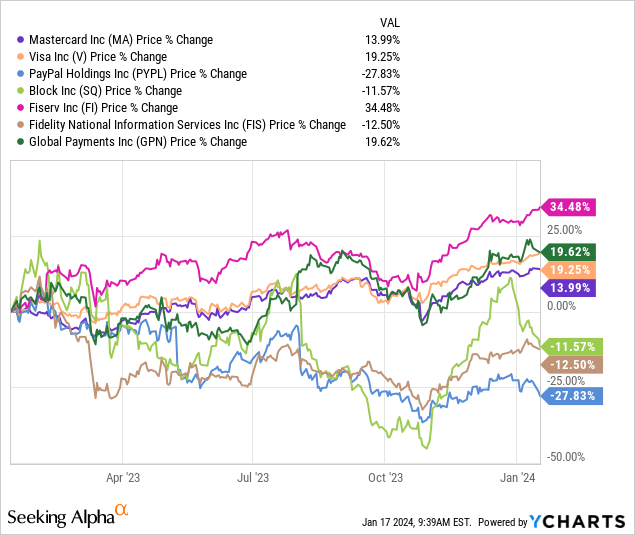

It’s no surprise that Mastercard Incorporated (NYSE:MA) stood out as one of the top performers in the electronic payments space over the past year, alongside the likes of Visa (NYSE:V) and the unexpected winner – Fiserv (NYSE:FI).

About a year ago, I also turned bullish on Mastercard, even though a recession in 2023 was highly likely – a scenario that failed to materialize. The odds of a major economic slowdown are even higher in 2024, evidenced by the continued deterioration of leading economic indicators and the steepening of the inverted yield curve.

Despite the challenging environment, my optimism for Mastercard’s business model over the long run remains unwavering. There is no apparent reason for the stock to underperform its broader peer group.

However, in the immediate future, 2024 is likely to be far less supportive for Mastercard’s operations. On top of that, the stock is now pricing in MA’s record-high profitability to be sustained, which is not an unreasonable scenario, but it also limits potential upside.

Transition from Success to Difficulty

Following a relatively flat period in 2021 and 2022, the stock experienced a robust 2023 due to several macroeconomic tailwinds and renewed business momentum.

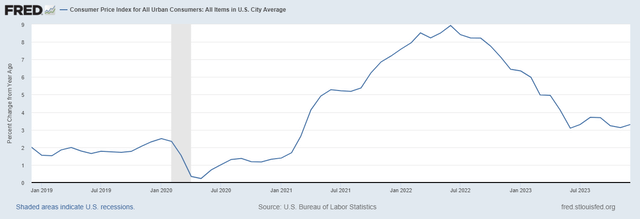

Elevated inflation during 2022 was a significant driver, propelling the nominal value of retail sales to record highs.

Subsequently, Mastercard’s gross dollar volume soared in 2023, with volumes outside of the U.S. increasing by 13% and high-margin cross-border volumes improving by 21%.

Gross Dollar Volume, or GDV, increased by 11% year-over-year on a local currency basis. In the U.S., GDV increased by 5%, with credit growth of 7% and debit growth of 4%. Outside of the U.S., volume increased 13%, with credit growth of 13% and debit growth of 14%. Sequentially, the debit growth rate was primarily impacted by the lapping of the NatWest portfolio migration in the U.K.

Overall, cross-border volume increased 21% globally for the quarter on a local currency basis, reflecting continued strong growth in both travel and non-travel-related cross-border spending.

Source: Mastercard Q3 2023 Earnings Transcript (emphasis added).

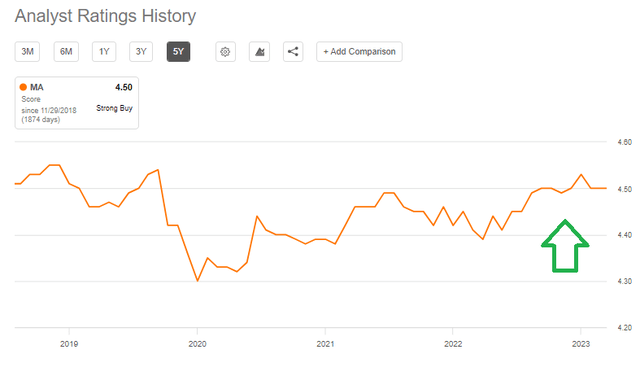

The stock has also witnessed notable upgrades from sell-side analysts over the past year, with the consensus rating for the company now at one of its highest levels in the last 5 years.

Though such rapid increases in the consensus view have valid reasons, they also pose significant short-term risks for the share price due to excessive optimism.

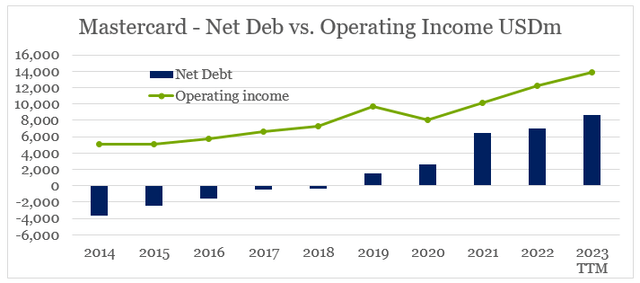

Additionally, Mastercard’s management has displayed more aggression than usual over the past few years in expanding the business through M&A activity. The company completed several major deals during 2020-2021, which significantly increased net debt to nearly $9bn, contrasting with the negative $350m in fiscal year 2018.

- Corporate Services business of Nets Denmark A/S (“Nets”) for €3.0 billion (approximately $3.6 billion as of the date of acquisition)

- 100% equity interest in Ekata, Inc. (“Ekata”) for cash consideration of $861 million

- Finicity Corporation (“Finicity”), an open-banking provider headquartered in Salt Lake City, Utah, for cash consideration of $809 million.

Although the sharp increase in net debt doesn’t pose a significant problem for Mastercard’s stable and highly profitable business model, the company is unlikely to sustain this aggressive M&A approach going forward.

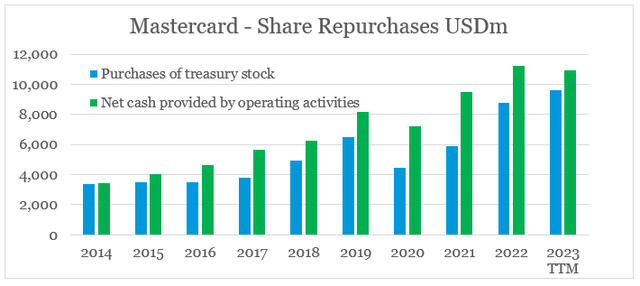

Following the completion of the aforementioned deals, Mastercard’s management has shifted its attention to share repurchases, which are on track to reach $10bn annually. Over time, the amount spent on share buybacks usually mirrors the company’s cash flow from operations, but it’s already showing signs of slowdown in 2023.

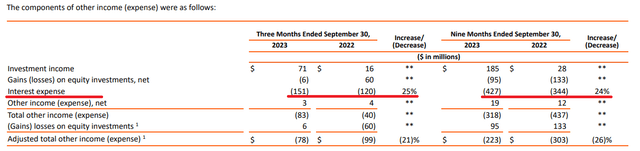

Furthermore, the recent increase in interest rates is likely to exert further pressure on Mastercard’s ability to grow inorganically and repurchase shares at the current rate. Interest expense grew nearly 25% for the first 9-month period of 2023 and is set to reach $600m for the full fiscal year.

Mastercard Balancing on Peak Margins

Margin Peaking Analysis

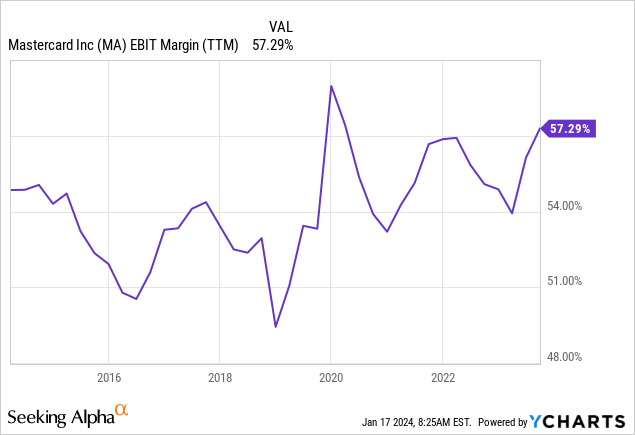

Mastercard’s top line and earnings growth have been thriving recently. Yet, the share price returns could face a new barrier – a peak in margins.

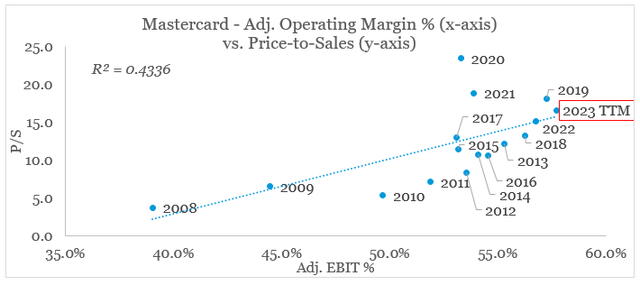

Since the pandemic, Mastercard’s operating margin has consistently exceeded historical levels and now peaks at a record high.

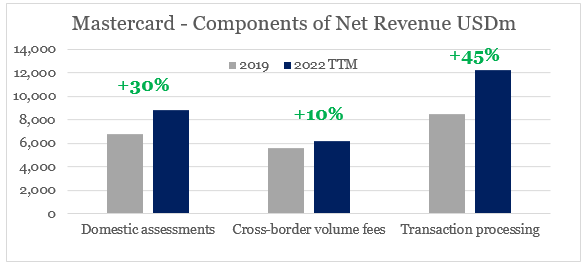

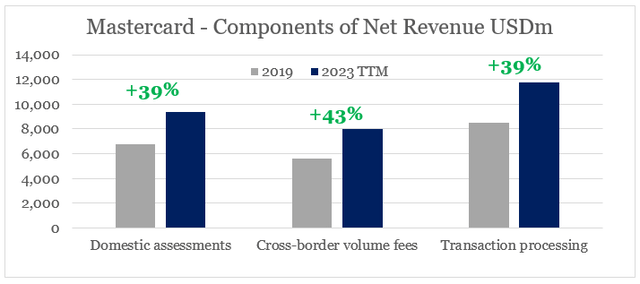

This surge has been mainly fueled by economies of scale as Mastercard significantly expanded in recent years. Notably, the company’s different segments amplified in size, with domestic assessments and transaction processing revenues climbing by 30% and 45% respectively.

As of the end of the third quarter of 2023, there has been a substantial increase in cross-border volume fees as well.

Conversely, Mastercard’s cross-border volumes display signs of weakness, given the intense recovery experienced last year.

Overall, cross-border volume increased 21% globally for the quarter on a local currency basis, reflecting continued strong growth in both travel and non-travel-related cross-border spending. While this is sequentially lower versus Q2, this is due to tougher comps as we lapped the cross-border travel recovery from last year.

Source: Mastercard Q3 2023 Earnings Transcript.

With operating margins at a record high, it’s no surprise that Mastercard’s stock now trades at one of its highest sales multiples since the company’s IPO. Over time, there has been a notably strong correlation between the two variables, and the current P/S ratio of nearly 17 aligns with the margins achieved over the past 12 months.

Hence, a further upward repricing in MA’s multiples seems highly unlikely unless the company manages to improve its margins beyond the already record-high levels. This is certainly a possible scenario in the short term, but improbable for anyone with longer investment horizons.

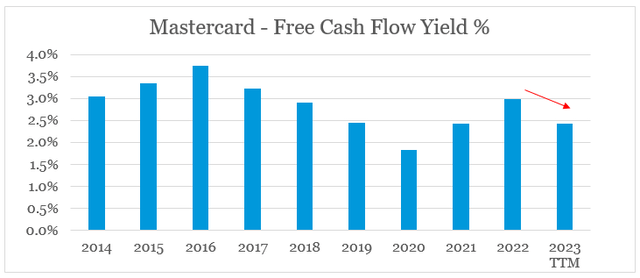

Over the past year, Mastercard’s free cash flow yield also noted a significant drop and now rests below 2.5%. In a higher rate environment, this poses risks for a company of its size.

The Verdict

While Mastercard Incorporated remains a top pick within the electronic payments space, the robust performance over the past year has resulted in limited upside for 2024. The highly supportive macroeconomic environment is likely to alter over the coming year. Shareholders should also be aware of specific capital allocation decisions and the optimistic business fundamentals currently being priced in.