Analysis of Dividend Yield as an Investment Metric

In this piece, we will dissect the roller-coaster journey of Medical Properties Trust (NYSE:MPW) stock to underscore the perils of relying solely on dividend yields when evaluating investment prospects.

Every weekday morning, I dive into the financial analyses of 10 stocks even before my first cup of coffee. Then, during the day, I scrutinize additional stocks that pique the interest of my readers. With a portfolio of around 600 stocks, I immerse myself in various investment strategies to marry them with the most apt techniques for forecasting their future values. My frequent interactions with investors and exposure to diverse stocks have unveiled patterns that often go unnoticed. One such pattern is the tendency of investors to kick off their stock evaluations by fixating on a stock’s dividend yield.

Why is this approach hazardous? Using the dividend yield as a primary indicator and adhering to a popular investing strategy, such as dividend investing, invariably leads to subpar long-term returns. Savvy investors seeking lucrative returns ought to steer clear of these pitfalls.

Unwarranted Prevalence

For the past two years, Medical Properties Trust has consistently hogged the limelight on Seeking Alpha’s trending page despite being a relatively obscure entity in the stock market. To put this into perspective, MPW’s market cap was only half the size of Lincoln National (LNC), the smallest business by market cap in the S&P 500 in 2023 before its removal from the index.

During this period, MPW’s stock price exhibited similar trends to the diminutive LNC. Yet, MPW has garnered ten times the number of articles on Seeking Alpha compared to LNC over the past three years. Moreover, MPW boasts over 82,000 followers on SA, while LNC hovers around 15,000. What accounts for this glaring popularity gap, especially considering MPW has never secured a spot in the S&P 500 index? The main driver appears to be MPW’s dividend yield, which has consistently been 2 to 4 times higher than that of LNC.

In essence, had investors not fixated on MPW’s dividend yield, the stock would have likely faded into relative obscurity alongside numerous other failed stocks over the past few years.

The extraordinary attention on MPW is not an isolated case. T-Mobile’s (TMUS) ticker has approximately 70,000 followers, while AT&T (T) and Verizon (VZ) command 567,000 and 358,000 followers, respectively. The appeal of AT&T and Verizon, both historically high-yielders, is evident, whereas T-Mobile, which lacks a dividend, trails behind. Let’s delve into their overall stock performance in the past decade:

Over the last decade, T and VZ have delivered returns roughly in line with inflation, equating to stagnant real returns for investors. In contrast, their competitor TMUS generated returns exceeding tenfold. The rationale for the sizable followings of T and VZ, relative to TMUS, can be attributed to the former’s higher-than-average dividend yields.

Culprit: Placing Emphasis on Dividend Yield

In any prudent stock or business analysis, dividends should figure as one of the final considerations. Dividends emanate from earnings and are not additional to earnings. Starting an evaluation or screening of a stock with its dividend yield, dividend record, or dividend growth constitutes a grave error.

Why is this erroneous?

There are two critical reasons. Firstly, dividends are derived from earnings and cash flows. A company must first generate profits before it can dispense dividends. Typically, it is optimal for a company to reinvest its earnings in the existing business to fuel growth. Should this prove unfeasible, the company can channel its earnings into debt reduction, expansion through acquisitions, stock buybacks, or dividends.

Berkshire Hathaway (BRK.A) (BRK.B) stands as a testament to significant growth sans dividend payments. Over the long term, the market places little emphasis on dividends. Otherwise, Berkshire Hathaway wouldn’t warrant its current lofty valuation.

Analysis of Dividends and REITs in the Stock Market

Dividends rarely matter to the long-term valuation of a business in the stock market. Focusing primarily on dividends when evaluating a stock is akin to filtering life partners by eye color—limiting and potentially detrimental. Instead, investors should prioritize analyzing the earnings and cash flows of a company for sustainable growth. Historically, dividend investing has garnered undue attention, leading to an investing bubble that is likely to gradually dissipate.

The Psychological Pitfalls of Emphasizing Dividends

While dividends may provide psychological comfort during market downturns, they can also lead investors to overlook a company’s fundamental weaknesses. The allure of high dividend yields amid stock price declines can mask inherent risks, potentially clouding judgment and fostering unwarranted positivity towards underperforming businesses.

Impact on Market Performance

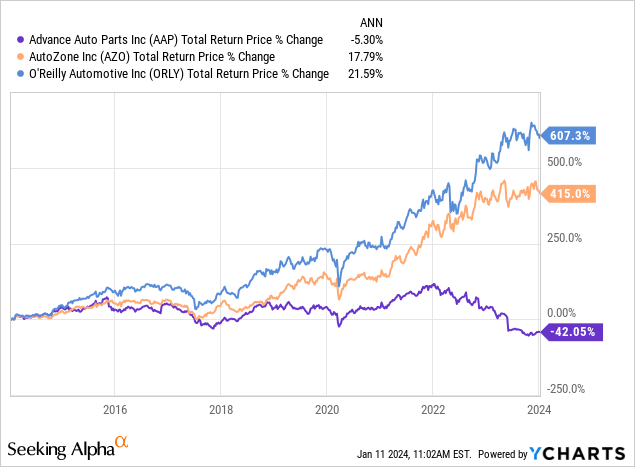

Analysis of the market performance of AutoZone (AZO), O’Reilly (ORLY), and Advanced Auto Parts (AAP) exemplifies the disparity between stock popularity and financial success. Despite similar analyst ratings and reader interest, the dividend status significantly influenced their stock performance, demonstrating the misleading nature of relying solely on dividends for investment decisions.

The disparity in market performance underscores the need to assess a company’s financial health beyond its dividend offerings. Earnings and cash flows should always remain the primary indicators of market value.

Medical Properties Trust & REITs

Real Estate Investment Trusts (REITs) operate within a distinct market dynamic, heavily reliant on interest rates and credit conditions to maintain a positive feedback loop for sustained asset and stock price appreciation. However, the reliance on dividends to attract investors creates a precarious investing environment, particularly when these factors falter.

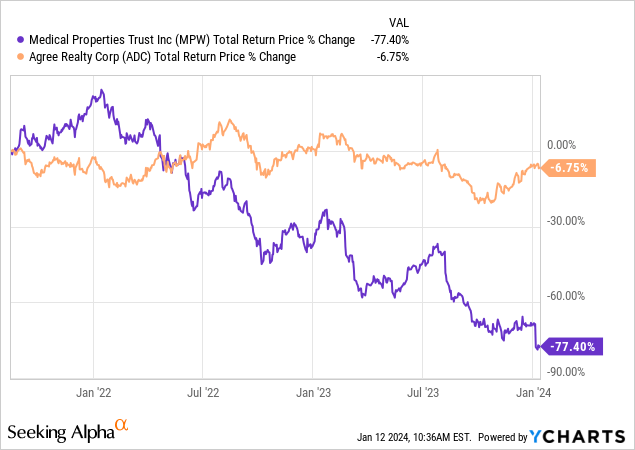

For instance, the case of Medical Properties Trust illustrates the complexities of REIT investing, where vigilant monitoring of market behavior and early corrective actions are essential for mitigating potential losses. A strategic shift can safeguard against substantial declines and minimize investment risks, as demonstrated by a preemptive divestment in favor of a more favorable REIT.

This strategic maneuver underscores the critical importance of continuous analysis and adaptability in navigating the volatile landscape of REIT investments.

The prolonged bullish sentiment towards Medical Properties Trust highlights the prevalence of misinformed investing psychology, shedding light on the broader implications of dividend-centric investment strategies.

Ultimately, diligent evaluation of market fundamentals, prudent risk management, and a discerning approach are indispensable for navigating the intricate terrain of dividend investing and REITs.

The MPW Stock Saga: Dividends, Technicals, and Investment Lessons

When it comes to the dramatic rise and fall of Medical Properties Trust (MPW), it seems like everyone has an opinion. The stock gained widespread attention after a series of ‘Buy’ and ‘Strong Buy’ articles flooded financial columns. However, it wasn’t until March 2023 when the stock was already down -65% off its highs.

I want to give kudos to both Peter F. Way and Colorado Wealth Management for their sell calls on MPW. I almost never comment on other authors’ articles (because I’m usually busy answering comments on my own), but I took the time to comment on Colorado’s article “The Only Bear On Medical Properties Trust” about a year and a half ago, and I think it was the last comment on another author’s article I’ve left. To put these bearish articles in context, there were 3 “Sell” articles written before MPW had a significant decline, while, by my quick count, there have been 168 “Buy” or “Strong Buy” articles written since 2021 on the way down. So, while I’ve never written on MPW publicly before, I have been fascinated by it for several years now.

REIT Dividends Vs. Technicals

While I’m not going to share my entire REIT strategy here, I will provide a couple of pointers for investors who dislike losing money. When a REIT is both -20% or more off its peak, and below the 200-day simple moving average, investors are usually better off selling at that point in time. For MPW, this happened on 4/22/22, which is when both conditions were met.

Above, we can see that it is below the 200-day simple moving average.

At the same time, the stock price was more than -20% off its high. That made it a “Sell” at that point in time.

It should not have mattered that the dividend yield was above 6% at that time. Here are the total returns since then:

Putting This All Together

I am a firm believer in closely studying one’s mistakes in order to improve as an investor. Those who don’t do this will continue to make the same errors over and over again. It’s even better if one can learn to avoid mistakes by watching others instead of making those mistakes personally. So, my hope is some readers will read this article and be able to avoid mistakes like MPW in the future. Here are my takeaways.

- When a company has any sort of unusual accounting or business activity, sell first, and ask questions later. It doesn’t matter what you paid for it and the loss you might take. Sell right away and never give management the benefit of the doubt. There are plenty of good businesses that don’t have these issues one can invest in.

- REITs are financially sensitive and deeply cyclical investments. When the stock prices fall more than -20% off their peaks, basic technicals break down, and the wider economy is in a late-cycle environment, sell those REITs quickly, and don’t buy them back until we are early cycle again.

- Don’t try to buy turnaround stories before they have actually turned around.

- Totally ignore the dividend when deciding to invest. Pretend it isn’t there. Sure, the dividend will ultimately be part of the total return, but it will be more likely to cloud your judgment about the quality of the business and stock.

I want to drive home this last point about dividends the most. After following this stock for 3 or 4 years, it is plainly obvious nobody would even know it existed if they didn’t start first by looking at the dividend yield. The fact that investors have poured so much time, energy, and money into this stock is, frankly, a travesty. The dividend bubble we find ourselves in is mostly to blame. Seeing a high dividend is like hearing a siren song for investors, and my experience the past few years is that entire fleets of retirees are sailing for the rocks. Odysseus had the sense to strap himself to the mast and fill his men’s ears with wax in order to avoid the disaster that had claimed so many others. Dividend investors would be wise to do the same and not begin their analyses by looking at the dividend yield.