Contributions by Sinai Partners in this article. To learn how to contribute to Seeking Alpha for profit and free access to SA Premium, click here.

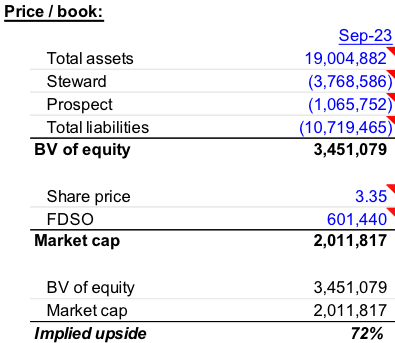

Medical Properties Trust (NYSE:MPW) puts forward senior unsecured bonds due in 2026 and 2027 as an enticing prospect. With visible credit ratings, shorter durations, and yields exceeding 10%, these bonds undoubtedly catch the eye of astute investors. Notably, MPW’s balance sheet for Q3 2023 underscores an $8.3 billion book value of equity against a market cap of approximately $2.0 billion, hinting at possible undervaluation. Even with the weight of negative news concerning Steward and Prospect, stripping out these weaknesses from the $19.0 billion total assets still maintains MPW’s equity at a lofty 70% premium above the current market cap. This reaffirms the notion that the equity is currently trading at rock-bottom prices.

For any wary investors, the 2026 and 2027 bonds appear as a safe haven. Their discounts, particularly in light of recent extensive attention, coupled with an equity cushion ranging between ~$2.0 billion to ~$3.5 billion, warrant a loan-to-value ratio of 76 – 84%. This essentially leaves the debt at par, a scenario skewed lower by the discounted bond prices and the hypothetical write-off of Steward and Prospect.

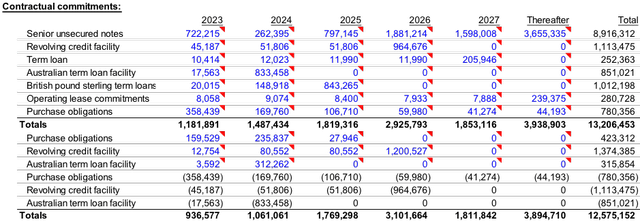

Underneath this facade, a deeper dive portrays a less optimistic picture. The Company has hefty contractual commitments on the horizon, primarily related to maturities on its existing debt. Detailed scrutiny of these figures delineates a harsh reality that investors cannot overlook.

Delving into AFFO (Adjusted Funds from Operations) and liquidity events unfolds a different narrative. In the past nine months, MPW reported AFFO of approximately $604 million. Extrapolating this number and excluding Steward and Prospect’s contribution indicates an annual AFFO of roughly $608 million. This paints an optimistic outlook amid upcoming liquidity events.

Liquidity measures are another reflection of the Company’s fiscal fortitude. Holding close to $1 billion in receivables on its balance sheet, MPW conservatively assumes a 75% discounted cash conversion in 2025. Management’s intent to target ~$2 billion in asset dispositions or secured debt raises brings clarity to the roadmap ahead.

Conclusively, the future seems bleak for the 2026 and 2027 bonds. As an astute investor, one has to bank on either Steward and Prospect overcoming their tribulations or the Company securing new debt in 2025/2026 to back the unsecured 2026s and 2027s. However, the offered yields on these bonds hardly justify the risk, challenging the underlying investment thesis. Cautious observation of developments is warranted, and careful investing is advised.