In 2023, the stock market made an impressive recovery from one of its worst years in over a decade, which occurred in 2022. However, the journey for us investors hasn’t been smooth.

Amid worries about inflation, escalating interest rates, an unforeseen crisis in regional banking, and escalating global tensions such as conflicts in Ukraine and Palestine, the US economy displayed resilience. Corporate profits saw an upward trend despite these challenges.

The year 2023 saw impressive returns across indices:

- S&P 500 posted a return of 24.2%.

- Dow Jones gained 13.8%.

- NASDAQ 100 surged by 43.4%.

- My portfolio yielded a return of 22%.

Yes, that’s correct. Following a successful 2022 when my portfolio yielded positive returns compared to the S&P 500’s double-digit slump, my portfolio underperformed the market in 2023.

I was caught off guard in the early months of the year, anticipating underperformance from the tech mega-caps and consequently heavily investing in defensive companies, REITs, telecommunications, and healthcare. Additionally, a significant portion of my investment was in cash, yielding 4% in my domestic market denominated in euros.

Most of my core holdings were of a defensive nature, focused on high quality earnings and dividend growth:

- PepsiCo (PEP) 10-year EPS growth 6.8%, Yield 2.95%

- Realty Income Corporation (O) 10-year FFO growth 5.11%, Yield 5.34%

- UnitedHealth Group (UNH) 10-year EPS growth 17.2%, Yield 1.38%

- Verizon Communications (VZ) 10-year EPS growth 1.7%, Yield 6.76%

- Visa (V) 10-year EPS growth 15.6%, Yield 0.8%

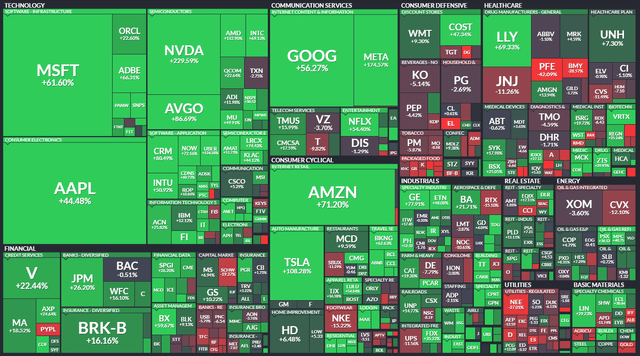

However, it’s the technology, communication services, and consumer discretionary stocks that saw substantial rebounds in 2023, alongside the general rise of growth stocks.

One pivotal factor behind this shift has been investors moving their attention from concerns about rising interest rates to the potential for rate cuts as early as 2024. This shift rescued the performance of REITs, propelling them into positive return territory during the last two months of the year.

Not only did many stocks bounce back, but high-growth, cyclical sectors like technology, communication, and consumer discretionary emerged as the top performers within the S&P 500 for the year.

The Magnificent 7 stocks alone initially comprising 19% of the S&P 500, surged to dominate at 30%. Their impact on the index was unparalleled, accounting for a staggering 70% of its total returns for the year.

On the flip side , defensive sectors where I was heavily invested, including utilities, healthcare and consumer staples, have been the biggest laggards in 2023.

As we step into 2024, the market and economy confront a fresh set of uncertainties:

- Has inflation truly been conquered, or are we heading for another spike?

- When will the Fed cut rates, and by how many basis points?

- Are we poised for a soft or hard landing?

- Which investments will outperform and yield superior returns in 2024?

With that, let me introduce you to my top holdings for 2024 and explain why I believe these companies are poised to deliver exceptional returns.

Alphabet Inc. (GOOG) – The Search Giant’s Rebound

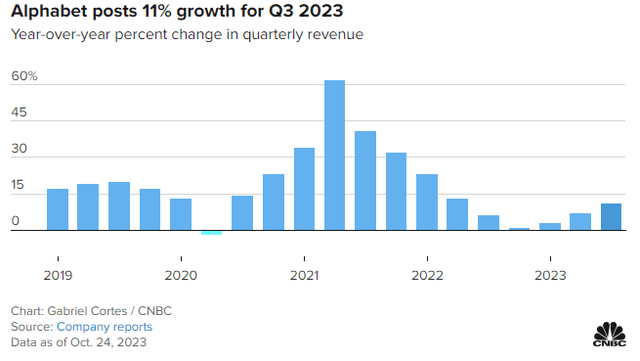

In early November, 2023, I wrote a bullish piece about Alphabet Inc., detailing a significant drop in stock value from $142 to $121 following Q3 earnings. This decline, triggered by slower growth in Google’s Cloud unit, led to a staggering $180 billion loss in market capitalization.

Q3 of 2023 saw Google Cloud’s growth rate decrease to 22.4%, a drop from the steady 28% growth seen in the year’s initial two quarters. However, it’s important to put this into perspective. Despite this slowdown, the cloud unit accounted for only 10.9% of Q3 revenue. Moreover, this deceleration in growth has been a trend for the past 10 quarters.

Since publishing the article, the stock has rebounded as anticipated, yielding a close to 9% return. Taking advantage of this, I made significant purchases of Alphabet Inc. stock around $125. To me, this seemed like an overreaction, especially considering Google’s growth, which had been picking up since the 2022 ad spending slump and reported an 11.1% growth.

Today, Alphabet Inc. is among my largest holdings.

This quarter, there’s been a shift from the usual pattern of single-digit revenue gains, coinciding with the ongoing recovery in the advertising market.

Looking ahead to 2024, a crucial election year in the US, the landscape seems ripe for heavy political contention amidst the country’s prevalent issues. Businesses geared toward advertising stand to benefit significantly from increased online campaigning. Meta Platforms, Inc. (META) is anticipated to be one of the prime beneficiaries as well, alongside Alphabet Inc.

Moreover, Alphabet Inc.’s investments in AI are expected to bear fruit in 2024. This growth extends not only to its cloud business but also to the expansion into generative AI, like Bard, beyond its existing offerings.

In October, Alphabet Inc. committed up to $2 billion in Anthropic, an AI startup behind Claude 2, a chatbot rivaling OpenAI’s ChatGPT. Claude 2 boasts the ability to summarize up to about 75,000 words, a significant capability compared to ChatGPT’s 3,000-word capacity. This technology allows users to distill large datasets into concise memos, letters, or stories.

While the company’s performance in 2023 was underwhelming, the potential for growth and rebound in 2024 makes Alphabet Inc. a strong buy for the year.

Investment Opportunities: Google, Nvidia, and Lowe’s

Google (GOOGL) – Strong Buy

Amidst the volatile waters of the stock market, Google’s valuation stands on firm ground. With a current trading ratio of 24x its blended P/E ratio, it seems to emerge as the “cheapest” among the illustrious Magnificent 7.

Since 2014, the company’s average valuation has orbited around 24.9x its earnings. Although the present price doesn’t immediately shout “discount,” the projected 16% EPS growth in the next two years seems to fit like a glove with the historical 17.5% growth rate.

Thus, the valuation of 24.8x its earnings appears to be sensible. If the forecasted growth unfolds, Google could soar to deliver an annual performance surpassing 17% over the coming three years, hence the hearty nod to a strong buy rating.

Nvidia (NVDA) – Strong Buy

In a digital age characterized by exponential technological strides, Nvidia emerges as the stellar frontrunner in the semiconductor space, embellished with a lavish $1.19 trillion market cap. A venerable pioneer in graphics processing units, or “GPUs,” it has toiled to etch its dominance in gaming, artificial intelligence, and deep learning.

Renowned worldwide for its innovations, Nvidia’s cutting-edge GPU solutions not only reign over the gaming sphere but also spearhead revolutions in data centers, autonomous vehicles, and numerous other sectors.

As the spotlight gleams on AI, Nvidia adroitly diversified its revenue streams beyond gaming, particularly propelling into Data Centers, now the largest segment. Realizing a staggering $14.5 billion in revenue in the previous quarter, it proclaims a phenomenal 378% year-over-year growth. This division now commands 80% of the total revenue, a dramatic shift from the era when gaming upheld over 50% of the earnings.

Nvidia’s stock has witnessed a rollercoaster ride. In 2023, it soared to earn the accolade of the S&P 500’s top-performing stock, sporting an enviable 220%+ return, chiefly attributed to its pivot towards data centers and the favorable tailwinds of AI.

Yet, the present price of Nvidia at $493 highlights the market’s capricious nature, depicted in its recent history. In 2022, the stock plummeted to a mere $108 from a prior peak of $346 during the tumultuous trading frenzy kindled by the pandemic, marking a momentous 70% decline.

For Nvidia, the central plot revolves around growth. If this growth fails to unfurl in the future, the company could face a stark realization – implying the presence of risks but also heralding substantial rewards.

While skeptics ponder over Nvidia’s potential to expand its earnings due to heightened competition, which could impede its profit margins (currently a resilient 74% Gross margin as of Q3 FY24, notably higher than its historical margins), the company’s engineering prowess positions it a league above rivals such as AMD (AMD).

Over the bygone 15 years, Nvidia has etched out a magnificent EPS growth rate of 39.54%, and signs of slowing down are nowhere in sight. Instead, the growth is anticipated to accelerate in the imminent years:

- 2024: Projected EPS of $12.28, YoY growth of 268%

- 2025: Projected EPS of $20.44, YoY growth of 66%

- 2026: Projected EPS of $24.06, YoY growth of 18%

If the anticipated growth transpires, the current blended P/E ratio of 41.3x masquerades as a lucrative deal.

In the preceding 15 years, the average valuation revolved around 34.9x its earnings. This places the stock at a premium, but given the anticipated accelerated growth, this valuation appears well-justified.

If this valuation endures over the next three years, we might witness Nvidia unfurling an annual return eclipsing 30%. An astounding feat, but Nvidia has to measure up to these expectations.

In my estimation, with the AI trends reigning supreme in the 2020s, this should pose no hindrance as long as the company maintains its pioneering stance within the industry, thus warranting the strong buy rating.

Lowe’s (LOW) – Buy

Lowe’s, a prominent player in the US and Canadian home improvement terrain, offering an array of building materials, appliances, décor, and tools, seems to have been treading water in the stock market over the past two years.

This stagnant trajectory aligns with significant price appreciation during the pandemic-induced low-interest-rate spell from 2020 to 2021, during which the company seemingly borrowed from the future demand.

The lackluster performance in stock price and earnings owes its dues to the burgeoning mortgage rates in its key markets, which surged from a pandemic low of 2.60% to nearly 8% in October, subsequently retracting to 6.67% for the 30-year fixed rate.

Lowe’s business heavily leans on existing home sales, with 75% of its earnings emanating from the do-it-yourself “DIY” sector and the remaining 25% from PRO customers.

However, amid the pandemic, a surge of homeowners locked in their interest rates below 3%, breeding apprehensions about selling their houses due to the prospects of securing

Lowe’s and Home Depot’s Prospects in 2024

The year 2023 posed significant challenges for the housing market, impacting existing home sales and subsequently influencing the performance of major home improvement retailers. The changing economic landscape called for investors to reevaluate their portfolios and consider the future prospects of companies such as Lowe’s and Home Depot. As we step into 2024, potential rate cuts by the FED signal a glimmer of hope for the housing market, and consequently, the businesses of these retail giants.

Redefining the Home Improvement Market

The housing market, in 2023, witnessed a shift dubbed as the “Great Reshuffling” where families sought larger, more suitable homes amid the pandemic-induced work-from-home culture. This trend led to a slowdown in existing home sales, prompting nearly one-third of homes in the US to be sold as new constructions, a significant increase from approximately 17% in 2020. Consequently, this affected the landscape for home improvement retailers, as fewer individuals engaged in house renovations or flipping homes, impacting their top and bottom lines.

A Glimmer of Hope

The potential for rate cuts by the FED in 2024 presents a ray of hope for the home improvement market. These projected rate cuts are expected to directly impact mortgage demand, potentially revitalizing existing home sales. If these expectations materialize, it would mark a positive turn for Lowe’s and Home Depot, reinvigorating their businesses in the tumultuous post-pandemic market.

Assessing Lowe’s Position

Despite the complex market dynamics, Lowe’s presents an interesting investment opportunity. Trading at 16.2x its blended P/E ratio, significantly lower than its 15-year average of 19.8x, the company is seemingly undervalued. While facing challenges such as a decline in EPS, Lowe’s historical EPS growth rate and its projected resurgence in 2025 hint at its potential for a strong rebound.

Forecasting the Future

Looking ahead into 2024 and beyond, investors are presented with the opportunity to position their portfolios strategically. The potential for a resurgence in the housing market, accompanied by forecasted growth in EPS, could position Lowe’s for a substantial total return by the end of 2025, provided the market realizes the company’s true valuation.

Embracing Investment Opportunities

Every market year brings fresh challenges and narratives, and the year 2023 was no exception. It’s a reminder for investors to stay invested while assessing and adjusting their portfolios in line with the evolving market landscape. As we enter 2024, the potential for a market shift and favorable valuations presents an opportunity to capitalize on the growth prospects of companies such as Lowe’s. Investors are encouraged to consider the potential and risks associated with such opportunities, aligning their choices with their financial goals.