Markets React to Trade Talks Amid Tariff Concerns

The S&P 500 Index ($SPX) (SPY) has increased by +0.29%, while the Dow Jones Industrial Average ($DOWI) (DIA) is up by +0.70%. The Nasdaq 100 Index ($IUXX) (QQQ) has gained +0.39%. Also, June E-mini S&P futures (ESM25) are up +0.26%, and June E-mini Nasdaq futures (NQM25) rose by +0.38%.

Stock indexes have retreated from earlier significant gains, showing a cautious upward movement as midday approaches. This comes after steep losses in recent days, which saw the S&P 500 drop nearly 15% from last Wednesday’s close. Optimism surrounding a potential tariff agreement with Japan emerged after a discussion between President Trump and Prime Minister Ishiba on Monday, igniting hopes that a trade deal might reduce the impending 24% import levy set to take effect on Wednesday.

Today’s gains were further supported by President Trump’s remarks about positive talks with South Korea regarding a potential trade deal. Treasury Secretary Bessent mentioned that “very large countries with large trade deficits” will likely seek to establish trade agreements with the US soon.

Ongoing Tariff Tensions

Despite these positive developments, tariff-related anxieties persist. President Trump dismissed an EU proposal aiming to eliminate tariffs on all bilateral trade in industrial goods with the US, indicating that the 20% tariff on EU imports will be activated on Wednesday. Additionally, a spokesperson for China warned that the country would respond aggressively to Trump’s announcement of potential 50% tariffs on all Chinese goods, stating, “The US threat to escalate tariffs on China is a mistake on top of a mistake…if the US insists on its own way, China will fight to the end.”

Chicago Fed President Goolsbee noted that some business leaders voiced concerns that tariffs could revert the economy to the turbulence seen in 2021 and 2022 when inflation surged.

Market Reaction to Tariff Announcement

On Monday, global equity markets faced significant declines amid fears that escalating trade disputes could trigger a recession. Market turmoil escalated last Wednesday after Trump announced reciprocal tariffs that exceeded expectations. Sentiment worsened further on Friday when China retaliated by imposing a 34% tariff on all US imports set to begin on April 10. During this tense environment, Trump reiterated his stance, stating, “We’re not looking at a tariff pause.” He emphasized that if China does not eliminate its 34% tariff on US goods by Tuesday, the US will implement additional tariffs of 50% effective April 9.

On the previous Wednesday, Trump indicated plans for a minimum 10% tariff on nearly all countries, with higher rates for around 60 nations. These tariffs were enforced on Saturday, with the elevated rates scheduled for April 9. While specific sectors, including steel and automobiles, are exempt from the new tariffs, Canada and Mexico are also excluded but will face previously announced 25% tariffs. Tariffs on China have risen to a total of 67%, while the EU now faces a total tariff of 39% and Japan 46%.

Economic Outlook and Upcoming Reports

Concerns regarding the impact of US tariffs on economic growth and corporate earnings have weighed heavily on stocks over the past month. On March 4, Trump set 25% tariffs on Canadian and Mexican goods and increased tariffs on Chinese imports to 20%. Just last Wednesday, he announced the implementation of a 25% tariff on US auto imports starting Thursday, emphasizing that these tariffs would be “permanent” without exceptions.

Market predictions show a 28% chance for a -25 bp rate cut after the FOMC meeting scheduled for May 6-7, slightly lower than the previous week’s 30% estimate.

This week’s market focus will remain on US trade policies and potential retaliatory measures from other nations. The FOMC meeting minutes from March 18-19 will be released on Wednesday. Furthermore, the March CPI is anticipated to decrease to +2.6% year-over-year, down from 2.8% in February, while the CPI excluding food and energy is expected to dip to +3.0%. On Friday, the March final-demand PPI is projected to climb to +3.3%, and Michigan’s consumer sentiment index is forecasted to drop to 54.0 from March’s 57.0.

The first quarter earnings season will kick off Friday, led by reports from major US banks. Bloomberg Intelligence indicates a consensus for year-over-year earnings growth of +6.7% for the S&P 500, a decline from earlier predictions of +11.1% in early November. Full-year 2025 corporate profits for the S&P 500 are estimated to rise by +9.4%, down from a previously anticipated +12.5% in January.

International Market Movements

Today, international stock markets have seen positive movement. The Euro Stoxx 50 is up by +3.55%, the Shanghai Composite Index in China closed with a gain of +1.58%, while Japan’s Nikkei Stock 225 surged by +6.03%.

Interest Rates Overview

For the June 10-year T-notes (ZNM25), a drop of -13 ticks has been observed. The yield for the 10-year T-note has risen by +2.5 bps to 4.208%. As global equity markets recover, safe-haven demand for government debt has diminished, leading to a moderate decline in June T-notes. Comments from Chicago Fed President Goolsbee have added pressure on T-notes amid fears of a repeat inflation surge due to tariffs. Additionally, upcoming Treasury auctions, starting with today’s $58 billion auction of 3-year T-notes, are pressuring supply.

European bond yields also climbed today, with the 10-year German bund yield up by +5.7 bps to 2.670% and the 10-year UK gilt yield increased by +2.8 bps to 4.643%.

ECB Governing Council member Simkus stated, “I still think the ECB should cut rates this month, and then, with a lot more information in June, we can reassess whether to wait and see or cut again.” Current swaps markets reflect a 90% chance of a -25 bp rate cut by the ECB at the April 17 policy meeting.

Major Stock Movers Lead Market Gains Amid Upgrades and Positive News

Stock Movers

The Magnificent Seven stocks are seeing substantial gains today, positively impacting the broader market. Nvidia (NVDA) has risen by over +6%, while Tesla (TSLA) is up more than +4%. Additionally, Meta Platforms (META) and Microsoft (MSFT) are gaining more than +3%, and Apple (AAPL), Amazon.com (AMZN), and Alphabet (GOOGL) have each seen increases of more than +2%.

Health Insurance Stocks Surge

Health insurance stocks are experiencing a significant uptick following the Centers for Medicare & Medicaid Services’ announcement of a 5.06% average increase in payments to Medicare Advantage plans from 2025 to 2026. This increase is notably higher than previous projections. As a result, Humana (HUM) has surged over +11%, leading the S&P 500 gainers, while Alignment Healthcare (ALHC) has also risen by more than +11%. Other notable gainers include CVS Health Corp (CVS), up more than +9%, and UnitedHealth Group (UNH), which has increased over +7%. Universal Health Services (UHS) is up more than +5%, and Centene (CNC) has gained more than +3%.

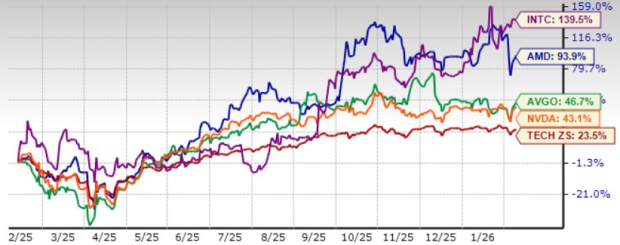

Chip Manufacturers Strengthen Market Performance

Chip manufacturers are contributing positively to the market today. ARM Holdings Plc (ARM) shows a modest rise of over +7%, while Advanced Micro Devices (AMD), KLA Corp (KLAC), and Applied Materials (AMAT) have all jumped more than +5%. Additionally, Lam Research (LRCX) and Micron Technology (MU) are up by more than +4%, with Intel (INTC), Analog Devices (ADI), and Qualcomm (QCOM) increasing more than +2%.

Highlighted Stocks on the Move

Marvell Technology (MRVL) has risen over +8% following its decision to sell its automotive networking business to Infineon for $2.5 billion. Broadcom (AVGO) is also up more than +8% after announcing a new stock buyback program worth up to $10 billion.

Eli Lilly & Co (LLY) has increased more than +3% after Goldman Sachs upgraded the stock from neutral to buy, setting a price target of $888. Meanwhile, Teradata Corp (TDC) gained over +4% following an upgrade by Morgan Stanley from equal weight to overweight, with a target price of $26. Range Resources (RRC) saw its stock rise more than +2% after Roth Capital Partners provided an upgrade to buy, increasing its price target to $42. Walgreens Boots Alliance (WBA) is also up more than +1%, reporting Q2 sales of $38.60 billion, exceeding the consensus estimate of $38.03 billion.

On the downside, RPM International (RPM) is down more than -4% after its Q3 net sales of $1.48 billion fell short of the consensus forecast of $1.51 billion.

Stock Declines and Market Sentiment

PDD Holdings (PDD) leads the Nasdaq 100 losers, dropping more than -1% after President Trump threatened to raise tariffs on Chinese goods by 50% unless China withdraws its 34% tariff on U.S. products. Alcoa (AA) is down more than -2% following a downgrade by Bank of America Global Research to underperform from neutral, with a price target of $26. Additionally, Virtu Financial (VIRT) has seen a decline of more than -1% after being downgraded by Morgan Stanley from equal weight to underweight, with a price target of $26.

The upcoming earnings reports include companies such as Aehr Test Systems (AEHR), Cal-Maine Foods Inc (CALM), Dakota Gold Corp (DC), Kura Sushi USA Inc (KRUS), Mama’s Creations Inc (MAMA), PACS Group Inc (PACS), RPM International Inc (RPM), Walgreens Boots Alliance Inc (WBA), and WD-40 Co (WDFC).

On the date of publication,

Rich Asplund

did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.