MillerKnoll, Inc. MLKN is gearing up to unveil its financial feathers with the release of its third-quarter fiscal 2024 results on Mar 27, 2024, post-market closure.

Casting a glance backward, in the previous quarter, MillerKnoll’s earnings not only eclipsed the Zacks Consensus Estimate by a triumphant 13.5%, but soared a staggering 28.3% compared to the prior year. Despite this, net sales fell short of the consensus by 1% and dipped by 11% on a yearly scale.

In an avian-like fashion, MillerKnoll’s earnings have continuously taken flight above the consensus estimate for the past four quarters, showcasing an awe-inspiring average surprise of 33.3%.

The Path of Estimations

Over the last 60 days, the Zacks Consensus Estimate for MillerKnoll’s third-quarter EPS has perched at 44 cents, unmoved. This anticipation foretells an 18.5% descent from the EPS value of 54 cents reported in the same quarter of the previous year.

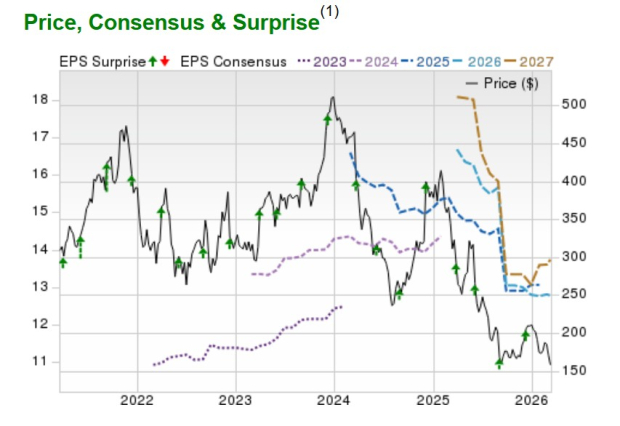

Peering into the Teacup: MillerKnoll’s Price and EPS Surprises

Behold the Price and EPS Sorcery of MillerKnoll, Inc. | MillerKnoll, Inc. Quote

The predicted revenue consensus tallying at $910.2 million hints at a 7.6% year-over-year aerial descent.

The Unveiling of Influences

Anticipatedly, MillerKnoll’s net sales and EPS may have taken a nosedive in the third fiscal quarter owing to dwindling sales volume in the soft feathers of the North American housing market. Simultaneously, the company faced headwinds from challenging economic environments in Europe and China, further obstructing growth.

For the fiscal rendezvous of Q3 2024, MillerKnoll expects net sales ranging between $890 to $930 million, fluttering downwards compared to the previous year.

Spanning its wings, MLKN foresees an adjusted gross margin span of 37.8-38.8% for the quarter, a boost from the yesteryears’ 35.7%. This elevation might be attributed to strategic stock handling, moderated input expenses, pricing optimization strategies hitting their mark, and reaping the rewards of ongoing synergy efforts.

On the operating expenditure front, a forecasted flight ranging $285-$295 million looms, surpassing the $277.6 million governance recorded a year ago. Diluted adjusted EPS is anticipated to range between 40-48 cents for the quarter, a slight downward drift from the comparable quarter in the previous year.

With wings spread wide, a diversified business model, bolstered by a sturdy brand portfolio, customer segment diversity, and geographical reach, offers MillerKnoll risk mitigation and opportunities for growth.

Reading the Fortune Teller: What Our Models Reveal

Our tried-and-tested model does not offer a precise gaze into MLKN’s earnings this cycle. Traditionally, a blend of a positive Earnings ESP, combined with a Zacks Rank of #1 (Strong Buy), 2 (Buy), or 3 (Hold), augurs well for an earnings perch. This quarter, however, does not unfurl as anticipated.

Earnings ESP: MLKN flaunts an Earnings ESP of 0.00%. Uncover more insights on today’s market entrants before the earnings dawn with our Earnings ESP Filter.

Zacks Rank: Currently crowned with a Zacks Rank #3, MillerKnoll waits in anticipation as the earnings reveal draws near.

Inclining the Ears Towards Earnings Triumph: Stocks to Behold

Within the Consumer Discretionary realm, a few other stocks warrant attention, favored by our modelling as prospective triumphants in the earnings arena.

Hasbro, Inc. HAS boasts an Earnings ESP of +24.90% and clinches a Zacks Rank #3. Explore the grand list of today’s foremost Zacks #1 Rank stocks here.

Envisionedly, HAS prepares for a staggering earnings boost of 2900% for the impending quarter. Alas, lower-than-expected earnings marked three of the previous four quarterly apparitions, settling at an average negative surprise of 32.8%.

MGM Resorts International MGM currently holds an Earnings ESP of +11.70% and graces a Zacks Rank #2.

Forecasts predict MGM will see an earnings surge of 38.6% in the forthcoming quarter. Its trail of better-than-expected earnings in the past four quarters leaves an enchanted average surprise of 271.5%.

Carnival Corp. CCL currently wears the mantle of an Earnings ESP of +6.26% and a Zacks Rank #2.

Portendedly, CCL’s earnings for the upcoming quarter look ripe for a 69.1% climb. Past earnings whispers suggest a string of better-than-expected showings, pegging the average surprise at 19.2%.

Stay attuned to forthcoming earnings galas with the Zacks Earnings Calendar.

Ready to Witness a Marvel Unfold?

From a plethora of stocks, 5 Zacks mavens have each picked their celestial favorites, poised to soar a whopping +100% or more in the seasons to come. Out of these, Director of Research Sheraz Mian specifically delves into a rising star with the potential for extraordinary growth.

This exceptional candidate is credited with an awe-inspiring “watershed medical breakthrough,” paving the path for a vibrant pipeline of projects that could revolutionize the healthcare landscape for patients grappling with hepatic, pulmonary, and hematological disorders. This represents an opportune moment for investment, catching a rising star on the verge of ascending from the shadowy lows of the bear market.

This unmissable prospect might soon outshine recent Stocks Set to Double, including the remarkable ascent of Boston Beer Company by +143.0% in a scant 9 months and NVIDIA’s stratospheric surge by +175.9% in a single year.

Witness the Crescendo: View Our Top Pick and 4 Honorable Mentions

Foray into Fuller Details at Zacks.com with a Click Here

The vantage points articulated herein reflect the author’s lens and do not necessarily mirror those of Nasdaq, Inc.