MercadoLibre (MELI) Shares Surge 47.4% This Year Amid Growth

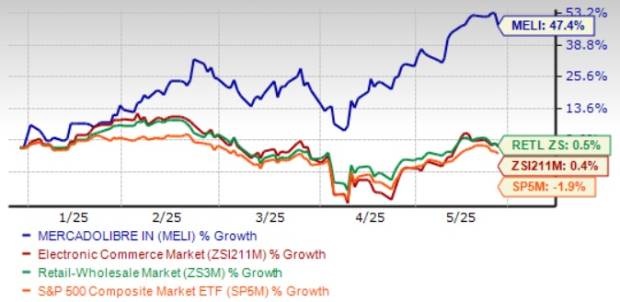

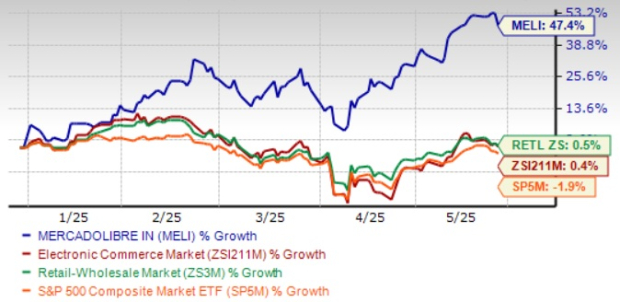

MercadoLibre (MELI) shares have increased by 47.4% year-to-date (YTD), significantly outperforming the Zacks Retail-Wholesale sector’s growth of 0.5% and the Zacks Internet-Commerce industry’s increase of 0.4%. The stock has also surpassed the S&P 500’s decline of 1.9% YTD.

Its strong performance is attributed to a dominant presence in Latin America and a diversified business model across e-commerce and fintech. MELI’s momentum gained traction from two consecutive strong earnings reports that exceeded expectations.

In Q1 2025, total revenues surged, propelled by e-commerce and fintech revenues growing by 32.3% and 43.3% year-over-year, respectively. The marketplace recorded a 25% increase in Unique Active Buyers, while fintech’s Monthly Active Users rose by 31%. However, despite these strong figures, investors should remain cautious due to emerging headwinds impacting the company. Let’s explore the factors influencing MELI’s performance.

MELI’s YTD Price Return Performance

Image Source: Zacks Investment Research

MELI Expands Its Advertising Inventory

MercadoLibre has broadened its advertising capabilities by launching the Mercado Play app on smart TVs across Latin America at the end of Q1 2025. The app is now downloadable on over 70 million smart TVs, offering more than 15,000 hours of free content. With under half the region’s population subscribed to paid streaming services, this presents a significant opportunity for user engagement.

This initiative aims to benefit consumers through free content, content studios through wider distribution, and Mercado Ads via increased ad inventory and reach.

MELI’s Earnings Estimate Revisions Show Upward Trend

The Zacks Consensus Estimate for second-quarter 2025 earnings is now at $11.70 per share, reflecting a 12.28% upward revision over the last 30 days. This indicates an 11.64% year-over-year growth.

For second-quarter 2025 revenues, the consensus estimate is $6.37 billion, suggesting a 25.52% year-over-year growth.

MercadoLibre has exceeded the Zacks Consensus Estimate in three of the last four quarters, with an average surprise of 22.59%.

MercadoLibre, Inc. Price and Consensus

MercadoLibre, Inc. price-consensus-chart | MercadoLibre, Inc. Quote

MELI Stock is Overvalued

MELI is currently trading at a premium relative to the broader Zacks Internet-Commerce industry. The forward 12-month Price/Sales ratio stands at approximately 4.32, compared to the industry’s 2, reflecting high growth expectations among investors.

The Value Score of D indicates that the current valuation of the stock is unattractive.

MELI’s P/S F12M Ratio Depicts Premium Valuation

Image Source: Zacks Investment Research

MELI Faces Credit Business Risks

In Q1 2025, MercadoLibre experienced a sharp decline in its credit portfolio profitability. The Net Interest Margin After Losses (NIMAL) dropped to 22.7% from 31.5% a year prior. The company attributed this to negative seasonality, but the year-over-year decline suggests deeper structural issues.

A growing dependence on credit cards—which now constitute 42% of the portfolio, up from 35%—has negatively affected margins. These products yield lower returns than consumer loans, impacting overall performance. Although Argentina’s share of the portfolio has doubled, it only partially offsets the deterioration in NIMAL.

MELI Faces Intense Competition in the E-Commerce Space

As global e-commerce expands, MercadoLibre faces increasing competition from well-funded international players targeting Latin America. Amazon is increasing its presence in the region, while Walmart, the largest brick-and-mortar retailer in Latin America, is leveraging its extensive stores for market share. Alibaba‘s AliExpress is also adding pressure by offering low-cost products to price-sensitive consumers.

Although MercadoLibre leads in Latin America’s digital commerce, competition from these global firms poses significant risks to its market position. Their advanced logistics, technology, and financial resources could threaten MELI’s user retention and pricing power, impacting long-term growth and profitability.

Investors Should Hold MELI Stock for Now

MercadoLibre remains a significant player in Latin American e-commerce and fintech. However, new challenges necessitate a cautious perspective. Heightening competition and pressure on credit margins pose substantial risks to its growth trajectory.

The recent drop in NIMAL and MELI’s premium valuation complicate the near-term investment outlook. While its expanding user base and diversified ecosystem are strengths, current profitability risks and competitive challenges suggest that investors may want to hold the stock until more clarity arises. MELI currently holds a Zacks Rank #3 (Hold).

7 Best Stocks for the Next 30 Days

Experts have identified seven elite stocks from a pool of 220 Zacks Rank #1 Strong Buys as “Most Likely for Early Price Pops.”

Historically, this selection has outperformed the market by more than 2X with an average gain of +23.0% per year since 1988.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.