Sekisui’s Acquisition of M.D.C. Holdings

Shares of M.D.C. Holdings (NYSE:MDC) have shown a robust performance over the past year. Shareholders received substantial gains on Thursday due to Sekisui’s proposal to acquire the company, resulting in an 18% rally. Under the agreement, Sekisui (OTCPK:SKHSY) will pay $63 per share in cash. With shares already hovering within 0.5% of the price, this deal looms as an attractive proposition, but with limited upside. Any remaining upside would be a rather thin gruel for investors.

Reasoning Behind the Acquisition

M.D.C. Holdings is a mid-sized US homebuilder with a focus on first-time homebuyers, offering homes at an average price of about $550k as of the third quarter. It has delivered nearly 8,400 homes over the past year and operates 235 active subdivisions, primarily across the Western United States with additional exposure in the Sun Belt.

The rationale for the acquisition becomes apparent when exploring Sekisui’s US business, which operates across a very similar footprint, focusing primarily on the middle and lower end of the US housing market.

By integrating M.D.C., Sekisui will bolster its presence in familiar markets, with the increased scale likely providing synergies to cut costs and enhance margins. Despite being a primarily Japanese builder, Sekisui has been seeking expansion in the US to diversify revenue, making this purchase critical in achieving its goal of building 10,000 homes in the United States by 2025.

In June 2022, Sekisui announced its acquisition of Chesmar, which added just over 2,000 homes to its portfolio. Coupled with its Woodside and Holt Group brands, which together build over 3,000 homes, Sekisui was at around 5,000 units of capacity. The addition of ~8,400 units from M.D.C. would push the company beyond its 10k unit goal. Notably, M.D.C. was ranked as the 11th largest US homebuilder by volumes, and the combined entity is poised to become the 5th largest.

The move by Sekisui is a tacit endorsement of the robust US housing market, which has been a fertile ground for opportunity in recent times. As housing supplies remain constrained, it has been a thriving sector that has defied expectations. With the Federal Reserve potentially cutting rates, the market could experience renewed demand, further benefitting builders like Sekisui.

This begs the question: with prices resilient amidst higher rates and the potential for renewed demand, could the market catapult itself into sustainable growth?

The Potential Roadblocks

In any M&A deal, concerns loom about the deal being blocked or the emergence of another suitor sparking a bidding war. Considering the downside risk first, the market’s confidence in the near-certain completion of the deal is evident, with shares inching perilously close to the $63 mark.

There has certainly been enhanced antitrust scrutiny across all deals in recent years, as evidenced by the Spirit Airlines (SAVE) and JetBlue (JBLU) saga. However, in the case of Sekisui and M.D.C., where the combined market share remains a mere 1%, it is difficult to conjure a plausible antitrust argument. With only about 1% market share and several larger players in the industry, it is challenging to see any viable antitrust concerns here.

A lingering risk is the acquisition of a US firm by a foreign company, which may invite additional scrutiny. However, considering Sekisui’s snag-free acquisition last year, a similar outcome is anticipated in this case. The recent political uproar surrounding Nippon Steel’s proposed acquisition of US Steel may raise some eyebrows, but the stark differences between the industries and companies involved make a similar response unlikely.

Regulatory challenges for this deal, from both antitrust and foreign investment angles, are improbable, especially with no financing conditions attached, ensuring a seamless deal closure by 6/30/24 or possibly even sooner.

Prospects of a Rival Bidder Emerging

While the downside risk from the $63 purchase remains minimal, the emergence of another bidder to justify owning shares seems unlikely. Founders Larry Mizel and David Mandarich, with a collective 21% ownership, have already thrown their weight behind the deal, tipping the scales heavily in favor of Sekisui.

The Thought-Provoking Push and Pull of the MDC Holdings Acquisition

Despite skepticism surrounding MDC Holdings’ founder-influenced stake, the decision to sell to Sekisui has drawn mixed reactions. Is this a prudent move or a missed opportunity for MDC Holdings?

Examining the Transaction

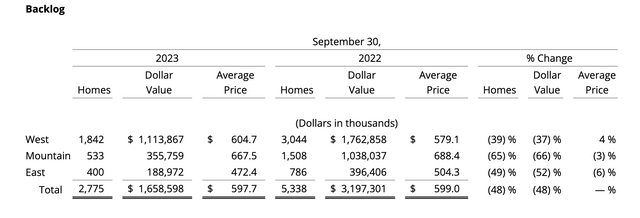

MDC Holdings seems to have found solace in the arms of Sekisui, regarding the acquisition as a fair deal. With MDC earnings in the third quarter totalling $1.40 and a notable drop in revenue from $1.4 billion to $1.1 billion, the company faced significant challenges. However, the potential for a prosperous future emerges as MDC is estimated to earn about $5.25 this year, supported by a 12x selling price in 2023 earnings and approximately 1.4x book value, which portrays a sturdy valuation. The acquisition also infuses added scale, with 235 active communities and 17,800 owned lots in MDC’s arsenal.

The company’s backlog of 2,775 units may have dipped by 48% from the previous year, but it assures a steady revenue stream for 2024. Moreover, recent data indicates a revival of activity, marked by the notable increase in new orders, predominantly in the West. The purchasing power of Sekisui aligned with the declining building costs paves the way for potential margin improvement and operational synergy. MDC, in turn, offers financial robustness, boasting $1.8 billion in cash and securities against a mere $1.5 billion in debt, positioning it in a net cash stance.

Comparative Analysis and Market Speculations

It is important to note that the selling price places MDC Holdings in a favorable light in comparison to its industry peers. Crunching numbers, the 12x earnings and 1.4x book value make for an appealing proposition. For instance, KB Home, a competitor of MDC Holdings, trails with a trading valuation just below 9x 2023 earnings and approximately 1.2x book value. The discrepancy in net debt between the two may contribute to this variance, driving home the significance of financial decisiveness in corporate perambulations.

Market foresight shadows the transaction, with indicators suggesting that most homebuilders trade around 10x earnings. Foremost among their strategic pursuits is channeling cash flow into share repurchases rather than engaging in mergers and acquisitions, especially at such valuations. It is also crucial to appreciate that public companies often fall short of premium M&A prices, accentuating the uniqueness of Sekisui’s rationale for the acquisition. This distinctiveness arguably places KB Home at a distance from achieving MDC’s multiple.

Final Reflections

The denouement of the MDC Holdings acquisition has unfurled a buoyant year for its shareholders. Nonetheless, the prevailing reticence in share prices undermines the rallying sentiment. Assuming a ~3 month close, investors are looking at an approximate annualized return of 5%, when factoring in one more dividend payment. This tepid yield beckons a lingering question–with a yield comparable to a treasury bill, is the capital market gauging the deal’s conclusion with rightful skepticism? The market bears witness to a palpable premium teetering on the edge of certainty, compelling shareholders to reckon with the allure of solid profits against the backdrop of evaporating equity risk premiums. The high time has arguably come to part ways, crystallizing the decision to relinquish shares, claim the dividend, and direct one’s gaze toward greener pastures.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.