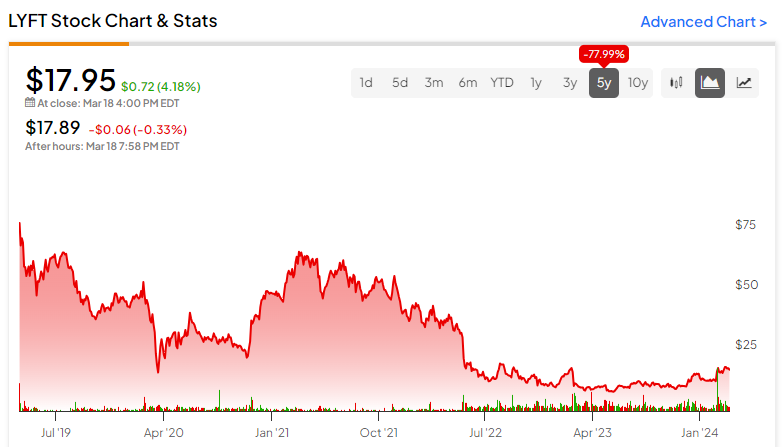

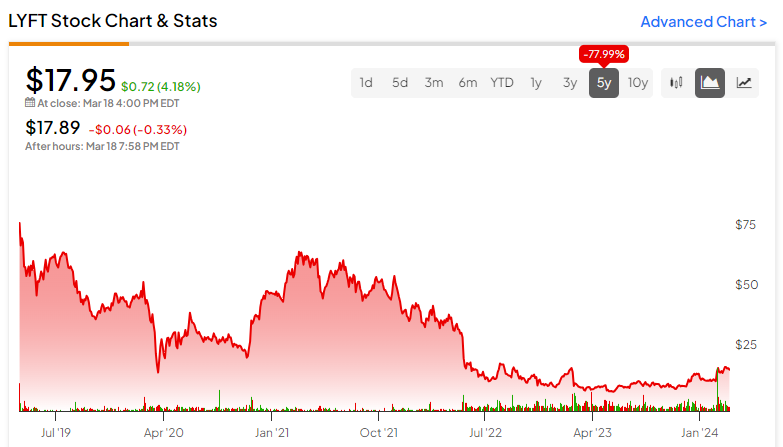

At first glance, Lyft (NASDAQ:LYFT) may seem like a promising underdog in the ridesharing industry, standing in the shadow of its Goliath counterpart Uber (NYSE:UBER). Positioned to capitalize on economic recovery tailwinds, Lyft presumably rides the coattails of a growing market. However, should market conditions tighten, the risk of commoditization looms large over the ridesharing sphere. In such a scenario, Lyft’s lack of competitive differentiation could render it a lackluster contender. As the narrative stands, skepticism shadows LYFT stock.

Financial Evaluation: The Contrasting Fortunes of LYFT and Uber

A nuanced examination of Lyft’s financial standing reveals an undervalued stock in comparison to its formidable rival Uber. Presently, Lyft shares hold a forward earnings multiple of 42x and a trailing-year sales multiple of 1.51x. In stark juxtaposition, UBER commands a forward earnings multiple nearing 60x and a revenue multiple of 4.3x.

Given the head-to-head comparison between these direct competitors, LYFT stock seems to furnish a more appealing investment prospect. Moreover, occupying a smaller market cap of $6.88 billion vis-à-vis Uber’s $158 billion, Lyft is naturally poised to snag a larger share of the burgeoning ridesharing market.

The ridesharing domain paints a vibrant landscape, poised for a compound annual growth rate of 16.3% from 2021 to 2028, culminating in a sector worth of $242.73 billion, as per Fortune Business Insights. Another report by Straits Research envisions an even more buoyant outlook, forecasting a CAGR of 20.38% from 2023 to 2031, elevating the industry value to $564.2 billion.

In essence, ridesharing remains a sizzling sector, with LYFT stock manifesting as a lucratively undervalued play relative to UBER.

In a nod to optimism, Lyft’s Q3 earnings report unveiled an adjusted EPS of 19 cents, surpassing the consensus EPS estimate of 8 cents. Additionally, the company recorded revenue of $1.22 billion, aligning with market projections. Noteworthy is Lyft’s staggering average positive earnings surprise of 531.6% across Q1 through Q4.

Looking ahead, analysts project Lyft to amass revenues of $5.13 billion in the current fiscal year, escalating by 16.5% from the previous year’s $4.4 billion. For Fiscal 2025, revenue forecasts stand at $5.76 billion, signifying a 12.3% year-on-year upswing.

Nonetheless, the trailing price-to-sales ratio of 1.51 raises cautionary flags.

Uber: The Growth Maestro Stealing the Limelight

Delving into earnings performance, Uber seemingly presents a mixed bag. In its Q3 earnings disclosure, Uber reported an EPS of 10 cents, falling short of the anticipated 12 cents. Crucially, Uber boasted GAAP profitability last year, a feat eclipsing Lyft’s non-GAAP adjusted profitability due to operational deficits.

The crux of concern centers on Uber’s trajectory of growth. By the fiscal year’s end, market analysts foresee Uber’s revenues soaring to $43.28 billion, a 16.1% lift from the preceding year’s $37.28 billion. Looking further into Fiscal 2025, experts envision Uber’s revenue scaling to $50.4 billion, a 16.4% surge from 2024’s prognosticated revenues.

Herein lies the rub: despite its heftier proportions, Uber is poised to outpace the smaller, more agile Lyft in expansion. Maneuvering a smaller entity up the growth ladder typically requires less effort, yet analysts predict Uber’s titanic expansion to outshine Lyft’s nimbleness.

This juxtaposes LYFT stock as a budget Maserati: an automotive marvel renowned for its exquisite design, akin to Modena’s prized export. Nonetheless, the caveat with Maserati is the peril lurking beneath: cruising the highway delightfully one moment, engulfed in flames the next.

Granted, LYFT stock garners a semblance of bargain next to UBER. However, if the latter guarantees reaching one’s destination, the premium is undoubtedly warranted.

Risk of Commoditization Looming Large

In the eventuality of an economic deceleration, LYFT stock appears susceptible to downside pressures. Beyond the lack of GAAP profitability, Lyft’s innovation narrative lags behind Uber’s diversification thrust, extending into disruptive forays, including the shipping arena. Conversely, Lyft contentedly stands as an alternative to Uber.

Thus far, Lyft’s comparative performance has held steady. Nevertheless, economic vicissitudes could cast Uber’s diversified profile as a shield against inclement conditions, leaving Lyft to grapple in an increasingly homogeneous field. Such circumstances pose additional hurdles that taint the allure of LYFT’s discounted metrics.

Analysts’ Vantage Point on LYFT Stock

Per Wall Street sentiment, LYFT stock carries a Hold consensus, reflecting four Buys, 24 Holds, and two Sells. The average price target for LYFT stock stands at $15.75, marking a 12.3% downside potential.

In Conclusion: The Perplexing Dynamics of LYFT Stock

Between the duo, LYFT stock beckons with a more alluring valuation juxtaposed against UBER. Yet, the looming question pertains to analysts’ foresight of a more robust growth trajectory for the larger corporate behemoth. Fueled by Uber’s expansive ventures, this prognosis isn’t entirely startling. Meanwhile, Lyft’s niche ride-sharing model, though successful thus far, faces mounting threats of commoditization should economic winds shift unfavorably.

Disclosure

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.