Food for Thought

“Joy comes to us in moments—ordinary moments. We risk missing out on joy when we get too busy chasing down the extraordinary.”

– Brené Brown, Daring Greatly

The Bird’s Eye View

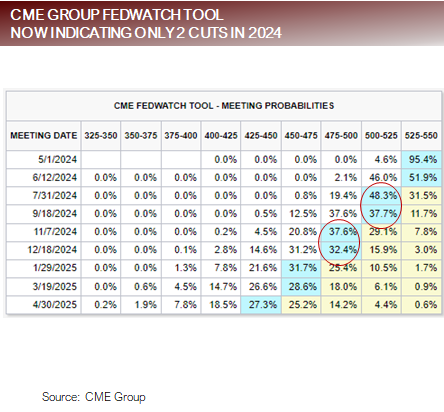

Last week’s significant events included the ISM Purchasing Manager Survey data, affirming an uptick in manufacturing and employment figures signaling a continuation of the robust job market that has been fueling consumer spending. Diplomatic tensions in the Middle East have surged since Putin’s Ukraine incursion, escalating geopolitical uncertainties and inflating oil prices. The collective impact of strong business survey data and healthy employment reports has tempered the deflation concerns of the past year, prompting a reassessment of interest rate expectations. Investors are now recalibrating for fewer anticipated rate cuts throughout the year, with a possibility of even factoring in a rate hike. The lineup of talks from Fed Presidents last week clarified the rift within the Fed, with one camp advocating a measured approach to rate cuts, while the minority remains circumspect about ongoing disinflation trends, opting for a cautious stance on rate adjustments. These diverging perspectives are further complicated by the upcoming election, adding another layer of complexity to the Fed’s decision-making process.

Market Indicators Update: Navigating the Path Ahead

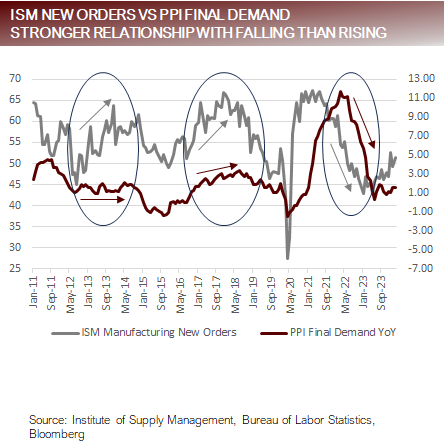

Unpacking the Interplay Between ISM Data and PPI

Manufacturing Sector Insights

-

-

Institute of Supply Management (ISM) Manufacturing sector unveiled their latest purchasing managers survey, indicating a rise in the New Orders component to a significant 51.4, signifying expansionary territory for the second time since mid-2022.

-

Moreover, Production surged while Customer Inventories dwindled, portraying an encouraging demand trend in Manufacturing indicative of an expansion phase.

-

Service Sector Observations

-

-

The Services segment, while not as robust as Manufacturing, experienced a minor dip in New Orders to 54.4 but remained well within expansion territory.

-

Similar to Manufacturing, Production saw an uptick with Inventories depleting, underscoring a strong demand narrative for the Services sector.

-

Employment Data and Federal Reserve Projection

Deciphering Labor Market Trends

- Employment data for the week continuously influenced the Federal Reserve’s perspective on labor supply dynamics.

Market Speculation on Interest Rates

10-Year Treasury Yields and Market Sentiment

- With the 10-year Treasury yield nearing concerning levels and the prospect of a rise in rates, the markets are on edge regarding the potential course of action.

2024 Presidential Election Update

Focus on Sector Rotation and Market Trends

Unwinding of Extreme Market Trends

Unveiling the Dynamics of Economic Indicators in the Market

Understanding the Role of Manufacturing in Economic Predictions

While the fervor in Manufacturing has slightly abated in recent times, it’s vital to remember that despite historically being perceived as a “leading indicator” of the economy, Manufacturing only constitutes roughly 20% of all activity. Furthermore, it didn’t live up to its leading indicator status in 2023.

Exploring Interconnections

- PPI Final Demand shares an intriguingly asymmetric relationship with ISM Manufacturing New Orders. When New Orders experience a decline, similar to the 2021-2023 period, PPI typically follows suit. Yet, when New Orders are on the rise, as is the case today, the correlation isn’t as robust. For instance, while New Orders saw an uptick between 2016 and 2018, PPI also followed suit, unlike the mismatch between 2012 and 2014.

- This divergence is significant because an upswing in ISM survey data does not necessarily translate to higher PPI. Hence, assuming that the uptick in manufacturing activity will result in inflation might be misleading.

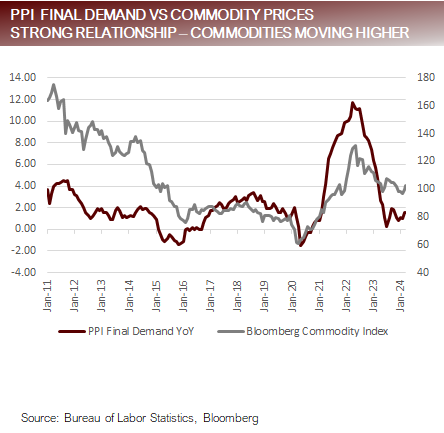

Observing Market Movements: ISM Manufacturing vs. Commodities

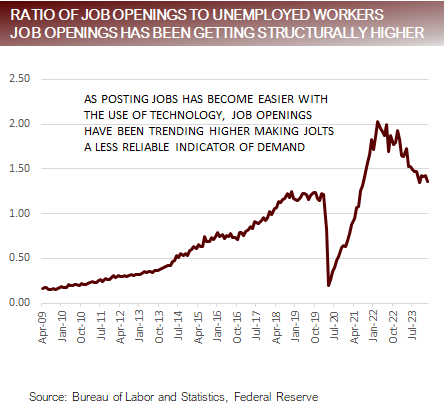

Insights from the Employment Landscape and its Impact on the Labor Supply Narrative

-

Significant employment reports from the past week revealed:

- Job Openings underwent a slight downward revision last month and maintained steadiness in the current period at 8756k. This leaves the Job Openings to Unemployed Workers Ratio at 1.36, lower than the peak of 2.03 in March 2022 but notably higher than the pre-pandemic average of 0.92. This could potentially mirror the relative ease of posting job opportunities amidst heightened job market activity.

The Thriving Pulse of the Market

A Blowout Performance on Nonfarm Payrolls

Nonfarm Payrolls stunned with a robust showing of 303k workers, surpassing the average economist forecast of 209k. The high forecast stood at 290k, with the actual figure of 303k delivering a blowout number. This unexpected surge in employment marks a significant step forward in the economic recovery post-recession.

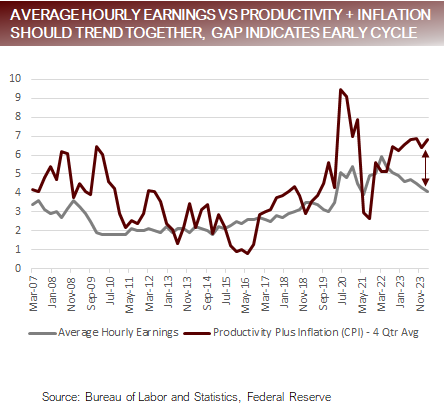

Steady Decline in Average Hourly Earnings Growth

Year-over-year Average Hourly Earnings growth dipped to 4.1%, continuing its downward trend and reaching the lowest annual growth rate since June of 2021. Although still above pre-pandemic levels, the current pace is below the desired threshold for wage growth sustainability, suggesting a cyclical phase post-recession.

Favorable Initial Jobless Claims and Labor Market Dynamics

Initial Jobless Claims fell to 221k, well below the level indicating steady employment state. The Unemployment Rate declined from 3.9% to 3.8%, while Average Weekly Hours inched up from 34.3 to 34.4, reflecting a positive momentum in the labor market.

Rising Labor Participation Rate Signals Promise

The Labor Participation Rate saw a rise from 62.5% to 62.7%, exceeding expectations. This increase in labor demand without inflationary wage pressures hints at the sustainable equilibrium advocated by the Fed. The rise in supply of labor aligns with this positive trend in labor dynamics.

Factors Driving Increased Labor Supply

- Larger than expected immigration

- The recent increase in Labor Participation from the 16-24 year old and 55+ cohorts

Analyzing ZipRecruiter’s Job Application Responses and Market Trends

Understanding the Job Application Landscape

ZipRecruiter has reported a notable 10% year-over-year increase in responses to job applications on their platform. This surge in activity signals a shifting landscape in the job market, where opportunities and candidate engagement are on the rise.

Accounting for Structural Factors in Job Openings

As we delve deeper into the job market dynamics, it becomes apparent that job opens may be nearing a state of normalization at current levels. This equilibrium reflects a balance between employer demand and job seeker interest, hinting at stability in the employment domain.

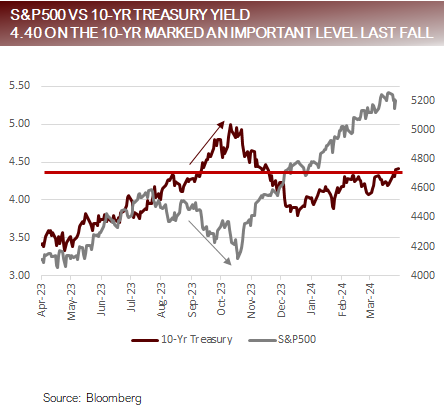

Delving into Treasury Movements

The 10-year Treasury yield has been flirting with the danger zone, posing a crucial question about the market’s next move — will it be driven by fear or acceptance of the evolving economic landscape?

- On Friday, the 10-year Treasury closed at 4.40. Back in September, the 10-year Treasury breached the 4.40 mark on 9/20/23, coinciding with an S&P500 value of 4402.20. This shift led to a subsequent decline in the S&P500 to an interim low of 4117.37, marking a decline of around -6.5%.

- The equities downturn was triggered by swift fluctuations in expectations of interest rate cuts by the Federal Reserve, stemming from a brief inflationary uptick. The market sentiments, as indicated by the WIRP function on Bloomberg, showcased a significant shift in expected rate cuts, causing a ripple effect in both bond and equity markets.

- The bond market tantrum in August/September saw the 10-year Treasury yield jump from 4.02 on 8/8/23 to 4.99 on 10/19/23, reflecting the volatility and sensitivity of the bond market to changing economic indicators.

- Fast forward to March 2024, the WIRP function on Bloomberg experienced fluctuations from a high of 6.71 on 1/12/24 to a low of 2.50. This rollercoaster ride paralleled the movements witnessed during the August/September market upheaval, emphasizing the market’s susceptibility to external factors and investor sentiments.

- With the 10-year Treasury breaching the 4.40 threshold once again, the key question remains: how will the market respond in the face of fluctuating economic conditions and investor expectations?

The Rollercoaster Ride of Financial Markets Amidst Inflationary Data Pandemonium

The Tug-of-War Between Inflationary Data and Market Expectations

Will we continue on this tumultuous journey spurred by the unexpected rise in inflation, or will we see a return to disinflationary patterns that could potentially lead to a reassessment of market rate-cut projections? Perhaps the markets will embrace the idea of increased rates, especially as the Fed subtly adjusts its long-term rate expectations. The dice are rolling, and the outcome is anyone’s guess.

As rate cut hopes fade, Treasury rates enter murky waters

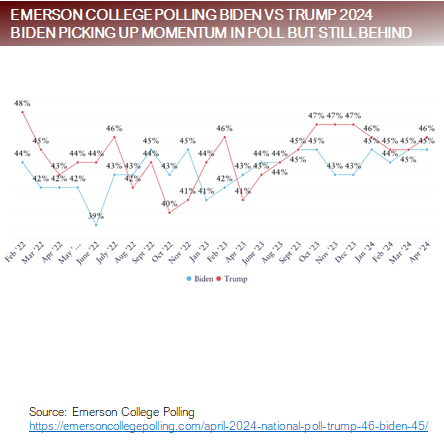

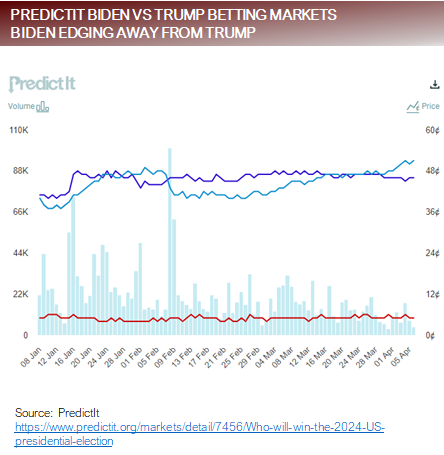

Insights into the 2024 Presidential Election Landscape

- The latest Real Clear Polling summary reveals Trump leading with a slight margin over Biden, but Emerson College’s recent commentary tips the scale slightly in Biden’s favor when including “very likely voters.” However, with undecided voters and Robert Kennedy supporters in the mix, the outcome remains uncertain. Betting markets, though, are leaning slightly towards Biden.

Convergence in Polling and Betting Markets Towards Biden’s Momentum

Unraveling Sector Rotation with a Heat Map

- The Focus Point Sector Rotation Model blends trend following and mean reversion strategies, utilizing seven factors to scrutinize sectoral price trends daily to gauge upward momentum.

- Last week saw the S&P500 experiencing a notable downturn with a decline in positive trends across various sectors.

- Sectors such as Materials, Energy, Financials, and Industrials have been the standout positive performers throughout the year.

- An overarching theme is emerging among the top sectors – a nexus of commodity inflation and a resurgence in manufacturing.

Bringing It All Together

- Amidst this whirlwind of market dynamics, the trends are shifting constantly, setting the stage for an unpredictable yet exhilarating ride for investors. Strap in for the rollercoaster ride of your financial life!

The Current Market Dynamics Shaping Investment Strategies

The Driving Forces in Today’s Markets

- A vibrant labor market that is supporting spending

- A revival in the manufacturing sector combined with supply concerns boosting commodities and their stock proxies

- Dissipating disinflationary trends of late 2023

- Questioning of the Fed’s resolve to cut rates in the face of stable employment and unstable price stability

The Fed has a dual mandate of full employment and price stability. The data, as it’s unfolding today, indicates the scale tips toward being more vigilant about price stability than concerned about full employment.

Today’s markets are setting up almost identically to the fall of 2023, when inflation jitters caused investors to re-gauge expectations for rate cuts in 2024, sending Treasury yields higher and the S&P500 lower. At the time, we continually used the metaphor that the equity markets were following the bond markets around like a star-struck lover; every time rates spiked higher, the equity markets would follow lower.

What’s may be different this time is that markets may be following the Feds’ lead and are quietly coming to consider baseline higher rates a possibility. It’s too early to tell if this will be the change that keeps the equity rally alive this round.

With the 10-year tittering on a ledge at 440, CPI on Wednesday, PPI on Thursday, and the banks, including JPMorgan, Citi, Wells Fargo, and State Street, reporting on Friday, the markets will get a lot of information on inflation and trajectory of earnings in Q1 this week and likely begin to shift the narrative one way or the other.

For more news, information, and analysis, visit the Innovative ETFs Channel.

Uncovering Intellectual Property Rights: Focus on Legal Protections

Important Risk Information

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI: A Closer Look

For more information, please visit www.focuspointlmi.com or contact us at [email protected] Copyright 2024, Focus Point LMI LLC. All rights reserved.

Protecting Copyrights and Intellectual Property

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced, or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including, but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights

Consequences of Unauthorized Use

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC Inc. will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber,

The Wild West of Financial Data: Proceed with Caution

Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses including lost income or lost profit and opportunity costs in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on asinvestment advice

This communication reflects our analysts’ current opinions and may be updated as views or information change.

Challenges and Disclaimers in Financial Markets

Investing Caution

Past outcomes serve as a weak crystal ball into the ever-fluctuating realm of future performance. Investment indicators are analogous to a capricious weather forecast, amorphous and subject to change without notice. Business landscapes shift, market conditions evolve, regulations mutate, all elements conspiring in a monetary ballet that can render historical hues irrelevant.

Artifacts masquerading as investment aids – be it a schematic, equation, or algorithm – carry a veil of treachery. The patterns that once heralded prosperity might implode into obscurity, mimicking a magician’s trick gone awry. Through market players who wield these tools, a ripple in the market may spawn, transforming the very essence of their efficacy.

Focus Point LMI LLC, ever the cautious guardian, asserts that no singular source of guidance – no chart, model, or any instrument of prediction – should stand as the sole compass for investment voyages. The sway of fortunes, long or short, on the securities under discussion remains an enigma, subject to abrupt whims of purchase and sale.

Neither Focus Point LMI LLC nor its emissaries proffer investment gospel, tax revelations, or legal sagacity to the populace. A tailored approach should precede any financial leap, experts summoned to navigate the rocky expanses of investment morass. The publications birthed by Focus Point LMI LLC embody a reservoir of data, perception, and analysis; a sherpa to the investment discerners, albeit sans a guarantee, a lone raft drifting in a river of uncertainties.

Void of Assurances

Focus Point LMI LLC thunders with disclaimers, an unassailable bulwark against the slings and arrows of outraged investors. Any and all warranties, veiled within the shadows of legalese – of merchantability, suitability, or fitness for a particular mission – fade away, leaving the investor unguarded against the caprices of the market storm.

Associates of Focus Point LMI LLC, be they kin or comrade, and even third-party soothsayers of data, swear by a code of immunity against financial squalls caused by reliance on their publications. They deflect liability with steely resolve, shielding against a deluge of losses, direct or indirect, meted out to any soul who dared to clutch their publications for solace.

Financial damages, akin to the toll of a tumultuous voyage, hang like an albatross around the neck of hapless investors who dared tread upon advice contained within Focus Point LMI LLC’s scrolls. Lost income, forsaken profits, and the intangible specter of opportunity vanishing into the ether – all sanctified losses in the grand theatre of investing.

Read more on ETFTrends.com.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.