Masimo MASI has set sail on a new course with the announcement of its intention to segregate its consumer business from the professional healthcare and telehealth products. The company’s captain, Joe Kiani, will steer both ships following the separation greenlit by the board of directors.

The impending separation will encompass a treasure trove of non-healthcare assets including premium home sound integration tech, high-performance in-vehicle audio systems, and an elite lineup catering to professional sound studios and audiophiles. Furthermore, the voyage will also ferry the Stork baby monitor and the Freedom smartwatch and band away from Masimo’s healthcare portfolio.

The strategic separation is currently navigating through the fog of due diligence and regulatory waters. However, the compass is set on maintaining financial course for the first quarter of the fiscal year 2024, hinting that landfall for the spin-off may occur in the latter part of 2024, or perhaps even further down the horizon.

The Voyage Strategy

Masimo’s decision to navigate towards the spin-off of its consumer business is a plotted course towards calmer seas in its healthcare territory. By unloading the consumer cargo, Masimo aims to bolster the profitability of its healthcare arm, centered around noninvasive monitoring products for hospitalized patients. The planned separation is intended to offer a clearer focus on the healthcare segment, potentially leading to higher margins and an accelerated growth in shareholder treasure chests.

The Market Winds: Historical Footprints and Future Projections

The winds of change blew strong against Masimo’s non-healthcare business in 2023, with dwindling demand for consumer audio products in a storm of decreased discretionary spending. Revenue from non-healthcare sources saw an 11% growth for the full fiscal year, mainly riding on favorable foreign currency tides. However, when measured in constant currency, sales faced an 18% dip.

The forecasts for 2024 also hint at a stormy outlook for non-healthcare sales, with the healthcare segment setting a different course with sales expected to surge by 5.5-8.6%. The separation is anticipated to clear a smoother path for Masimo’s gross margins moving forward, with the healthcare segment showcasing a robust 62% adjusted gross margin compared to the 33%-35% range expected for the non-healthcare segment in 2024.

Is the Masimo voyage one to board? The market seems to think so as the company has already witnessed a 4.2% uptick in its shares since the announcement of the spin-off plans last Friday. However, the ultimate treasure from this separation will heavily depend on the value of the deal struck.

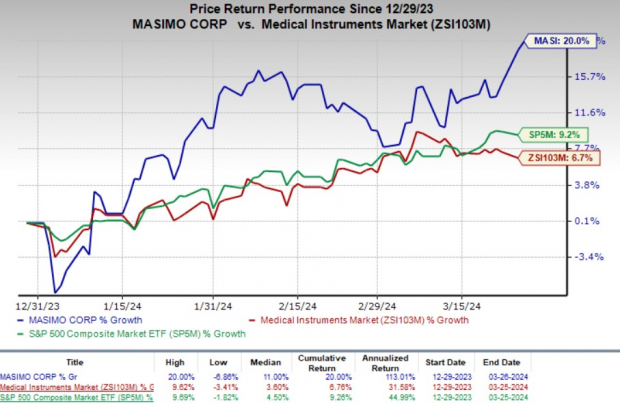

In the expedition of stock performance, Masimo has hoisted its shares 20% higher since the start of the year, setting sail ahead of the industry at 6.7% and leaving the S&P 500 Index a few knots away at 9.2%.

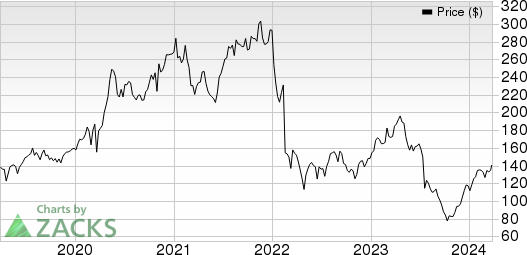

Masimo Corporation price | Masimo Corporation Quote

Image Source: Zacks Investment Research

Further Market Explorations

In the expansive seas of the market, Masimo anchors its rank at #2 (Buy), enticing investors with its alluring voyage towards the consumer business spin-off. Other notable ships navigating these waters include Cardinal Health CAH, Stryker SYK, and DaVita DVA, each with their sails set differently. Cardinal Health and Stryker proudly bear a Zacks Rank #2 insignia, whereas DaVita unfurls the Zacks Rank #1 (Strong Buy) flag.

Cardinal Health’s journey has seen a 55.8% surge in the past year with earnings estimates gaining wind in their sails for fiscal years 2024 and 2025. Meanwhile, Stryker’s voyage has been marked by a 26.2% rise in the past year, a testament to the company’s consistent beating of earnings estimates. DaVita’s odyssey charts a 74.7% journey through the market’s waters while posting impressive earnings surprises along the way, averaging at 35.57%.

Venture Deeper into the Markets

Stryker’s plans for stagnant earnings per share in 2024 are keeping investors guessing, while DaVita has seen a revision in its earnings forecast for the same year. Both companies have ridden the wavering market waves, with Stryker inching 5.2% higher than the industry, and DaVita shining bright with a 22% industry-wide rise.

Whether this separation spin-off spells fair winds for Masimo or potential stormy seas, one thing remains certain – in the unpredictable world of market voyages, strategic decisions can often make the difference between finding hidden treasure and getting lost at sea.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.2% per year. So be sure to give these hand-picked 7 your immediate attention.

Stryker Corporation (SYK) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report

Cardinal Health, Inc. (CAH) : Free Stock Analysis Report

Masimo Corporation (MASI) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.