Dear readers/ followers,

Let’s talk about Lufthansa. This airline company has not been soaring in the market, not by a long shot. In fact, the company has been descending faster than a lead balloon, declining by 2.4% RoR while the market takes off almost 29%. That’s a 30% difference that’s hard to ignore. But despite this downward spiral, I remain unmoved in my apathy towards this company, as well as other pure-play airlines. I’m an investor in companies that own planes, such as Exchange Income Corp (OTCPK:EIFZF) or TUI (OTCPK:TUIFF), but when it comes to pure-play airline companies, I align with Warren Buffett’s sentiment that they are not the most attractive investments.

Is there a price at which I’d consider investing in Deutsche Lufthansa? Yes, there is. But for now, let’s delve into why I find pure-play airlines such as Lufthansa unappealing.

Lufthansa’s Outlook for 2024E

Lufthansa has been nothing but trouble from an investment viewpoint. It’s one of the very few companies that I have given a “Sell” rating to, and that decision has paid off thus far. And things haven’t changed much with the latest updates. Some analysts might see an upside to this company, but I don’t share their optimism.

On the surface, Lufthansa seems like an attractive play. It has control over some key central-European airlines, including geographies like Switzerland, Austria, and BeNeLux. It carries the Star Alliance brand and provides travelers with an extensive network of destinations. But even with these strong assets, the outlook for the airline industry as a whole is unappealing, especially when considering the addition of the logistics operator Eurowings. It’s not the company’s geographical exposure or its Germany-heavy operations that concern me; it’s the anticipated future of the company in a forecast with no expected improvement in earnings.

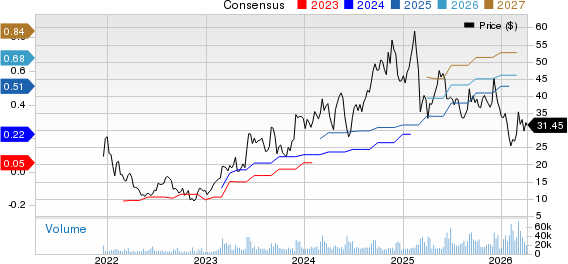

The current company expectation is a flat EPS beyond 2023, possibly growing by 1-2%. This forms the basis of the bearish thesis that I support at this valuation. While Lufthansa is profitable, the business model, in my opinion, lacks attractiveness, especially when a substantial portion of revenue translates to a sub-3% net income. This kind of low margin in a highly cyclical industry just doesn’t pique my interest.

But I’m not all doom and gloom. Lufthansa does have some positive aspects. For one, the company has regained its BBB rating from leading agencies. It has also concluded sale/leaseback transactions and ordered 80 new aircraft, split evenly between Airbus and Boeing. However, I’m more inclined towards Airbus due to my reservations about Boeing’s recent track record. In addition, the latest quarter has shown positive results, positioning the company for a full-year adjusted EPS of over €1.5, which is a forecast I stand by. But even with these improvements, I find the company unattractive in its current state.

Fundamental improvements such as a reduction in net debt and pension liabilities are only small positives in a picture I consider fairly negative, or at best, flat for the near term. The company’s good FCF has brought the debt on an adjusted EBITDA down to below 1.5x, which explains the rating increases, but even so, I remain unconvinced of the company’s appeal.

Deutsche Lufthansa – Navigating the Turbulent Skies of Investment

Amidst the volatile landscape of the airline industry, Deutsche Lufthansa has been a topic of both speculation and skepticism. With an impressive order book, emission reduction targets met, and strategic vision for the future, the German carrier aims to chart a course for growth and greater efficiency. However, as investors ponder its investment potential, there are conflicting views about its future trajectory.

The Company’s Strategic Outlook

Deutsche Lufthansa’s approach to customer value and sustainability in the airline industry is much like a craftsman shaping a fine sculpture – meticulous and precise. Despite the company’s promising endeavors, skepticism looms over its investment potential.

Valuation Analysis and Investment Considerations

As an astute navigator meticulously considering every factor that influences the flight path of an investment, analysts have scrutinized Deutsche Lufthansa’s valuation with an eagle eye. The company’s potential upside is clouded in uncertainty, with its historical returns signaling caution to prospective investors.

Insightful Investment Thesis

Through a nuanced lens, considering all the complexities and intricacies like a seasoned pilot in the cockpit, the investment thesis for Deutsche Lufthansa comes into view. With a judicious outlook, the company’s potential for a turnaround is juxtaposed against its historical performance and market sentiments.

Adopting a Discerning Investment Approach

Like a shrewd investor scanning the stock market landscape for nuggets of promise, the investment strategy regarding Deutsche Lufthansa is rooted in cautious optimism. The path to realizing its investment potential is riddled with potential pitfalls and uncertainties.

Key Investment Criteria Evaluation

Amidst it all, the assessment of Deutsche Lufthansa’s investment worthiness hinges on a confluence of comprehensive criteria, much like contemplating the intricate facets of a multifaceted gemstone. However, the company’s current standing fails to align with the stringent investment benchmarks set by astute analysts.

As the clouds of uncertainty gather around Deutsche Lufthansa’s investment potential, the company’s future remains a matter of spirited debate among investors. The push and pull between optimism and skepticism have set the stage for a riveting investment saga in the airline sector.