W. R. Berkley Corporation Outperforms Industry with Solid Growth

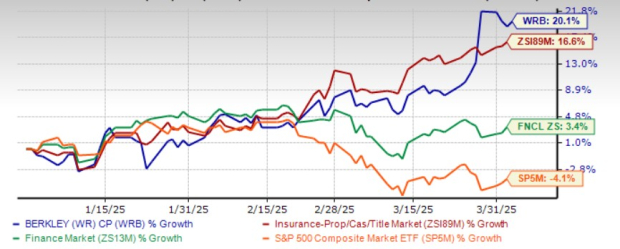

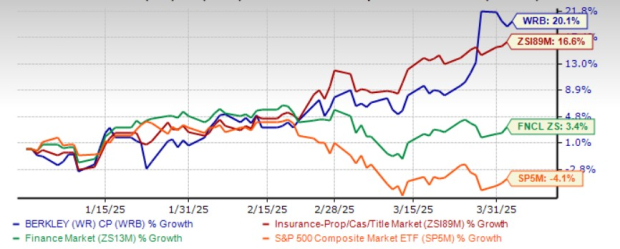

Shares of W. R. Berkley Corporation (WRB) have surged 29.1% year to date, outperforming its industry, the sector, and the Zacks S&P 500 composite during the same period.

Currently, W. R. Berkley shares are trading well above their 50-day moving average, which indicates a bullish trend in the market.

As one of the largest commercial lines property casualty insurance providers in the U.S., WRB has a market capitalization of $26.7 billion. Over the past three months, the average trading volume reached nearly 2 million shares.

WRB vs. Industry, Sector & S&P 500 Year to Date

Image Source: Zacks Investment Research

Valuation of WRB Stock

Currently, WRB shares are trading at a premium compared to the industry average, with a price-to-book value standing at 3.16X versus the industry average of 1.66X.

Image Source: Zacks Investment Research

Similarly, other insurers such as Arch Capital Group (ACGL), CNA Financial (CNA), and Cincinnati Financial (CINF) are also trading at a premium to industry averages.

Return on Capital and Operational Efficiency

The company’s return on equity for the trailing twelve months stands at 20.6%, significantly higher than the industry average of 8.3%, demonstrating WRB’s effective use of shareholder funds. The company aims for a long-term return of 15%.

Moreover, WRB’s return on invested capital (ROIC) has shown an upward trend over recent quarters, currently at 10%, well above the industry average of 6.4%. This growth reflects the company’s ability to effectively invest and generate income.

Growth Drivers for WRB Stock

W. R. Berkley is strategically positioned in areas where it holds a competitive advantage, which is likely to fuel further growth. The firm concentrates on commercial lines, including excess and surplus lines, admitted lines, and specialty personal lines.

WRB is poised for growth through new startup units within various business lines alongside its international business expansion, which provides diversification, market stability, and increasing retention rates. The company is expanding its reach into global markets, including the United Kingdom, Continental Europe, South America, Canada, Scandinavia, Asia, and Australia.

With over 60 consecutive quarters of favorable reserve development due to prudent underwriting, W. R. Berkley maintains a sound balance sheet characterized by strong cash flows and adequate liquidity.

Positive Analyst Sentiment Surrounding WRB

Recent updates indicate that the Zacks Consensus Estimate for WRB’s earnings for 2025 and 2026 has increased by 1 cent each over the past month, suggesting positive analyst sentiment.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for 2025 earnings is currently set at $4.34, reflecting a 4.8% increase, with revenues projected to rise by 6.7% to $14.4 billion. For 2026, earnings are estimated at $4.72, indicating an increase of 8.7% on anticipated revenues of $15.7 billion, which is a growth of 8.6%.

Additionally, the long-term earnings growth rate for WRB is anticipated to be 8.2%, outpacing the industry average of 7.6%.

Market Outlook for WRB Stock

Research involving 16 analysts suggests that the Zacks average price target for WRB is $66.56 per share, indicating a potential downside of 4.6% from its last closing price.

Investment Perspective on WRB Stock

W. R. Berkley is well-positioned for growth due to better pricing strategies, careful reserve management, diversification, and strong momentum in international markets. The company has consistently raised dividends since 2005, currently boasting a dividend yield of 0.5%, which is attractive compared to the industry average of 0.3%, making it appealing to yield-seeking investors. The stock also enjoys a VGM Score of A.

However, consideration of WRB’s leverage and times interest earned raises some caution. Increasing expenses have been impacting margins, making it prudent to adopt a cautious stance.

In light of its premium valuation, it would be advisable to take a wait-and-see approach for this Zacks Rank #3 (Hold) stock in the near future. For insights into other investment opportunities, you can explore the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Discover Top Stocks for Short-Term Gains

Recently released, analysts have handpicked 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They are considered “Most Likely for Early Price Pops.”

Since 1988, this comprehensive list has outperformed the market by more than 2X, achieving an average gain of +23.9% per year. Don’t miss out on these recommended stocks.

W.R. Berkley Corporation (WRB): Free Stock Analysis Report

Cincinnati Financial Corporation (CINF): Free Stock Analysis Report

CNA Financial Corporation (CNA): Free Stock Analysis Report

Arch Capital Group Ltd. (ACGL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.