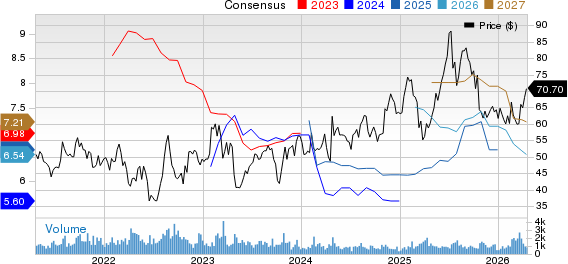

Stocks are soaring to new heights, seemingly propelled by remarkable optimism about the economy and better-than-expected earnings in the last quarter. However, amid this rapid ascent, concerns loom large. The continuation of this stock rally hinges on perennial factors – the economy and earnings. This article delves into five crucial macro themes that wield immense power over the future trajectory of stocks.

The Inflation Conundrum and Labor Market Dynamics

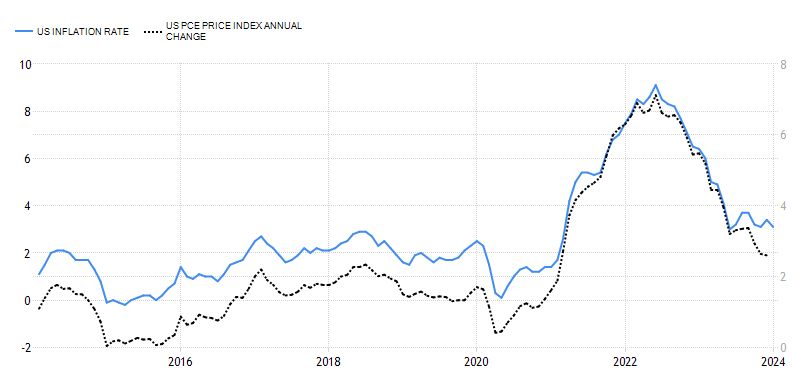

In the wake of the Covid-19 crisis, factors such as pent-up demand for services and supply chain disruptions led to an inflation shock in 2021-22. However, with the Fed’s aggressive tightening, prices have been rapidly decelerating. Yet, a recent CPI print suggests that the battle against inflation is far from over, primarily due to persistent price stickiness in shelter expenses. The length of the remaining inflation fight may necessitate the central bank to maintain higher rates for a prolonged period.

Interestingly, the once widely accepted Phillips Curve theory, which posits an inverse relationship between the job market and inflation, now appears outdated. While inflation is on a downward trajectory, the labor market exhibits robust health, with robust hiring and accelerated wage growth. However, the sustainability of this disinflationary trend remains ambiguous, with potential triggers such as rising wages or services costs posing a risk. As market participants anxiously await PCE inflation data at month-end, significant policy implications might hang in the balance.

Source: Trading Economics

As we navigate these economic crosscurrents, vigilance will be critical, as it is no longer business as usual in terms of market dynamics and the implications for inflation-control measures.

Consumer Spending: A Key Pillar of Economic Growth

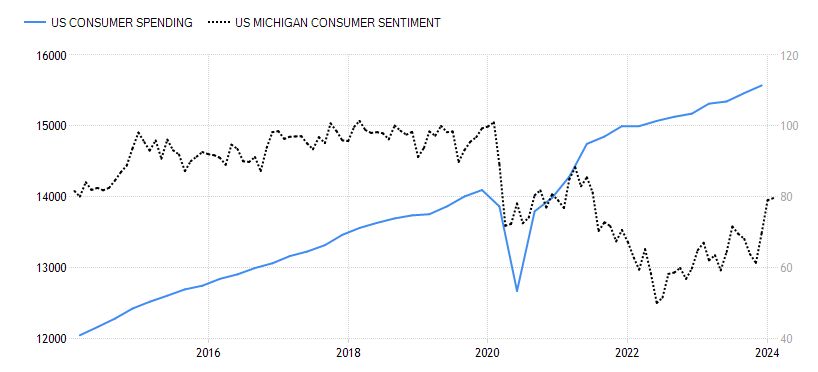

In the U.S., consumer spending is the bedrock of developed economies, comprising 70% of the GDP. Despite mounting concerns about household debts in the face of high interest rates, U.S. personal consumption has displayed astonishing resilience. Household debts have remained largely unchanged, and the surge in disposable personal income has assuaged fears that burgeoning interest on debt would stifle consumption. Furthermore, various consumer loan categories, including credit card debt, now represent a smaller proportion of disposable incomes than pre-pandemic levels, with delinquencies inching up from the ultra-low floor.

Historically, the consumer sentiment index has been a reliable gauge of short-term spending trends. However, this familiar barometer now appears increasingly erratic in the post-pandemic landscape, with rising consumer spending defying waning sentiment. As consumer confidence stages a robust recovery, the dissonance between sentiment and spending underscores the complexity of today’s economic realities.

Source: Trading Economics

While the robustness of the American consumer warrants acknowledgement, it is essential to recognize the influence of stock market movements on consumer sentiment. The euphoria surrounding the S&P 500’s record-breaking streak has undoubtedly buoyed consumer confidence. However, amidst the current exuberance, it is paramount to remain cognizant of potential market irrationality that could resuscitate inflationary pressures.

Unpacking Economic Growth: Striking the Right Balance

Amid the notable retreat of recession concerns, even the most bearish strategists have revised their outlooks to align with this newfound reality. Notably, the prevailing consensus echoes the “Goldilocks” narrative – an economy that is neither too hot nor too cold, but just right. However, this consensus simplification could overshadow nuanced data that might underpin a bear case.

The boons that drove inflation surges in 2021-22 also fueled post-pandemic growth spikes, compelling the Fed to embark on a tightening crusade. However, mounting rate hikes and the resultant financial tightness, alongside waning economic sentiments, precipitated a significant deceleration in GDP growth in 2022. As we navigate these economic crosscurrents, vigilance will be critical, as it is no longer business as usual in terms of market dynamics and the implications for inflation-control measures.

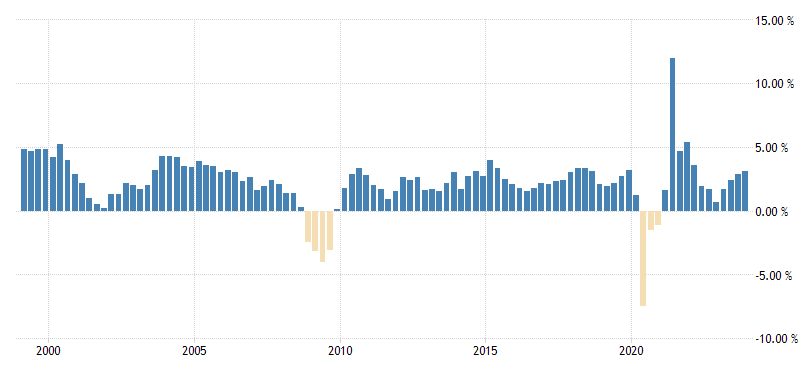

Insight into 2024 Economic Growth Prospects

Economic growth has been on a strong upward tilt in 2023, reaching its 75-year average of 3.1% in the last quarter.

Source: Trading Economics

However, true economists will always find a reason for concern. Growth forecasts have been moving higher lately, and, according to the Atlanta Fed’s “GDPNow” estimate, this quarter’s growth will reach 3.4%. Some components of the index, such as employment numbers, manufacturing and services growth, construction spending, and others, paint an even hotter outcome, while simultaneously lifting the inflation outlook, too.

So, while we enjoy this Goldilocks moment, we must acknowledge that a hotter-than-needed economy may lead to resurging inflation. If that happens, we may find ourselves in a situation where the Fed needs to induce a recession to squash inflation.

Federal Reserve: Feasibility of Rate Cuts

Goldilocks got a little burned by the latest CPI inflation report, which came in too hot to fit the narrative. Although we shouldn’t focus too much on a single, albeit crucially important, data point, it shouldn’t be dismissed either.

Policymakers are in a tight spot, as underneath the surface of the economy’s ruddy health, different economic subsectors are impacted by high interest rates (at the moment, the worry du jour is regional banks’ exposure to the reeling commercial real estate market). Still, these pockets of distress are very local and easily manageable, presenting far lower risk than that of a premature cut reigniting inflation. History tells us that the economy will be much better off with higher rates lingering for a while, than with a cut followed by a spike in prices, which would lead to another hiking avalanche.

Further rate increases are out of the question unless the Fed’s favorite inflation gauge, the PCE, shifts strongly upward, or the economy shows concise signs of overheating. On the other hand, there is no immediate pressure to cut, given the robust labor market and consumer strength. Besides, the stock market rally leads to looser financial conditions and the money surging freely through the economy heats it up, counterweighing the central bank’s efforts. In short, policymakers want proof that inflation is tamed before they make their first cut. That’s going to take a while.

Corporate Earnings: AI Love U

One of the most important drivers of the stock-market rally has been corporate earnings, whose resiliency in the face of higher rates surprised analysts and economists.

The fact is that large corporations represented by the S&P 500 index locked in low-interest rates on their debt during the near-zero rates era, reducing the threat of high debt servicing costs. Coupled with various cost-cutting efforts and improved operating efficiencies, this has helped companies to counter elevated input prices, while expanding their profit margins. In addition, many large companies were able to pass higher costs on to their customers, reaching record profits along the way.

Building on these achievements, stocks of the SPX firms were further lifted by the Artificial Intelligence (AI) narrative, which took the world by storm. Besides all other expected effects, AI is anticipated to further increase corporate efficiency, considerably upping bottom lines for years to come. No wonder that the rally has been led by tech stocks, the drivers of the coming AI revolution, leading many to ponder about its similarity to the dot-com boom.

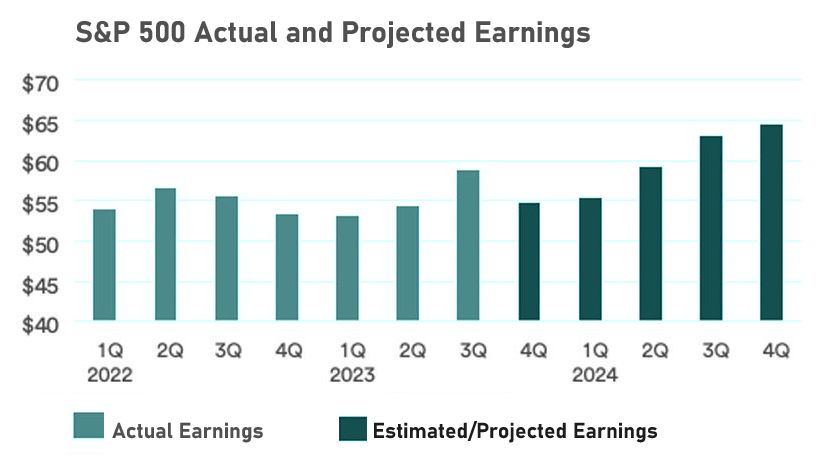

Source: FactSet

While it might be the case that the technology stocks have run ahead of themselves, numbers don’t lie; corporate earnings have been very strong and are slated to continue their upward march. Roughly three-quarters of the S&P 500 firms have reported their Q4 2023 results, with earnings up almost 6% year-on-year. However, the earnings positivity in the previous quarter was contributed by the megacap technology companies, while most other sectors’ earnings are expected to rebound only further along the road.

Analysts expect SPX earnings to increase by 10% in 2024, followed by 12% growth in 2025. However, outside of the tech megacaps, strong earnings growth remains in question, as it faces challenges from elevated interest rates, while economic growth is expected to moderate this year. In short, earnings will continue to be impacted by the economy and inflation – and, since earnings are the most important driver of stock prices, the stock market’s direction will hinge on economic performance. In short, stay tuned.