Meta Platforms Anticipates Strong Q1 Growth Amid AI Investments

Meta Platforms (META) is scheduled to report its first-quarter 2025 results on April 30.

Revenue Expectations for Q1 2025

META forecasts total revenues between $39.5 billion and $41.8 billion for the first quarter of 2025. This projection signifies an 8-15% year-over-year growth or 11-18% growth at constant currency (cc).

The Zacks Consensus Estimate for first-quarter revenues is currently $41.22 billion, reflecting a 13.08% increase from the previous year’s figure.

Earnings Expectations

The consensus for earnings is set at $5.21 per share, representing a decline of 2.3% over the past month but indicating a growth of 10.62% compared to last year.

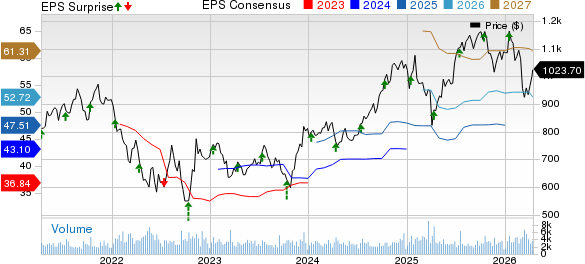

Meta Platforms, Inc. Price and EPS Surprise

Meta Platforms, Inc. price-eps-surprise | Meta Platforms, Inc. Quote

Meta has surpassed the Zacks Consensus Estimate for earnings in the previous four quarters, with an average surprise of 13.77%.

Impact of Advertising Revenues

Meta Platforms is bolstered by strong advertising revenue growth. The Zacks Consensus Estimate for first-quarter 2025 advertising revenues is currently $40.44 billion, showing a 13.5% increase year-over-year. Advertisers are expected to sustain spending due to META’s advancements in AI technology, despite some tariff-related uncertainties.

The company’s platforms—WhatsApp, Instagram, Messenger, and Facebook—reach over three billion users daily. This substantial reach, coupled with a 6% increase in ad impressions year-over-year as of Q4 2024, positions META as a key player in the digital advertising market alongside Alphabet (GOOGL) and Amazon (AMZN). These companies are projected to capture approximately 50% of the global ad spending by 2028.

Challenges in Operating Margins

While META is leveraging AI to enhance user engagement, rising costs associated with advanced model development may impact profit margins. The Reality Labs segment continues to incur losses, with a consensus estimate for its loss at $4.70 billion, which is larger than the prior year’s loss of $3.85 billion.

Market Performance Overview

Year-to-date, META shares have dropped 6.6%, performing better than the Zacks Computer & Technology sector, which is down 11%. However, it lags behind the Zacks Internet Software Industry’s decline of 5.9%.

Compared to its “Magnificent 7” peers, META has also outperformed companies like Apple, Alphabet, Amazon, Microsoft, NVIDIA (NVDA), and Tesla, whose year-to-date declines range from 7.1% to 29.5%.

META Stock Performance

Image Source: Zacks Investment Research

META’s stock valuation seems stretched, as indicated by a Value Score of C. Currently, META is trading at a forward 12-month Price/Sales ratio of 7.23X, surpassing the broader sector’s 5.59X.

Price/Sales (F12M)

Image Source: Zacks Investment Research

AI as a Growth Catalyst

With over 3.35 billion daily users, META holds vast amounts of data for AI applications. The company continues to enhance its platforms’ capabilities, making it a favored choice among advertisers. Using its proprietary Andromeda machine learning system, META aims to improve ad performance by delivering personalized content.

The implementation of META’s deep neural network on the NVIDIA Grace Hopper Superchip has led to improvements of over 6% in recall and more than 8% in ad quality for targeted segments.

Tools like Advantage+ are streamlining campaign management and enhancing performance by delivering a greater number of ads to various audience segments. META’s generative AI capabilities are helping advertisers create engaging content to retain business.

With more than 700 million monthly active users of its AI offerings, META plans to continue enhancing user interactions through personalized updates.

Investment Considerations Ahead of Q1 Results

While META’s AI initiatives present promising growth prospects, concerns arise from its current valuation and ongoing regulatory challenges. Presently, Meta Platforms holds a Zacks Rank #3 (Hold), suggesting that investors may want to hold off on accumulating the stock until a better buying opportunity arises.

This report originally appeared on Zacks Investment Research.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.