NVIDIA Corporation (NVDA) has experienced over 1,000% growth in stock value over the past five years, though in the past year, Micron Technology, Inc. (MU) outperformed with a 307% increase compared to NVIDIA’s 43.1%. This shift highlights Micron’s emergence as a pivotal player in AI investments driven by strong demand for its high-bandwidth memory (HBM) chips.

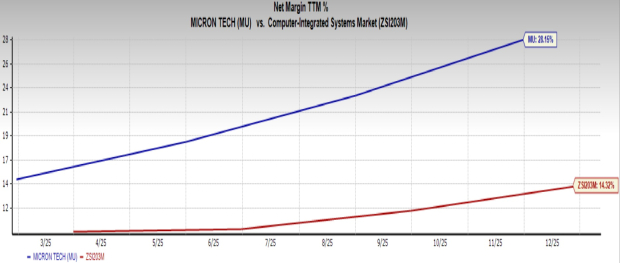

Micron’s CEO, Sanjay Mehrotra, indicated that ongoing demand for HBM chips and constrained supply could enhance profit margins. The company expects fiscal second-quarter 2026 revenues between $18.3 billion and $19.1 billion, surpassing the $13.64 billion reported in the first quarter of the fiscal year. Additionally, Micron’s net profit margin stands at 28.2%, significantly higher than the industry average of 14.3%.

Investors are optimistic about Micron’s future, supported by a Zacks Consensus Estimate of $32.9 for earnings per share (EPS), reflecting a projected growth of 204.3% year-over-year. Micron’s forward price-to-earnings (P/E) ratio of 11.66 is notably below the industry average of 18.18, marking it as a strong investment opportunity.