MillerKnoll, Inc. MLKN is gearing up to unveil its first-quarter fiscal 2025 financial results after the market closes on Sept. 19, 2024.

The previous quarter saw the company surpassing the Zacks Consensus Estimate for earnings by a staggering 26.4% and marking a 63.4% year-over-year increase. However, with net sales falling short of expectations by 1.1% and declining 7.1% versus the previous year, the stakes are high for MillerKnoll’s upcoming report.

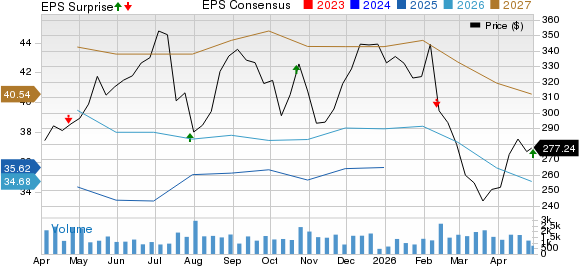

Remarkably, MillerKnoll has outperformed the consensus estimate for earnings in each of the last four quarters, with an average surprise of 29.6% to the delight of investors.

MillerKnoll, Inc. Price and EPS Surprise

MillerKnoll, Inc. price-eps-surprise | MillerKnoll, Inc. Quote

Reading the Trends for MLKN’s Q1

The Zacks Consensus Estimate for MillerKnoll’s first-quarter earnings per share has held steady at 42 cents over the last 60 days, signifying a potential 13.5% growth compared to the same quarter last year. Meanwhile, the projected net sales consensus stands at $892 million, pointing towards a modest 2.8% year-over-year decline.

Factors at Play for MLKN’s Q1

MillerKnoll expects a year-over-year decrease in net sales for the first quarter, largely attributing it to reduced sales volume amidst a challenging North American housing market. The company has set sales expectations between $872 million and $912 million, indicating a slight decline from the prior year.

Despite market hurdles, MillerKnoll remains focused on enhancing margins and operational efficiency through product innovation and integration synergies from Knoll. The implementation of pricing strategies and logistic improvements are anticipated to boost margins, with an expected adjusted gross margin of 39-40%, marking an improvement from the previous year.

Projected lower operating expenses and an increase in adjusted earnings per share further underscore MillerKnoll’s strategic efforts to navigate the tough market environment and deliver value to shareholders.

Insights on MLKN’s Q1 with a Quantitative Lens

While a positive Earnings ESP combined with a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) typically signals a higher likelihood of an earnings beat, MillerKnoll’s current scores don’t paint a conclusive picture. With an Earnings ESP of 0.00% and a Zacks Rank #3, the upcoming report seems poised for intrigue.

Comparative Performance Among Peers

Peers in the industry, including Virco Manufacturing Corporation (VIRC), Bassett Furniture Industries, Incorporated (BSET), and Culp, Inc. (CULP), have shared mixed results in their recent quarterly reports, mirroring the industry’s dynamic landscape.

Each company is strategizing to address market challenges, enhance operational efficiency, and drive long-term growth, highlighting the resilience and adaptability required in the competitive market environment.

© 2024 Benzinga.com. Benzinga reminds readers that prudent investment decisions require careful consideration and analysis. All rights reserved.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.