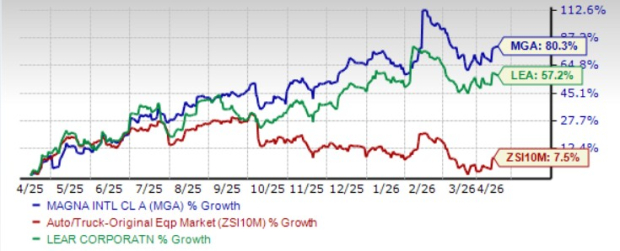

Magna International (MGA) and Lear Corporation (LEA) are competing in the evolving automotive sector, focusing on advanced vehicle technologies and increasing vehicle content. Over the past year, Magna has outperformed Lear, driven by a diversified portfolio, strategic partnerships, and margin improvements. As of 2025, Magna’s adjusted EBIT margin is projected to reach between 6% and 6.6%, with over $5.1 billion in liquidity, including $1.6 billion in cash.

In contrast, Lear is enhancing its core seating business through acquisitions and new program wins, securing over $1.4 billion in E-Systems awards in 2025. The company anticipates net new business of approximately $600 million in 2026 and $725 million in 2027, with free cash flow conversion projected to exceed 80%. However, despite a stable growth outlook, Lear’s narrower focus limits its growth potential compared to Magna.

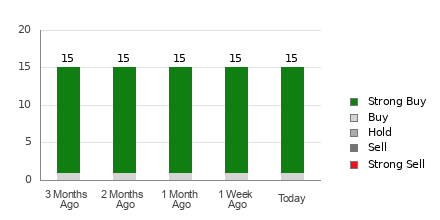

Overall, while both companies remain strong investments—Magna holds a Zacks Rank #1 (Strong Buy) versus Lear’s Zacks Rank #2 (Buy)—Magna’s comprehensive approach to industry trends and financial health gives it an edge in navigating future challenges.