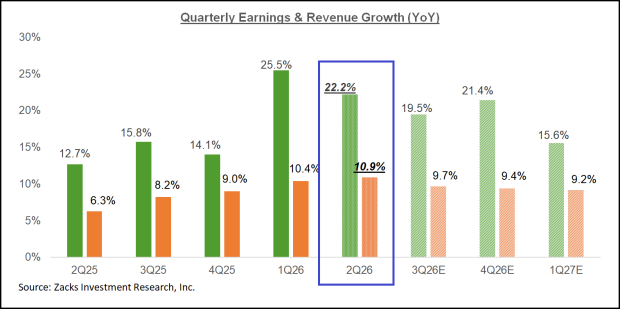

MRC Global Inc. MRC has been thriving due to its diversified presence across multiple end markets, including upstream production, midstream pipelines, gas utilities, and Downstream, Industrial, and Energy Transition (“DIET”). The company’s robust performance in the DIET sector has been fueled by a surge in energy transition activities in the United States, with revenues from this sector witnessing a notable 4% year-over-year increase in the fourth quarter of 2023. Additionally, heightened customer infrastructure activity in the Permian basin has been a boon for the company.

The company’s dedication to customer service, bolstered by reliable operations and efficient supply-chain management, along with the introduction of new products, has been highly beneficial. Despite cost inflation, strategic pricing actions have been instrumental in driving the company’s margin performance. For instance, MRC Global’s adjusted gross margin saw a 70 basis point increase year over year, reaching 21.9% in the fourth quarter.

MRC has remained committed to enriching shareholder value through dividend payouts, having disbursed dividends worth $24 million in 2023. Moreover, debt reduction continues to be a key priority for the company, which repaid $882 million in borrowings under revolving credit facilities during 2023.

Image Source: Zacks Investment Research

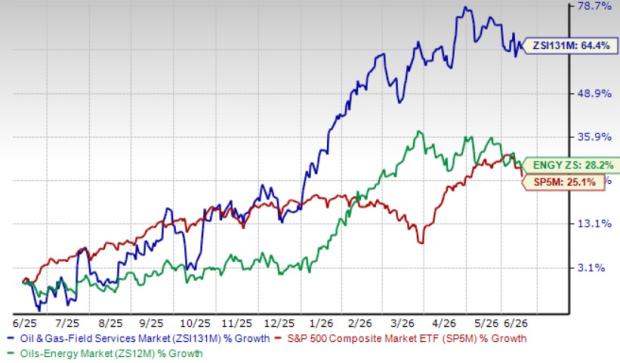

Over the past three months, the Zacks Rank #3 (Hold) company has witnessed a remarkable 11.5% growth, outperforming the industry’s decline of 8.4%.

However, a downturn in customer spending for modernization and replacement activity, coupled with delayed customer projects, has adversely impacted the Gas Utilities and Production & Transmission Infrastructure (PTI) sectors. Revenues from these sectors saw a 21% and 15% year-over-year decrease, respectively, in the fourth quarter. MRC anticipates an overall revenue flatline to low-to-mid single digit decline in 2024.

MRC has been grappling with the adverse effects of soaring operating costs and expenses. In 2023, its cost of sales remained high at $2.72 billion, while selling, general, and administrative expenses surged by 7% to $503 million, primarily due to escalated employee-related costs and associated benefit costs.

Promising Stock Options in the Industry

Among the prevailing options in this industry, three companies stand out — AZZ Inc. (AZZ), Valmont Industries (VMI), and Mueller Water Products (MWA), each carrying a Zacks Rank #2 (Buy). For further insights, you can explore the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

AZZ has exhibited a trailing four-quarter average earnings surprise of 37.5%, with the Zacks Consensus Estimate for AZZ’s 2024 earnings witnessing a noteworthy 4.9% increase in the past 60 days.

Valmont Industries has recorded a trailing four-quarter average earnings surprise of 5.9%, while the consensus estimate for VMI’s 2023 earnings has remained stable over the past 60 days.

Mueller Water Products posted a trailing four-quarter average earnings surprise of 23.7%. Furthermore, the consensus estimate for MWA’s 2024 earnings has improved by 9.5% in the last 60 days.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.” Since 1988, the full list has outperformed the market by more than 2X, delivering an average annual gain of +24.0%. Hence, these hand-picked 7 stocks deserve immediate attention.

For the latest recommendations from Zacks Investment Research, you can download the report on 7 Best Stocks for the Next 30 Days.

Valmont Industries, Inc. (VMI) : Free Stock Analysis Report

AZZ Inc. (AZZ) : Free Stock Analysis Report

MRC Global Inc. (MRC) : Free Stock Analysis Report

Mueller Water Products (MWA) : Free Stock Analysis Report

For the original article, visit Zacks.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.