Major U.S. Indices Decline Amid Trade Policy Concerns

The S&P 500 Index ($SPX) (SPY) has fallen by -3.58%, the Dow Jones Industrial Average ($DOWI) (DIA) is down -3.24%, and the Nasdaq 100 Index ($IUXX) (QQQ) shows a -3.90% decline. Additionally, June E-mini S&P futures (ESM25) are down -3.66%, while June E-mini Nasdaq futures (NQM25) have decreased by -3.94%.

Stock indexes are taking a sharp downturn today, with the S&P 500 and Nasdaq 100 reaching 6-1/2 month lows, and the Dow sliding to a 3-week low. These declines stem from mounting worries that President Trump’s trade policies could lead the economy closer to recession. On Wednesday, President Trump announced reciprocal tariffs that exceeded market expectations, causing significant sell-offs in both stocks and the dollar, and fostering a risk-averse atmosphere across asset markets. This downturn has driven a flight to safety into government bonds, leading European government bond yields to hit 4-week lows and the 10-year T-note yield to fall to a 5-1/2 month low.

The Barchart Brief: Your FREE insider update on the biggest news stories and investing trends, delivered midday.

In his announcement, President Trump indicated that the U.S. would implement at least a 10% tariff on all countries, alongside higher reciprocal tariffs targeting approximately 60 nations. These new tariffs will take effect on April 5, with elevated rates beginning on April 9. Treasury Secretary Bessent noted that negotiations are off the table. Certain sectors, such as steel and automobiles, will not be affected by the new tariffs, while Canada and Mexico will remain subject to the previously imposed 25% tariffs. Conversely, China faces a reciprocal tariff of 34%, while the EU will incur a 20% reciprocal tariff, raising total tariffs on the EU to 39%. Japan is set to face a 24% reciprocal tariff, increasing total tariffs on Japanese goods to 46%.

In recent labor market news, weekly initial unemployment claims unexpectedly dropped by 6,000 to a 7-week low of 219,000, indicating a stronger labor market than the projected rise to 225,000. However, continuing claims rose by 56,000 to a 3-1/3 year high of 1.903 million, surpassing expectations of 1.870 million and highlighting the challenges facing those attempting to reenter the workforce.

Additionally, the U.S. trade deficit for February narrowed to -$122.7 billion from -$130.7 billion in January, slightly better than the anticipated -$123.5 billion.

In the past month, stocks have endured pressure from concerns that U.S. tariffs may weaken economic growth and corporate earnings. On March 4, Trump initiated 25% tariffs on Canadian and Mexican goods and doubled the tariff on Chinese goods from 10% to 20%. Recently, Trump signed a proclamation to implement a 25% tariff on U.S. auto imports, effective today, which first targets vehicles assembled outside the US and will include automobile parts by May 3. Trump stated that these tariffs are “permanent” and that he is not seeking any negotiations.

This week, market participants are closely monitoring reactions to President Trump’s tariff announcements. Thursday’s March ISM services index is expected to fall by -0.5 to 53.0, while Friday’s nonfarm payrolls for March are projected to increase by +138,000, with the unemployment rate expected to remain steady at 4.1%. March average hourly earnings are anticipated to rise by +0.3% month-over-month and +4.0% year-over-year, maintaining the figures from February. On Friday, Federal Reserve Chair Powell will address the Society for Advancing Business Editing and Writing Conference on the economic outlook.

Currently, markets are pricing in a 29% chance of a -25 basis point rate cut following the FOMC meeting on May 6-7.

Overseas markets are also experiencing declines. The Euro Stoxx 50 has dropped to a 2-month low, down -3.14%. China’s Shanghai Composite Index closed down -0.24%. Meanwhile, Japan’s Nikkei 225 fell to a 7-3/4 month low, ending down -2.77%.

Interest Rates

Today, June 10-year T-notes (ZNM25) increased by +1-6/32 points, with the 10-year T-note yield decreasing by -10.0 basis points to 4.030%. June T-notes rose to a 5-3/4 month high, while the 10-year T-note yield fell to a 5-1/2 month low of 4.014%. The rally in T-notes is driven by fears that Trump’s tariffs will push the economy into recession, suggesting that the Fed may need to continue cutting interest rates. The global equity market selloff today has heightened demand for safe-haven government debt. Furthermore, today’s -6% decrease in crude oil prices, which hit a 2-week low, has restrained inflation expectations, benefiting T-notes.

European bond yields have also seen declines. The 10-year German bund yield fell to a 4-week low of 2.625%, down -8.5 basis points to 2.636%. Similarly, the 10-year UK gilt yield dropped to a 4-week low of 4.527%, down -10.8 basis points to 4.532%.

In other headlines, the Eurozone March S&P composite PMI was revised upward by +0.5 to a 7-month high of 50.9, up from the previously reported figure of 50.4.

The Eurozone’s February PPI rose by +3.0% year-over-year, aligning with expectations and marking the fastest increase in nearly two years.

Minutes from the ECB’s March 6 meeting indicated that policymakers are considering both a rate cut and a pause for their April meeting, depending on future data. Currently, swaps suggest an 85% probability for a -25 basis point rate cut at the ECB’s meeting on April 17.

US Stock Movers

The notable decline in the “Magnificent Seven” stocks is contributing to the overall market downturn. Apple (AAPL) has fallen over -8%, reflecting its significant exposure to tariff risks. Other tech giants, such as Amazon.com (AMZN) and Meta Platforms (META), are down more than -6%, while Nvidia (NVDA) and Tesla (TSLA) have decreased over -5%. Alphabet (GOOGL) is down more than -3% and Microsoft (MSFT) has dropped more than -2%.

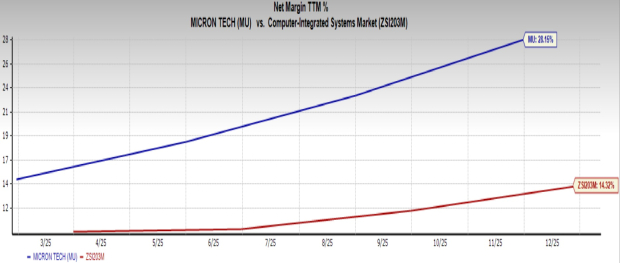

Chip manufacturers are also experiencing significant declines. Marvell Technology (MRVL), Micron Technology (MU), and Microchip Technology (MCHP) are each down more than -7%. Other companies like Broadcom (AVGO) and Lam Research (LRCX) are down more than -6%, and NXP Semiconductors NV (NXPI), ON Semiconductor (ON), Qualcomm (QCOM), KLA Corp (KLAC), and Applied Materials (AMAT) are down more than -5%.

Consumer stocks, primarily retailers and apparel makers sourcing goods from Asia, are suffering losses as well. Deckers Outdoors (DECK) is down over -14% to lead S&P 500 losers. Nike (NKE) has dropped more than -10%, leading the Dow Jones declines. Lululemon Athletica (LULU) is also down more than -10%, topping Nasdaq 100 losers. Skechers (SKX), Dollar Tree (DLTR), Target (TGT), and Walmart (WMT) are down by -16%, -10%, -8%, and more than -1% respectively.

Travel and leisure stocks are also tumbling due to concerns about rising prices from tariffs and potential cuts in discretionary spending. Norwegian Cruise Line Holdings (NCLH), Caesars Entertainment (CZR), and United Airlines Holdings (UAL) are down more than -10%. Additionally, Carnival (CCL) and Royal Caribbean Cruises Ltd (RCL) are both down more than -9%.

RH (RH) suffered a dramatic decline of more than -40% following the release of its Q4 revenue, which was reported at $812.4 million, falling short of the consensus estimate of $831.7 million; the company forecasts full-year revenue growth of only 10% to 13%, below the consensus of +14.6%.

Lyft (LYFT) is down more than -10% after Bank of America downgraded the company’s stock to underperform from buy, setting a price target of $10.50.

Amid a broader market downturn, defensive food and beverage makers are seeing gains. Mondelez International (MDLZ) is up more than +3%, and Coca-Cola (KO) has risen over +2%, leading gainers in the Dow. Other companies, including General Mills (GIS), Kraft Heinz (KHC), and PepsiCo (PEP), are also up more than +2%. Furthermore, Tyson Foods (TSN) and Conagra Brands (CAG) are each up more than +1%.

Lamb Weston Holdings (LW) reported a strong Q3, achieving an adjusted EPS of $1.10, exceeding the consensus estimate of 87 cents. The company forecasts full-year adjusted EPS between $3.05 and $3.20, with the midpoint above the consensus of $3.08, leading to a gain of more than +9% in the S&P 500.

Acuity Inc (AYI), Conagra Brands Inc (CAG), Lamb Weston Holdings Inc (LW), and MSC Industrial Direct Co Inc (MSM).

On the date of publication,

Rich Asplund

did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information, please view the Barchart Disclosure Policy

here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.