truly capitalize on a catalyst, one must enter the market before it materializes. This often involves recognizing subtle indicators, such as merger possibilities or managerial shifts.

For instance, I predicted in late August a potential acquisition of Spirit Realty (SRC) by Realty Income (O), which was subsequently announced close to two months later. This demonstrates the value of interpreting subtle signs of change in the market.

Changes in management, new contracts, global expansions, or external economic factors are also capable of propelling stock prices into greater profitability.

Amidst this landscape, VICI Properties (VICI) emerges as a compelling prospect. The gaming REIT went public in 2018 and within just a few years, had achieved an investment-grade credit rating and inclusion into the S&P 500 – a feat possibly unmatched by any other REIT in such a short time frame.

VICI’s portfolio boasts top gaming, hospitality, and entertainment destinations, including iconic properties such as Caesars Palace, The Mirage, MGM Grand, and The Venetian Resort, all situated on the illustrious Las Vegas Strip.

VICI Properties and Safehold: A Closer Look at Two Unique REITs

VICI Properties: Expanding Horizons and Diversifying Portfolios

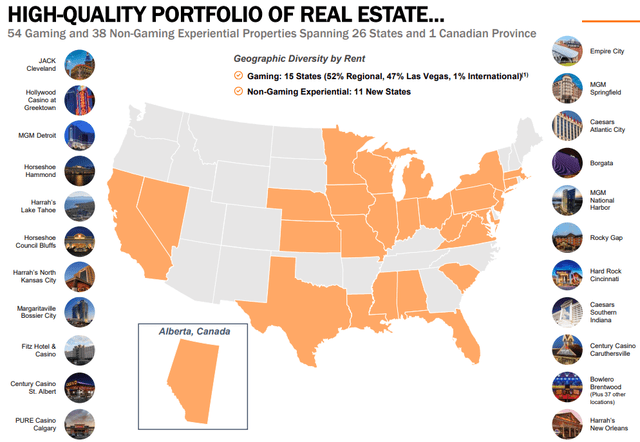

VICI, a prominent player in the gaming industry, possesses a vast empire of gaming properties, with a significant presence in Las Vegas, the entertainment capital of the world. Boasting a portfolio of 54 gaming properties and 39 experiential non-gaming properties scattered across 26 states and 1 Canadian Province, VICI’s reach is indeed extensive.

In addition to its core gaming properties, VICI strategically invests in non-gaming experiential real estate, including 38 family entertainment bowling centers obtained from Bowlero (BOWL) in 2023. The company also owns 4 championship golf courses and over 30 acres of developable land adjacent to the Las Vegas Strip.

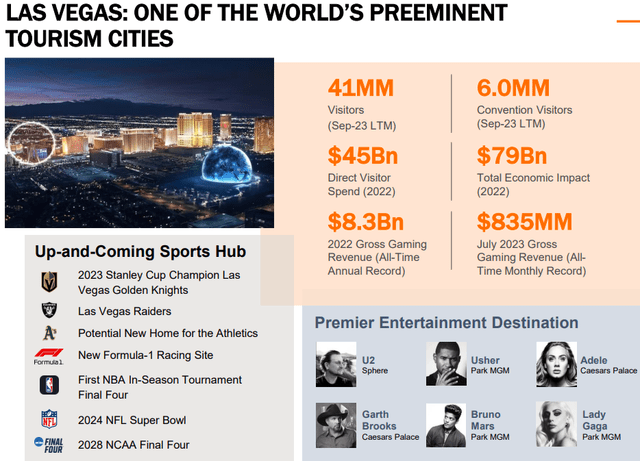

As Las Vegas continues to flourish, with record-breaking visitor spending in 2022 and a surge in gaming revenue, VICI is well poised to reap the benefits. The company’s strategic positioning with undeveloped land in prime locations and its foray into other experiential categories signal a promising future.

Furthermore, VICI’s expansion into states where gambling is restricted exemplifies its foresight and adaptability, as exemplified by the acquisition of bowling entertainment centers across 17 states in 2023.

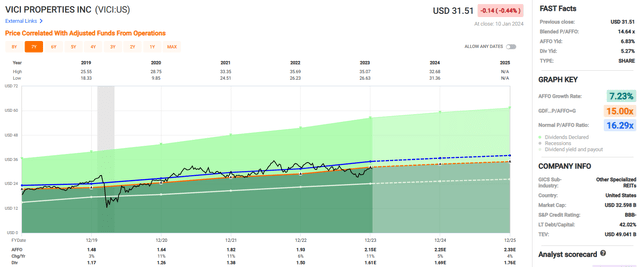

The company’s consistent and impressive growth rates, with an average AFFO growth rate of 7.23% and an average dividend growth rate of 10.11% since 2019, signify its financial strength. With an anticipated increase of 11% in AFFO per share in 2023, followed by 5% and 4% in 2024 and 2025 respectively, VICI’s growth trajectory seems appealing to investors.

VICI’s attractive dividend yield of 5.27%, well-supported by an AFFO payout ratio of 74.88%, coupled with a comparatively low P/AFFO ratio, make it a compelling prospect in the REIT landscape.

In light of these factors, we are bullish on VICI Properties and rate it a Buy.

Safehold: Pioneering Ground Leases and Residual Rights

Safehold (SAFE) stands out in the REIT arena with its focus on ground lease transactions, acquiring the land beneath commercial properties rather than the buildings themselves. This unique approach sets Safehold apart, providing long-term capital to commercial building owners and developers through sale-leaseback transactions structured on a triple-net basis.

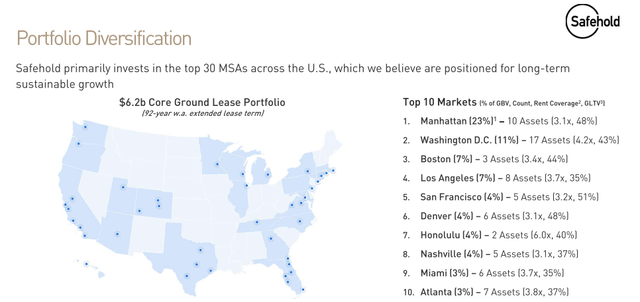

SAFE’s $6.2 billion ground lease portfolio, characterized by a weighted average extended lease term of 92 years, showcases its commitment to prolonged partnerships. With a stronghold in Manhattan, where it holds 10 assets constituting approximately 23% of its gross book value, SAFE’s market presence is substantial.

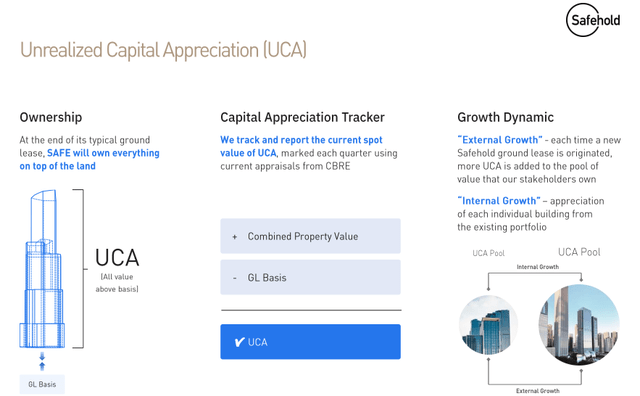

The company’s ground leases, spanning between 30 and 99 years, come with residual rights, allowing SAFE to assume ownership of the commercial property upon lease expiration or default by the building owner. This forward-thinking model not only secures SAFE’s position but also presents opportunities for potential capital appreciation.

Furthermore, SAFE’s innovative extension into Caret – a subsidiary aimed at monetizing the Unrealized Capital Appreciation (UCA) from its ground lease cost basis – underscores its ability to leverage and amplify its assets.

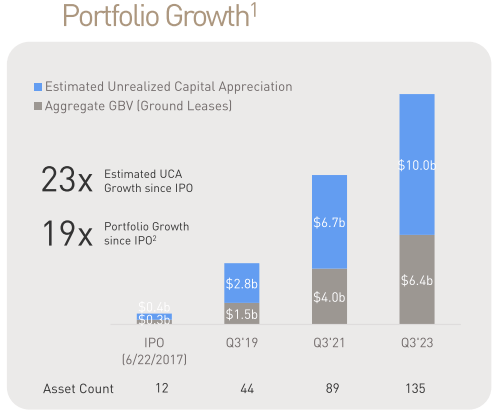

The rising demand for ground leases in the investment sphere indicates a promising trajectory for Safehold, as evidenced by its substantial growth from 12 ground lease assets in 2017 to 135 by the third quarter of .

In Conclusion

Both VICI Properties and Safehold present distinctive strategies and compelling value propositions within the REIT sector. VICI’s expansive gaming and experiential real estate portfolio, coupled with its projected growth rates and robust financial indicators, make it an appealing investment. Similarly, Safehold’s innovative approach to ground leases, residual rights, and the monetization of UCA heralds promising prospects in the commercial real estate landscape.

Real Estate Investment Trusts: Safehold and Realty Income

Safehold (SAFE)

Safehold Inc., a real estate investment trust (REIT), has shown remarkable growth since its Initial Public Offering (IPO). The estimated value of Safehold’s Underlying Contribution Amount (UCA) has surged twenty-three times over, skyrocketing from $0.4 billion in 2017 to approximately $10.0 billion today.

Potential for Growth

The lack of understanding surrounding ground leases and the monetization of UCA through Safehold’s Caret units presents an opportunity for growth. As businesses become increasingly informed about ground leases and their advantages, demand for Safehold’s offerings is likely to grow. The substantial value inherent in Safehold’s UCA is not adequately reflected in the current stock price. Furthermore, there is potential for value creation through the potential spin-off of SAFE’s subsidiary, “Caret.”

We rate Safehold a Strong Buy.

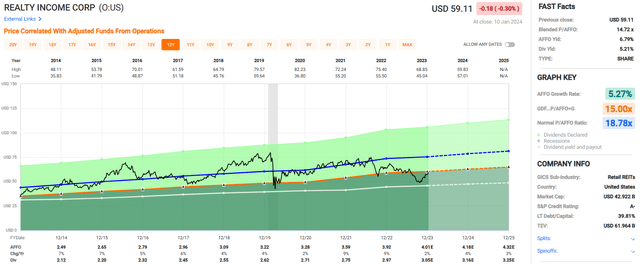

Realty Income (O)

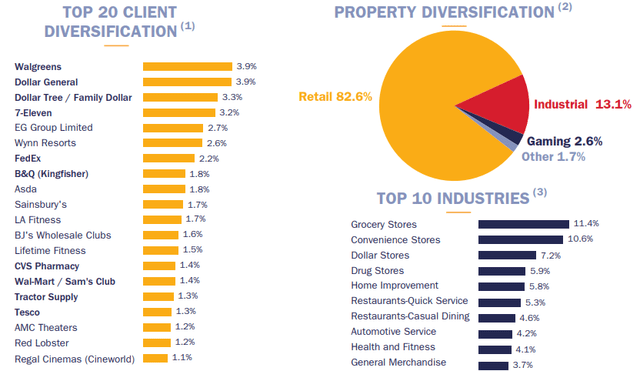

Realty Income, the largest net lease REIT with a market cap of nearly $43.0 billion, has a vast portfolio comprising single-tenant, free-standing commercial properties leased on a triple-net basis. With properties in all 50 states, the United Kingdom, Spain, Italy, and Ireland, O’s portfolio consists of approximately 13,282 commercial properties leased to about 1,324 different tenants across 85 separate lines of trade, including retail, industrial, and gaming properties.

At the end of the third quarter in 2023, roughly 82.6% of Realty Income’s total portfolio rent came from retail properties, 13.1% from industrial properties, and 2.6% from gaming properties. The company achieved a physical occupancy of 98.8% with a weighted average remaining lease term of about 9.7 years.

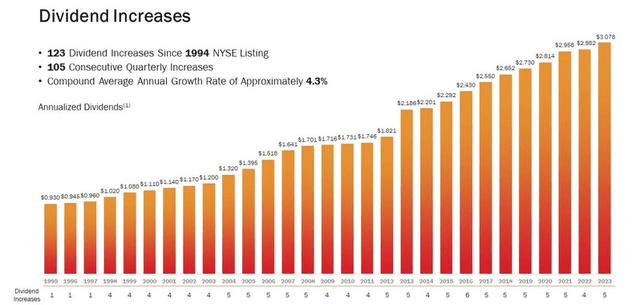

Realty Income is best known for its decades-long history of consistently paying monthly dividends. Trademarked as “The Monthly Dividend Company,” O has increased its dividend an impressive 123 times since going public in 1994 and has raised its dividend for 105 consecutive quarters. Recognized as a member of the S&P 500 Dividend Aristocrats, Realty Income boasts 29 consecutive years of dividend growth.

Consistent Growth

Realty Income sets itself apart as a consolidator in the fragmented net lease space, exemplified by its proposed acquisitions of Spirit Realty (SRC) and Vereit. With its robust portfolio and limited direct competition, O stands as a leader in the net-lease REIT sector. Its vast scale enables the company to take advantage of opportunistic deals that may be too substantial for other net-lease REITs to absorb.

Realty Income’s average Adjusted Funds from Operations (AFFO) growth rate of 5.27% since 2014 and its consistent dividend growth make it an attractive investment option. Analysts project a 4% AFFO per share growth in 2024 and 3% in 2025. With a well-covered 5.21% dividend yield, Realty Income presents an appealing investment opportunity.

We rate Realty Income a Buy.

In Conclusion

The decrease in interest rates stands out as a significant catalyst for REITs, as it impacts their cost of capital. This favorable trend is expected to support earnings growth for REIT investors. Furthermore, the three REIT consolidators, Safehold, Realty Income, and VICI Properties, offer sustainable growth prospects and attractive valuations.

Thank you for reading and Happy SWAN Investing!

Note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.